Doctors who want other options besides a 401(k) should look at IRAs, HSAs, taxable brokerage accounts, real estate, and defined benefit retirement plans. When a 401(k) reaches its contribution limit or is not flexible, these options let doctors keep saving for retirement with different tax benefits and risks.

The right mix depends on income type (W-2 vs 1099), practice ownership, time horizon, and how much control you want over investments—but every physician has viable paths beyond a traditional 401(k).

This guide is written for physicians and medical professionals who feel boxed in by employer plans and want real retirement planning options, not generic advice.

The options below show how doctors actually save for retirement. They come from banks, research focused on doctors, and IRS rules for retirement plans.

You’ll walk away knowing:

- Which 401k alternatives exist

- When each option makes sense

- How doctors combine them into a single strategy

- Where the tradeoffs and risks live

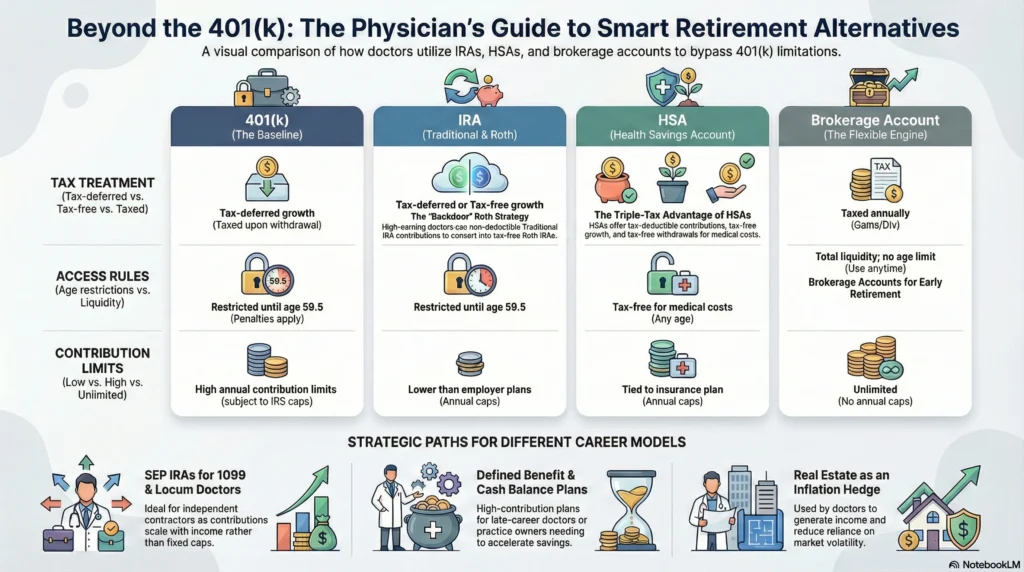

Traditional IRA as a 401(k) Alternative

A Traditional IRA is one of the most common 401k investment alternatives because it allows tax-deferred retirement savings outside an employer plan. You open it independently, control the investments, and decide how it fits into your broader retirement plans.

Many physicians earn too much to deduct contributions, but that doesn’t make the account useless. People often make non-deductible Traditional IRA contributions on purpose. They use these contributions to convert to Roth IRAs, especially when they earn a lot later in their careers.

According to Diamond Credit Union, IRAs are often the next most popular retirement savings option after a 401(k) Plan, precisely because they operate independently of employer benefits and expand tax flexibility

This option works best if you:

- Want control over investment options

- Are planning advanced tax strategies

- Need flexibility beyond employer rules

The tradeoff is lower contribution limits compared to employer plans, which is why Traditional IRAs are rarely used alone by doctors.

Roth IRA for Tax-Free Growth

A Roth IRA flips the tax equation. You pay taxes now, and qualified withdrawals—including earnings—are tax-free later. For physicians who expect high future income or want tax diversification, this matters.

Diamond Credit Union also highlights that Roth IRAs differ from Traditional IRAs through after-tax contributions and tax-free withdrawals, making them powerful tools for long-term retirement savings and flexibility

Even though income limits block many doctors from direct contributions, Roth IRAs still appear in physician retirement plans through structured conversions.

This option fits best if you:

- Want tax-free withdrawals later

- Expect rising tax rates

- Are building multiple retirement accounts

The limitation isn’t value—it’s access. That’s why Roth IRAs are usually paired with other strategies.

SEP IRAs for Self-Employed and 1099 Physicians

SEP IRAs are tailor-made for physicians with independent income streams. Locum tenens doctors, consultants, and practice owners often rely on SEP IRAs because contributions scale with income rather than fixed caps.

According to Fidelity, SEP IRAs are valuable retirement plan alternatives for self-employed professionals, allowing higher contributions while remaining easy to administer

SEP IRAs make sense when:

- Income fluctuates

- You want simplicity

- You don’t need Roth treatment

The tradeoff is lack of tax-free withdrawals and less flexibility once income drops.

SIMPLE IRA for Small Medical Practices

SIMPLE IRAs exist for smaller practices that want structured retirement plans without the cost of a full employer-sponsored retirement plan.

They allow both employee contributions and employer matching contributions, which helps retain staff while building retirement savings.

Fidelity also highlights SIMPLE IRA structures as practical retirement plans for small teams with modest administrative needs

They’re best when:

- You employ fewer people

- You want predictable setup

- You’re not ready for larger pension plans

Contribution limits are lower, so growing practices often outgrow SIMPLE IRAs.

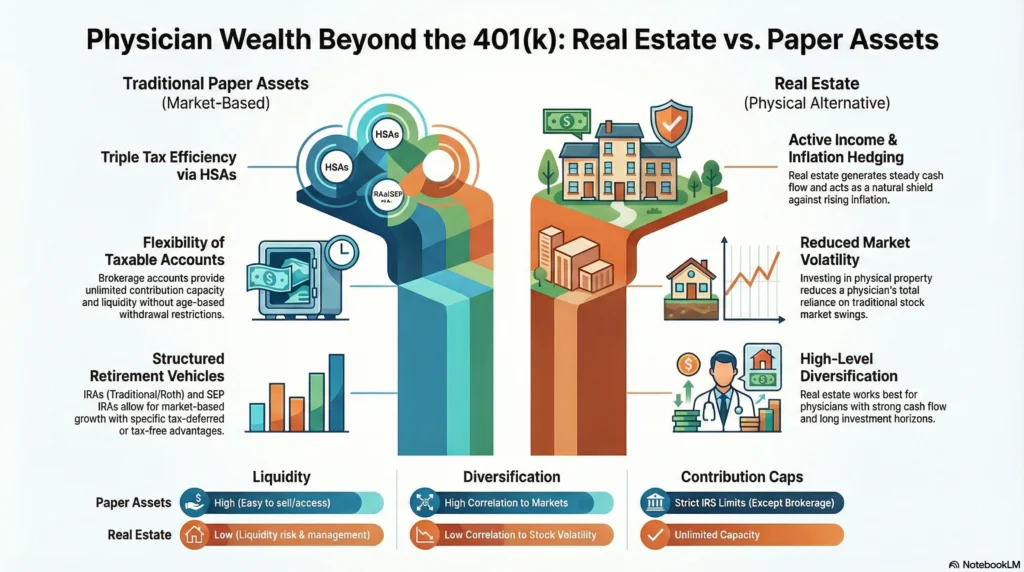

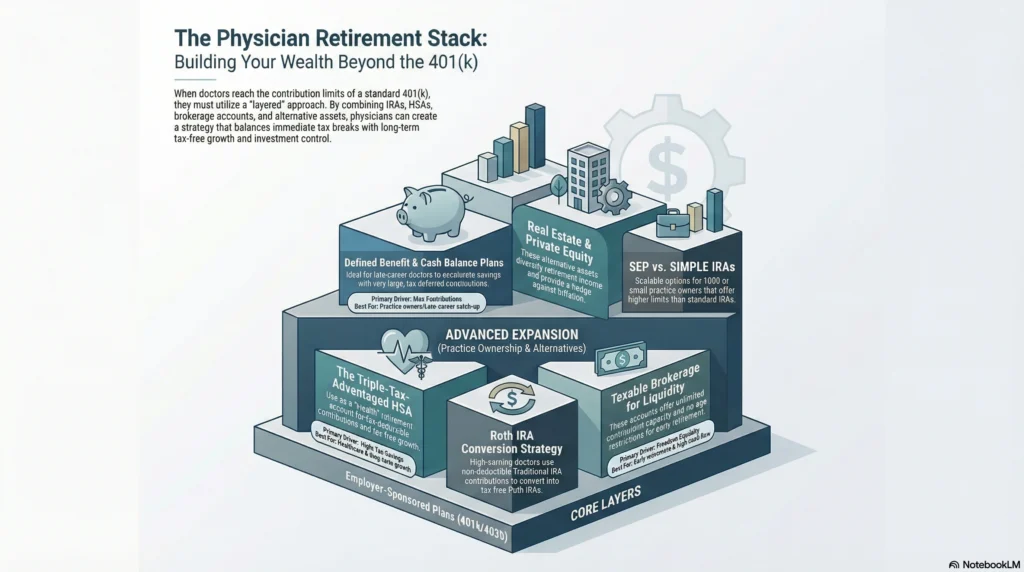

Health Savings Account (HSA) as a Stealth Retirement Account

A Health savings account (HSA) is one of the most tax-efficient retirement accounts available—yet many doctors underuse it.

HSAs allow:

- Tax-deductible contributions

- Tax-free growth

- Tax-free withdrawals for qualified medical costs

Fidelity explains that HSAs can act as long-term retirement savings vehicles, especially for healthcare expenses in retirement

This option fits physicians who:

- Can pay current medical costs from cash flow

- Want future healthcare coverage

- Already max other retirement plans

Eligibility depends on your insurance plan, which is the main limitation.

Taxable Brokerage Accounts for Flexible Investing

Brokerage accounts don’t offer tax deferral—but they offer something many retirement plans don’t: freedom.

Titan Wealth International notes that investment (brokerage) accounts provide unlimited contribution capacity and no age restrictions, making them flexible retirement savings alternatives

Doctors use brokerage accounts when:

- Retirement accounts are maxed

- Early retirement is a goal

- Liquidity matters

The tradeoff is annual taxation on dividends and capital gains, which can slow compounding without planning.

Real Estate as a 401(k) Alternative

Real estate remains one of the most common alternative assets physicians use to diversify retirement savings.

Real estate investment can:

- Generate income

- Hedge inflation

- Reduce reliance on market volatility

Titan Wealth International includes real estate investment as part of diversified retirement planning outside traditional employer plans

Real estate works best for doctors with:

- Strong cash flow

- Long time horizons

- Willingness to manage or outsource

Liquidity risk and time commitment are the main downsides.

Defined Benefit and Cash Balance Plans

Defined benefit plans, like cash balance plans, let doctors save very large amounts for retirement. This is especially true for doctors later in their careers.

Investopedia notes that pension plans and defined benefit options still exist outside standard 401(k) Plans, particularly through practice ownership

These plans make sense if:

- Income is stable

- Retirement acceleration is needed

- You own or control the practice

They require commitment and professional administration.

Alternative Assets Beyond Traditional Markets

Many doctors eventually allocate a portion of retirement savings to alternative assets such as private equity, private credit, or specialized funds.

Alternative assets can help spread out investments but they also make things more complicated. They’re best used once core retirement plans are solid.

This approach suits physicians with:

- High net worth

- Higher risk tolerance

- Long investment horizons

How Doctors Combine Multiple 401k Investment Alternatives

Most physicians don’t choose one alternative. They layer them.

A common structure looks like:

- Employer 401(k) Plan

- IRA-based strategies

- Health savings account

- Brokerage investing

- Real estate investment or defined benefit plans

This layered approach balances tax advantages, liquidity, and long-term growth.

If you’re mapping next steps, explore:

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Yes, there can be better alternatives to a 401k depending on your income, employment structure, and tax goals. IRAs, HSAs, brokerage accounts, real estate, and defined benefit plans can outperform or complement a 401k when contribution limits, fees, or investment restrictions become a bottleneck.

You need alternatives to a 401k when contribution limits, limited investment options, or high plan fees prevent further efficient retirement savings. This is common for physicians who earn high incomes, change employers often, or want more control over asset allocation and liquidity.

The best 401k alternatives for doctors typically include IRAs (Traditional and Roth), Health Savings Accounts, taxable brokerage accounts, real estate, and defined benefit or cash balance plans. Which ones make sense depends on whether you’re employed, self-employed, planning early retirement, or optimizing taxes.

Alternative investments outside a 401k include real estate, private equity, brokerage accounts, HSAs, and pension-style plans like cash balance plans. These options let you invest beyond your employer's retirement plans. They also meet different tax and cash needs.

When both a 401k and Roth IRA are maxed out, doctors often use HSAs, taxable brokerage accounts, real estate investments, and defined benefit plans. These alternatives remove contribution caps and offer flexibility, though they may trade tax advantages for access or control.

You diversify retirement savings outside a 401k by spreading assets across IRAs, brokerage accounts, real estate, and alternative assets. This reduces reliance on a single account type and balances tax treatment, liquidity, and risk.

401k plans offer tax deferral and employer matching but limit investment choice and annual contributions. Other retirement accounts—like IRAs or HSAs—offer more control or tax flexibility, while brokerage accounts trade tax benefits for unrestricted access.

No account guarantees better returns than a 401k—the returns depend on the investments inside the account. However, brokerage accounts, real estate, and private investments can outperform if they allow better asset selection and cost control.

Roth IRAs offer tax-free withdrawals in retirement, while 401ks typically offer tax deferral upfront. Roth IRAs are more flexible long term, but have lower contribution limits and income restrictions compared to 401k plans.

A Solo 401(k) is a retirement plan for self-employed individuals with no full-time employees other than a spouse. It matters because it allows much higher contributions than IRAs and combines features of both employee and employer retirement plans.