Doctors don’t struggle with saving money—they struggle with where to put it once income rises and decisions start compounding.

This guide is for doctors and healthcare workers who earn well and invest. It helps them understand how retirement and investment accounts work together. It does not say which one is better.

We built this list by:

- Studying physician-specific retirement structures

- Analyzing IRS rules, contribution limits, and tax treatment

- Comparing real-world outcomes doctors face at different income stages

By the end, you’ll know:

- When a retirement plan creates leverage

- When an investment account creates freedom

- How doctors combine both to protect cash flow, taxes, and long-term wealth

Understanding Retirement Accounts

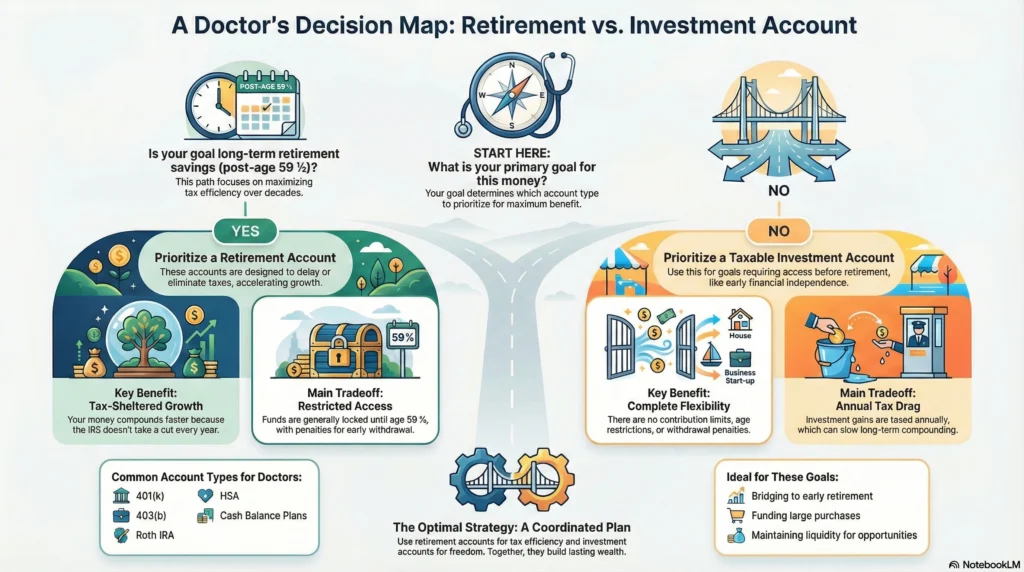

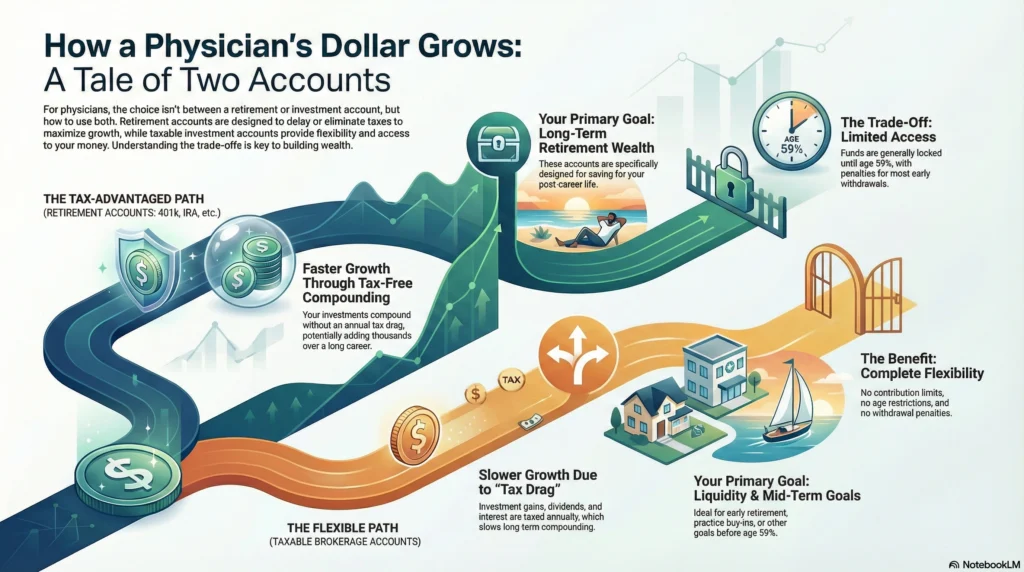

Retirement accounts exist to delay or eliminate taxes, not to maximize flexibility. That tradeoff is intentional.

This wide access allows doctors to time taxes strategically based on future income and retirement goals

The core benefit is compounding without tax drag. Money inside a retirement plan grows faster simply because the IRS doesn’t take a cut every year.

But the cost is access. Most retirement savings are locked until age 59½, and early withdrawals can trigger penalties.

This structure works best for doctors who:

- Expect rising income

- Want predictable retirement savings

- Can fund short-term goals elsewhere

Traditional vs. Roth Accounts

A Traditional IRA or Traditional 401k plan gives tax relief today. Contributions reduce taxable income, which matters for physicians in high brackets.

A Roth IRA or Roth 401k flips the equation. You pay tax now, but withdrawals later are tax-free.

Why this matters now:

Doctors often underestimate future tax exposure. In retirement, required distributions, Social Security, real estate income, and brokerage dividends add up.

Industry data shows that average IRA balances continue rising, reaching roughly $137,900 across age groups, reflecting long-term compounding effects

Roth accounts provide:

- Tax-free withdrawals

- No required minimum distributions

- Better estate planning outcomes

Tradeoff:

You give up immediate tax relief.

This is why many physicians use both—layering Traditional accounts early and Roth accounts later through backdoor Roth IRA strategies.

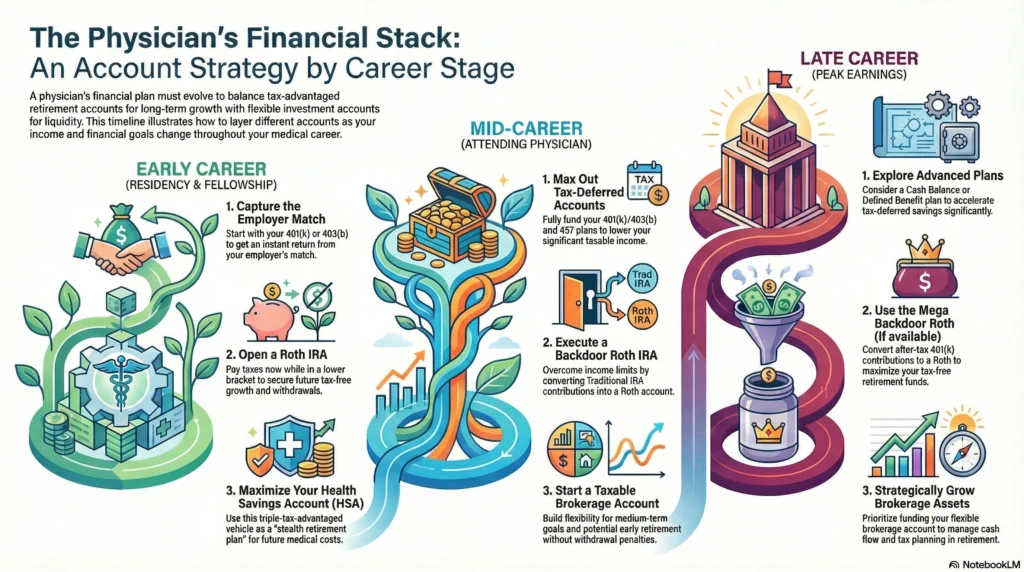

Employer-Sponsored Plans: 401(k), 403(b), and 457 Plans

An employer-sponsored retirement plan is usually the foundation of a physician’s retirement plan.

A 401(k) plan or 403(b) allows high annual contributions, while 457 plans offer unique withdrawal flexibility—often penalty-free once employment ends.

Why doctors care:

- Contribution limits are significantly higher than IRAs

- Payroll deductions automate retirement savings

- Employer matches boost returns instantly

However, not all plans are equal. Investment menus, fees, and plan rules vary widely.

Physicians often assume their 401k plan is optimal—many aren’t.

This is why doctors later explore:

- 401k investment alternatives

- supplemental defined contribution plans

- private investment layering

Read: [Where Doctors Should Invest After Maxing Out Their 401k and Roth IRA]

Leveraging Health Savings Accounts (HSAs)

A health savings account is the only vehicle with triple tax benefits:

- deductible contributions

- tax-free growth

- tax-free withdrawals for medical expenses

For doctors, this matters because healthcare costs don’t disappear in retirement.

Unlike Savings Accounts, HSAs can be invested in mutual funds, stocks, and ETFs.

Used correctly, an HSA becomes:

- a stealth retirement plan

- a hedge against future healthcare inflation

- a tax-efficient spending reserve

Doctors who pay medical costs out of pocket and let the HSA grow long-term extract the most value.

Managing Early Withdrawal Penalties and Required Minimum Distributions (RMDs)

Retirement accounts restrict access by design.

Withdrawals before 59½ often trigger penalties. Later, required minimum distributions force taxable income—even if you don’t need the money.

This matters for doctors who:

- want early financial independence

- plan semi-retirement

- sell a practice later in life

Investment accounts do not have these rules. Many doctors stop adding extra money to retirement plans when they want more flexibility.

Strategies for High-Income Earners

Once income exceeds Roth eligibility limits, doctors use structural workarounds.

The backdoor Roth IRA allows high earners to convert a Traditional IRA contribution into a Roth, preserving tax-free growth.

Used correctly, this avoids income caps entirely.

Some employer plans allow a mega backdoor Roth, using after-tax 401k plan contributions converted into Roth accounts.

These strategies matter because:

- Roth space is limited

- tax-free growth is extremely valuable for long careers

- future tax rates are uncertain

Mistakes here can trigger unexpected taxes, especially if pre-tax IRA balances exist.

Retirement Planning for Self-Employed Healthcare Professionals

Self-employed physicians control their retirement plan design.

Options include:

- Solo 401k plan

- Defined Benefit plans

- Cash Balance Plans

Defined benefit plans let doctors, especially older ones with steady income, contribute a lot.

Cash Balance Plans combine pension mechanics with modern flexibility.

These plans are powerful but complex. They require:

- consistent cash flow

- long-term commitment

- professional administration

If used right, these accounts help you save for retirement faster. They also lower your taxes a lot.

Handling Old Retirement Accounts

Old 401(k) plans from prior employers often:

- charge higher fees

- limit investment choice

- block backdoor Roth IRA strategies

Rolling into a Traditional IRA or consolidating into a current 401k plan can simplify management—but must be done carefully to avoid taxes.

This is a decision point, not an automatic move.

Tax-Efficient Investment Strategies

Investing in Taxable Accounts

Investment accounts, usually brokerage accounts, give full flexibility.

Unlike retirement accounts:

- no contribution limits

- no age restrictions

- no withdrawal penalties

They allow investing in stocks, bonds, mutual funds, ETFs, and Real Estate vehicles.

However, gains are taxed annually, which slows compounding.

This makes investment accounts ideal for:

- medium-term goals

- bridging early retirement

- liquidity for opportunities

- asset protection strategies

According to SmartAsset, brokerage accounts are the most common taxable investment vehicle and are used for goals beyond retirement

Read: [What to do after maxing out 401k]

Balancing Risk, Return, and Cash Flow

Doctors often over-optimize returns and under-optimize structure.

A strong financial setup balances:

- retirement savings for tax efficiency

- investment accounts for access

- insurance (including disability insurance) for downside protection

- debt control (especially credit card debt)

This balance—not account selection alone—drives financial independence.

Read:

Creating a Fulfilling and Financially Secure Future

Doctors don’t fail financially due to lack of income.

They fail due to uncoordinated financial plans.

Retirement accounts reduce taxes.

Investment accounts create freedom.

Insurance protects income.

Structure protects behavior.

Read: [Doctor Net Worth vs Financial Freedom: Why They’re Not the Same Thing]

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

The 7% rule assumes a long-term average annual market return of about 7% after inflation. It’s a planning assumption—not a guarantee—and actual results depend on asset allocation, fees, and market cycles.

Retirement accounts offer tax advantages but restrict access, while investment accounts offer full flexibility with no tax shelter. Doctors typically use retirement accounts for long-term wealth and investment accounts for liquidity and early access.

No, an investment account is not “better,” just different, because it trades tax advantages for flexibility. Doctors usually need both to balance taxes, cash flow, and long-term goals.

A Roth IRA provides tax-free growth and withdrawals, while a brokerage account offers unlimited access but taxable gains. Roth IRAs are best for long-term retirement wealth; brokerage accounts are better for flexibility and non-retirement goals.

Because retirement accounts let your investments compound without annual tax drag. Over long careers, this tax advantage can add hundreds of thousands of dollars compared to investing in the same assets in a taxable account.

Most doctors need enough disability insurance to replace 60–70% of gross income. Insurance specific to a medical specialty is very important. Generic policies may not protect your medical income.

Doctors get the best returns by filling tax-advantaged retirement accounts first. Then they use investment accounts for flexibility. This layered approach balances tax efficiency with access.

Investment accounts let you access money and fund early retirement. Retirement accounts limit this access. Together, they prevent forced withdrawals and reduce long-term tax pressure.

Doctors should consider time horizon, tax bracket, need for liquidity, and career stability. The right choice changes as income and goals evolve.

Retirement accounts save on taxes but limit access. Investment accounts give more flexibility but increase tax risk. Doctors need both to build durable wealth.

Retirement accounts lower or eliminate taxes on growth, while investment accounts shift tax timing and flexibility. Strategic use of both smooths lifetime tax liability and supports financial independence.