Good returns for beginners come from long-term, diversified investing that outpaces inflation not from picking winning stocks or timing the market.

For doctors and physicians new to investing, good returns depend on time frame, cash flow, and risk tolerance. But the basics stay the same: be consistent, keep it simple, and be patient.

If you’re overwhelmed, that’s expected. Medical training teaches you how to save lives, not how to build an investment portfolio. This guide removes the noise and gives you a clear, step-by-step framework to invest confidently without turning finance into a second career.

By the end, you’ll know where to invest money to get good returns as a beginner, how to avoid common traps, and how to build an investment strategy you can actually stick with.

What “Good Returns” Actually Mean for Beginners

For beginners, good returns mean steady, repeatable growth that compounds over time, not fast wins or flashy gains.

A realistic long-term investment return for a diversified portfolio often falls in the 7–10% range. That may sound modest. But over decades, it’s transformative.

This matters because cash alone quietly loses purchasing power.

According to U.S. Bank, investing is a long-term strategy that helps money grow faster than inflation, while savings accounts typically cannot match inflation-adjusted returns

That distinction is critical when you’re thinking about your financial future, retirement plan, or even optional early flexibility.

Before You Invest: Set Clear Financial Goals

Every strong investment strategy starts with clarity.

Before choosing mutual funds or index funds, you need to define:

- What the money is for

- When you’ll need it

- How flexible it must be

Vanguard emphasizes this step because financial goals determine everything else—from asset allocation to risk tolerance.

Vanguard highlights the importance of starting with clear financial goals and choosing investments based on time horizon and risk tolerance

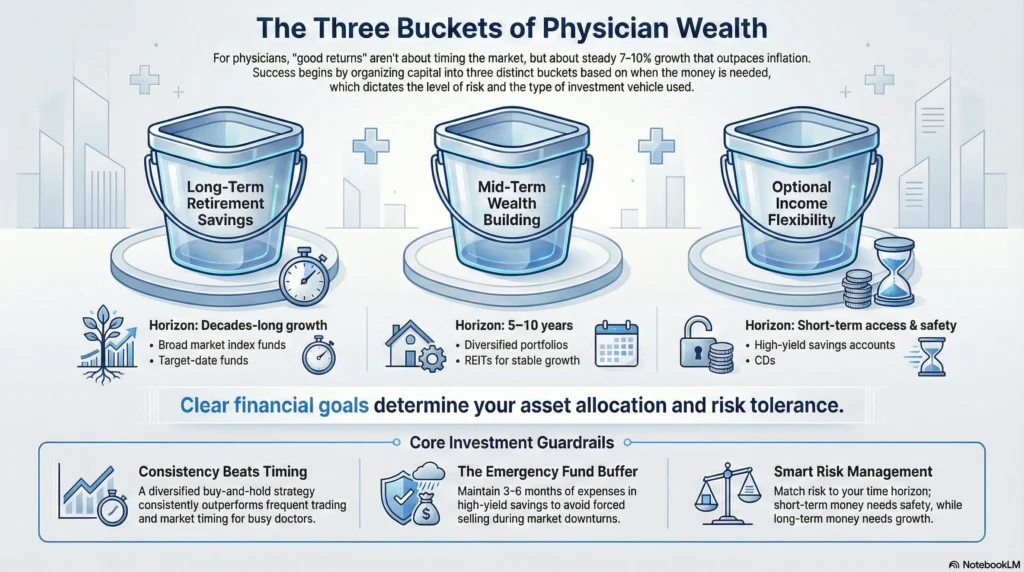

For most doctors, early investment goals fall into three buckets:

- Long-term retirement savings

- Mid-term wealth building

- Optional income flexibility later in life

Without this clarity, even good investments feel stressful.

Read: [What to Do After Maxing Out 401k]

Understanding Risk (And Why Avoiding It Completely Is a Mistake)

Many physicians associate risk with danger.

In investing, risk simply means short-term price movement, not permanent loss.

Avoiding all risk usually means:

- Holding too much cash

- Overusing savings vehicles

- Losing purchasing power over time

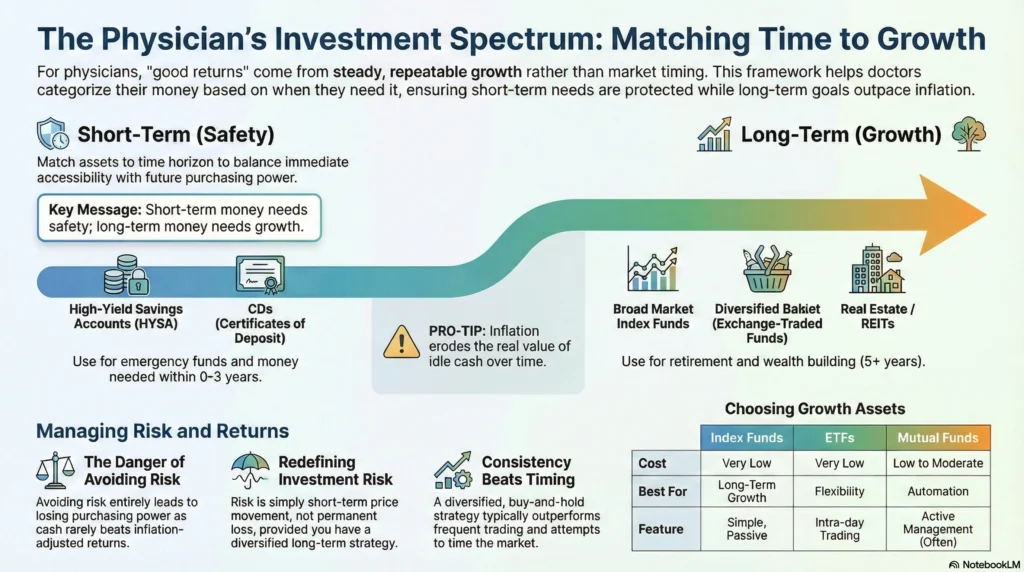

The goal isn’t to eliminate risk. It’s to match risk to your risk tolerance and time horizon.

Short-term money needs safety.

Long-term money needs growth.

That balance is where smart investing lives.

Why Consistency Beats Timing the Market

Trying to time the stock market is one of the most common beginner mistakes.

Even professional investors struggle with it.

Investopedia emphasizes that long-term diversified investing is more suitable than frequent trading for most investors

For doctors with demanding schedules, this is good news.

You don’t need perfect timing—just consistency.

Safe & Low-Risk Investment Options for Beginners

“Safe” doesn’t mean zero volatility.

It means low complexity and low chance of permanent loss.

Beginner-friendly options include:

- Broad market index funds

- Exchange-traded fund (ETF) portfolios

- Target-date funds

- High-yield savings accounts for short-term needs

Bankrate outlines that beginners can start with conservative options like high-yield savings accounts and CDs, then scale into mutual funds, ETFs, and stocks

This spectrum lets you match investments to comfort level.

Getting Started With the Stock Market (The Simple Way)

You don’t need to analyze balance sheets or predict earnings.

The simplest way into the stock market is through owning the market itself.

Broad index exposure gives you:

- Built-in diversification

- Lower fees

- Less emotional decision-making

The S&P 500, for example, represents 500 of the largest U.S. companies and reflects the overall market index many long-term investors use as a benchmark.

Fractional investing removes the minimum account balance requirement completely.

Read: [401k Investment Alternatives]

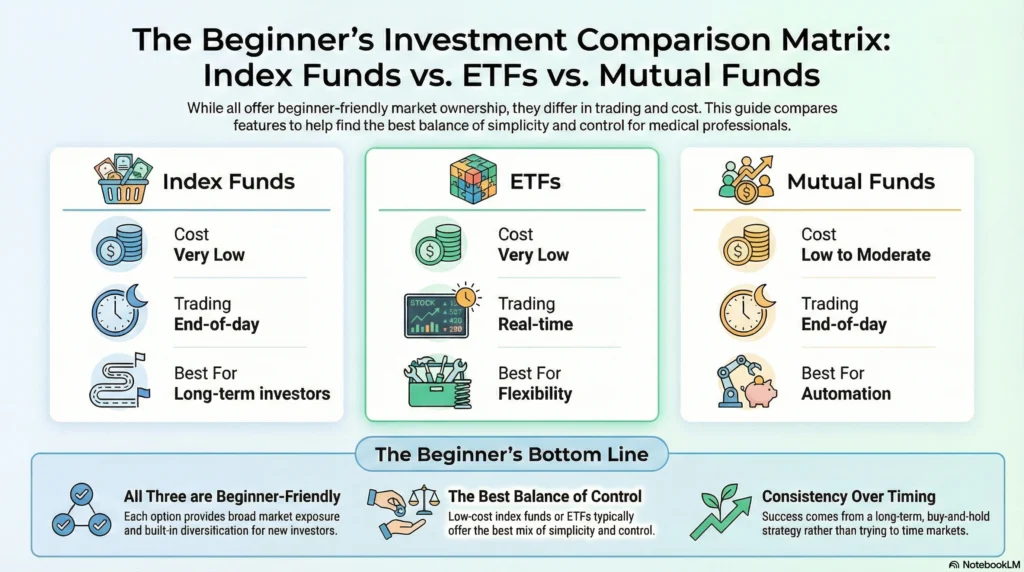

Index Funds vs ETFs vs Mutual Funds (What Beginners Should Choose)

This comparison trips up most beginners. Here’s a clean breakdown:

Feature | Index Funds | ETFs | Mutual Funds |

|---|---|---|---|

Cost | Very low | Very low | Low to moderate |

Trading | End-of-day | Real-time | End-of-day |

Best for | Long-term investors | Flexibility | Automation |

Beginner-friendly | Yes | Yes | Yes |

Index funds and ETFs often track the same market index. The difference is how they trade.

For most beginners, low-cost index funds or ETFs offer the best balance of simplicity and control.

Should Beginners Consider Real Estate or REITs?

Real estate sounds attractive, but direct ownership requires:

- Time

- Capital

- Management skills

For beginners, REITs provide real estate exposure without landlord stress.

This method lets you invest in real estate while keeping your investment portfolio easy to manage.

Direct property ownership often makes more sense later—after your core portfolio is stable.

The Power of Diversification (Don’t Bet on One Horse)

Diversification spreads risk across:

- Companies

- Industries

- Asset classes

A diversified portfolio reduces the chance that one bad decision ruins long-term outcomes.

It’s the seatbelt of investing.

How Compound Interest Does the Heavy Lifting Over Time

Compound interest means your returns start earning returns.

Time matters more than brilliance.

Starting early—even imperfectly—dramatically increases the value of your investment over decades.

This is why consistency beats intensity.

Emergency Fund: The Unsung Hero of Good Returns

Before investing aggressively, build an emergency fund.

Fulton Bank recommends maintaining 3–6 months of expenses in an emergency fund to avoid forced selling during market downturns

An emergency fund belongs in high-yield savings accounts, not the stock market.

This single step protects your investment return more than any stock pick.

DIY Investing vs Robo-Advisors vs Financial Advisors

Three valid paths exist:

- DIY: Lowest cost, requires discipline

- Robo-advisors: Automated, beginner-friendly

- Advisors: Personalized, useful as complexity grows

Many doctors start DIY or robo, then layer advice later.

There’s no “right” path—only the one you’ll actually follow.

A Simple Beginner Investment Playbook You Can Follow

Let me be honest with you.

Investing alone won’t fix burnout.

Maxing out accounts won’t automatically give you freedom.

And chasing returns without clarity often leaves doctors feeling more trapped, not less.

I wrote Freedom for Doctors because I lived this tension myself.

As physicians, we’re taught how to earn—but not how to design a life. We work harder, save more, invest more… and still feel behind, exhausted, or boxed into choices we didn’t consciously make.

This book isn’t about beating the market.

It’s about escaping the doctor’s trap.

Inside Freedom for Doctors, I walk you through how investing fits into a much bigger picture, one that includes your time, health, purpose, and relationships. Not theory. Not hype. Real frameworks that physicians can actually apply.

You’ll learn:

- Why many high-earning doctors still feel financially insecure

- How to stop confusing income with independence

- How to use investing as a tool for choice, not just retirement

- Practical ways to build financial independence without sacrificing your well-being

Whether you’re a medical student, early-career physician, or approaching retirement, the goal is the same: to reclaim control over your life—not just your money.

If this guide helped you understand where to invest money to get good returns as a beginner, the book helps you answer the deeper question:

“What am I investing for?”

Freedom for Doctors is a roadmap for physicians who want more than endless work, mounting burnout, and delayed fulfillment. It’s about redefining success on your own terms and building a financial life that actually supports that vision.

If you’re ready to stop treating investing as a standalone task and start using it as part of a freedom-first plan, this is the next step.

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

The best investment for beginners is a diversified mix of low-cost index funds or ETFs. These provide broad market exposure, lower risk than individual stocks, and require minimal ongoing management.

You can start investing with as little as $50–$100. Many platforms allow fractional shares and low or no account minimums, making investing accessible even with small amounts.

Saving is better for short-term needs, while investing is better for long-term growth. Ideally, you do both: keep an emergency fund in savings and invest money you won’t need for several years.

Yes, you can invest in stocks with little money using fractional shares or funds.

This allows you to own portions of companies or diversified funds without needing large upfront capital.

The safest investments for beginners include high-yield savings accounts, government bonds, and broad-market index funds. Each offers lower volatility, though returns vary depending on risk and time horizon.

Stocks have historically delivered the best long-term returns. However, they also come with short-term volatility, which is why diversification and time in the market matter more than picking winners.

You should invest as much as you can consistently after covering essentials and emergency savings. For most beginners, starting with 10–20% of income is realistic and effective over time.

Beginners diversify by spreading money across stocks, bonds, and different markets. Using broad-market funds automatically achieves this without needing complex strategies.