Doctors can get steady monthly retirement income by combining guaranteed sources like annuities and bonds with income investments such as dividends, real estate, and planned withdrawals.

There is no single “best” option—your ideal setup depends on your retirement age, risk tolerance, tax bracket, and how predictable you want your retirement income to be.

This guide is written for physicians and medical professionals who are no longer asking how to grow money, but instead want to know where to invest retirement savings so they actually produce steady monthly income.

The strategies below are based on bank-led retirement research, insurer data, and investment frameworks commonly used in wealth management for high-income professionals not internet hype. By the end, you’ll understand how doctors typically build a durable income strategy that doesn’t fall apart when markets change.

Dividend-Paying Stocks

Dividend-paying stocks work because they convert business profits into repeatable retirement income without forcing you to sell assets. For physicians, this matters because your human capital disappears at retirement age, and replacing earned income requires assets that pay you back.

Dividend income behaves differently from market appreciation. Even when prices fluctuate, established companies often maintain payouts because dividends signal financial stability. This makes dividend-paying stocks useful inside both a retirement account and taxable portfolios.

Where doctors go wrong is yield chasing. High yields often mean fragile businesses. A sustainable income strategy focuses on companies with long dividend histories, rising cash flows, and pricing power. Healthcare, utilities, and consumer staples often fit this profile.

Dividend income also interacts favorably with retirement plans that already include growth assets. Instead of drawing down principal early, dividends slow the depletion of retirement savings, extending portfolio longevity.

This approach works best when matched to your risk tolerance, since equity income still fluctuates. Used correctly, dividends supplement Social Security, reducing pressure to claim benefits early.

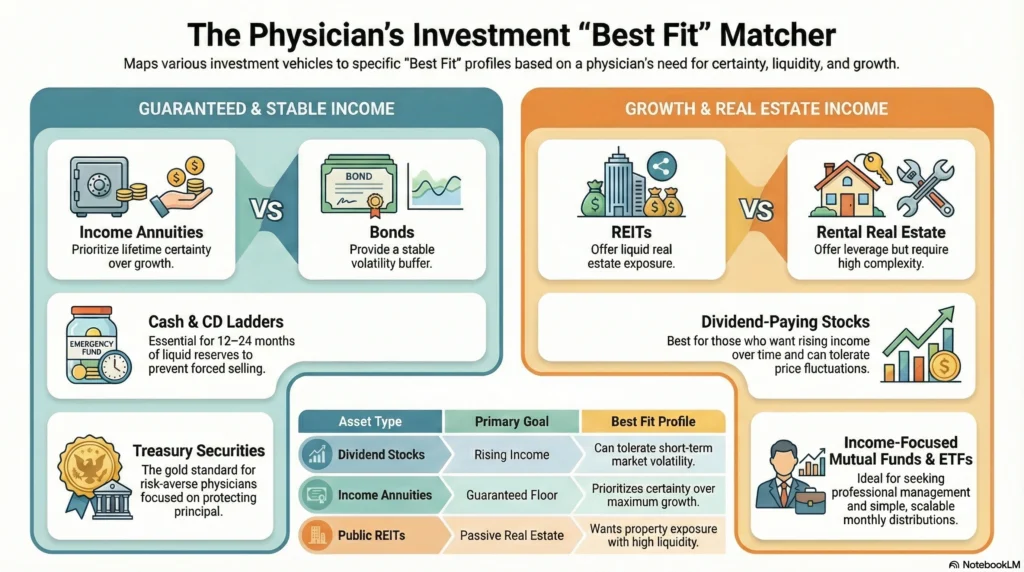

Best fit: Physicians who want rising income over time and can tolerate short-term volatility.

Bond Funds & Bond Ladders

Bonds are the structural backbone of fixed income investing. They exist to do one job: deliver predictable cash flow while dampening volatility.

According to U.S. Bank, a diversified bond portfolio can generate regular payouts while lowering portfolio risk

For physicians transitioning from accumulation to retirement income, bonds act as a shock absorber. A bond ladder—where bonds mature at staggered intervals—creates scheduled liquidity, allowing you to meet expenses without selling stocks during downturns.

Bond funds simplify this process by pooling maturities and issuers. While less precise than ladders, they offer instant diversification and professional management, which fits many doctors’ time constraints.

The key is duration management. Longer bonds pay more but react strongly to interest-rate changes. Shorter bonds provide stability but less income. A balanced approach aligns investment options with spending timelines rather than market forecasts.

Bonds also integrate well with traditional IRA distributions, smoothing required withdrawals while preserving capital.

Best fit: Physicians seeking stability and lower volatility in retirement savings.

Income Annuities

Income annuities exist to replicate what most doctors no longer have: a guaranteed pension.

Guardian Life explains that annuities are designed to convert savings into a steady retirement income stream, with payment options that can last for life or a fixed period

An annuity converts a portion of retirement savings into a contractually guaranteed monthly payout. This monthly benefit continues for life or a defined period, regardless of market performance.

The real value is psychological. Annuities cover essential expenses like housing, utilities, and insurance. They reduce the need to depend on unstable markets. This allows the rest of your portfolio to stay invested longer.

Used poorly, annuities reduce flexibility. Used selectively, they stabilize your retirement income plan.

Doctors often layer annuities alongside Social Security, creating a guaranteed income floor before tapping investments. This sequencing protects longevity risk, which is often underestimated in high earners.

Best fit: Physicians prioritizing certainty over maximum growth.

REITs (Public, Not Speculative)

Public REITs distribute rental income from commercial properties—often hospitals, medical offices, and senior housing—making them uniquely aligned with physician wealth profiles.

REITs produce income through mandatory distributions while offering liquidity that direct real estate lacks. This matters for doctors who want real estate exposure without tenant calls or maintenance headaches.

Because REIT income fluctuates, they work best when blended with fixed income and dividend stocks. Inside a retirement account, REIT distributions grow tax-deferred, enhancing compounding.

REITs also diversify retirement plans away from traditional equity risk, improving overall portfolio resilience.

Best fit: Physicians seeking real estate income with liquidity.

Rental Real Estate

Direct rental real estate produces income through rent, appreciation, and tax advantages. It remains one of the most powerful tools for physicians who understand leverage and cash flow.

But complexity is real. Rental properties cause problems without professional management. This is especially true during retirement. Doctors who succeed treat real estate as a business, not a side hobby.

When structured properly, rental income reduces reliance on Social Security and market withdrawals. It also diversifies income sources, protecting against policy or tax changes.

Real estate works best for physicians with adequate liquidity and patience. It should complement—not replace—core retirement savings vehicles.

Best fit: Physicians comfortable with long-term ownership and complexity.

High-Yield Savings Accounts

A savings account will not fund retirement—but it prevents bad decisions.

Holding 12–24 months of expenses in cash reduces forced selling during downturns. This improves long-term outcomes more than chasing returns.

Doctors often do not realize how important cash availability becomes after retirement. Cash buffers allow you to delay claiming Social Security, which increases lifetime benefits.

Citizens Bank includes cash-based savings vehicles as part of a balanced retirement income mix

Savings also smooth tax planning, letting you control withdrawals from taxable and tax-deferred accounts based on your tax bracket each year.

Best fit: Emergency reserves and short-term income needs.

Certificates of Deposit (CDs)

CDs provide contractual interest for a defined period. They function as short-term fixed income tools when certainty matters more than growth.

For physicians entering retirement, CD ladders create predictable cash flow while preserving principal. They are especially useful when markets feel overheated.

CDs often sit between savings and bonds in a broader investment strategy, filling timing gaps without market exposure.

Best fit: Physicians who value certainty and capital preservation.

Income-Focused Mutual Funds & ETFs

Income-focused funds bundle dividend stocks, bonds, or both into a single structure. This makes management easier. It also provides regular payments.

These vehicles shine for physicians who value simplicity and consistency. Inside a Roth IRA, distributions compound tax-free, making them powerful late-stage tools.

U.S. Bank highlights a total return approach using diversified funds with systematic withdrawals

Funds also adapt automatically as markets shift, reducing behavioral mistakes that derail retirement plans.

Best fit: Doctors who want simplicity and professional management.

Treasury Securities / Government Bonds

Treasuries deliver income backed by the U.S. government. While returns are modest, reliability is unmatched.

Doctors often use Treasuries to fund essential expenses early in retirement, reducing stress during volatile periods. This stabilizes retirement income and improves portfolio longevity.

Treasuries also serve as collateral for more aggressive investments elsewhere, balancing growth with certainty.

Best fit: Risk-averse physicians protecting principal.

Dividend-Focused ETFs

Dividend ETFs provide exposure to dozens or hundreds of dividend-paying companies. They reduce single-company risk while delivering consistent income.

For physicians managing large portfolios, ETFs scale efficiently. They integrate seamlessly into wealth management frameworks and simplify rebalancing.

Dividend ETFs also pair well with Social Security, filling income gaps while maintaining equity exposure.

Best fit: Physicians seeking scalable, rules-based income.

How Doctors Combine These Strategies

Most doctors blend:

- Social Security as a base monthly benefit

- Fixed income for stability

- Dividends for growth

- Select guarantees for peace of mind

Read: [Retirement Account vs Investment Account]

Read: [401k Investment Alternatives]

Read: [What to Do After Maxing Out 401k]

Read: [Where to Invest Money to Get Good Returns for Beginners]

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

There is no single “best” investment; the most reliable monthly income comes from combining dividends, bonds, annuities, and Social Security into one coordinated income strategy. The right mix depends on how much income you need, how stable you want it to be, and how much market risk you can tolerate.

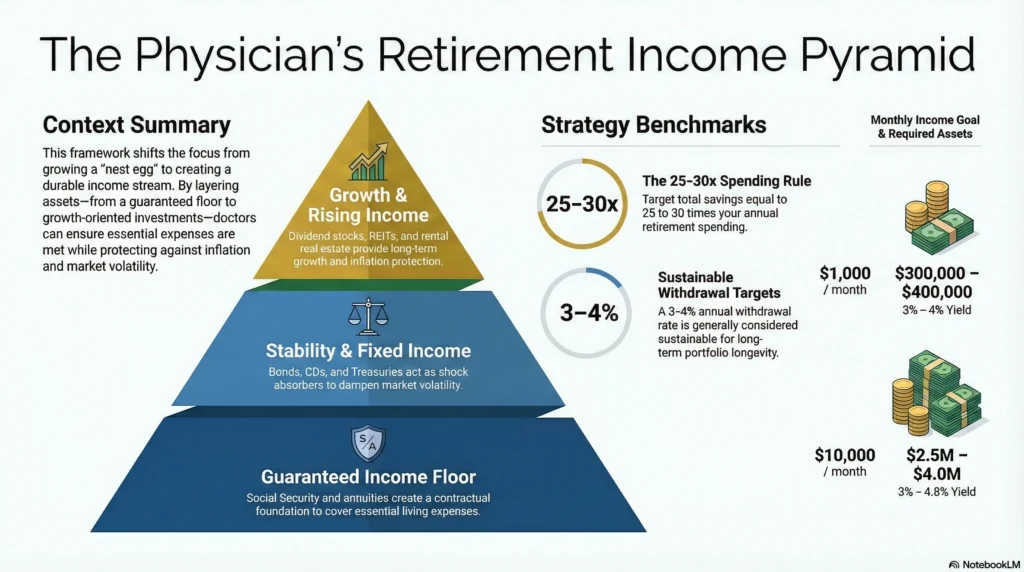

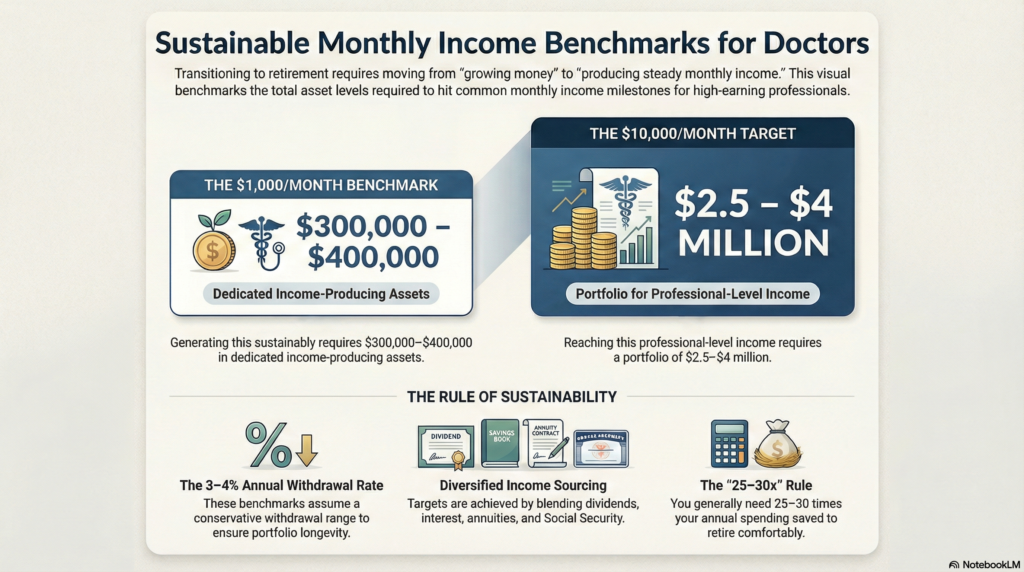

You typically need $300,000–$400,000 invested to generate $1,000 per month sustainably, assuming a 3–4% annual withdrawal rate. The exact amount depends on whether income comes from dividends, interest, annuities, or a mix of sources.

Regular monthly income usually comes from dividend-paying stocks or ETFs, bond funds, income annuities, rental real estate, and Treasury securities. Most retirees use more than one source to reduce the risk of income interruption.

To generate $10,000 per month sustainably, you generally need $2.5–$4 million in income-producing assets, depending on yield and risk. This level of income almost always requires diversification across investments, real estate, and guaranteed income sources rather than a single asset.

You generally need 25–30 times your annual spending saved to retire comfortably without running out of money. If Social Security or pensions cover part of your expenses, the required savings amount may be lower.

Your Social Security benefit depends on your earnings history and when you claim, but for high-income professionals it often replaces 20–35% of pre-retirement income. Delaying benefits past full retirement age increases your monthly benefit permanently.

Safer income options include Treasuries, high-quality bonds, CDs, income annuities, and dividend-focused funds, though each has tradeoffs. “Safe” means lower volatility—not higher returns—and often requires accepting more modest income.

You should think about income reliability, inflation protection, taxes, longevity risk, cash availability, and market changes before picking investments.

Ignoring any one of these factors can cause income shortfalls later in retirement.

The right investment options depend on your income needs, risk tolerance, tax bracket, and time horizon. Most retirees benefit from blending guaranteed income with market-based investments rather than choosing one approach.