Physician net worth by age varies widely, and most doctors are not as financially ahead as their income might suggest, especially early and mid-career. This gap exists because of long training, delayed earnings, high student loan payments, lifestyle choices, and uneven wealth building habits. The result is that two physicians of the same age can have dramatically different financial security even if their salaries look similar on paper.

This BOFU guide is written for doctors who want clarity, not comparison anxiety. You will see realistic benchmarks, understand why those numbers look the way they do, and learn what actually matters for long-term financial independence at each stage of a medical career.

Average vs. Median Net Worth

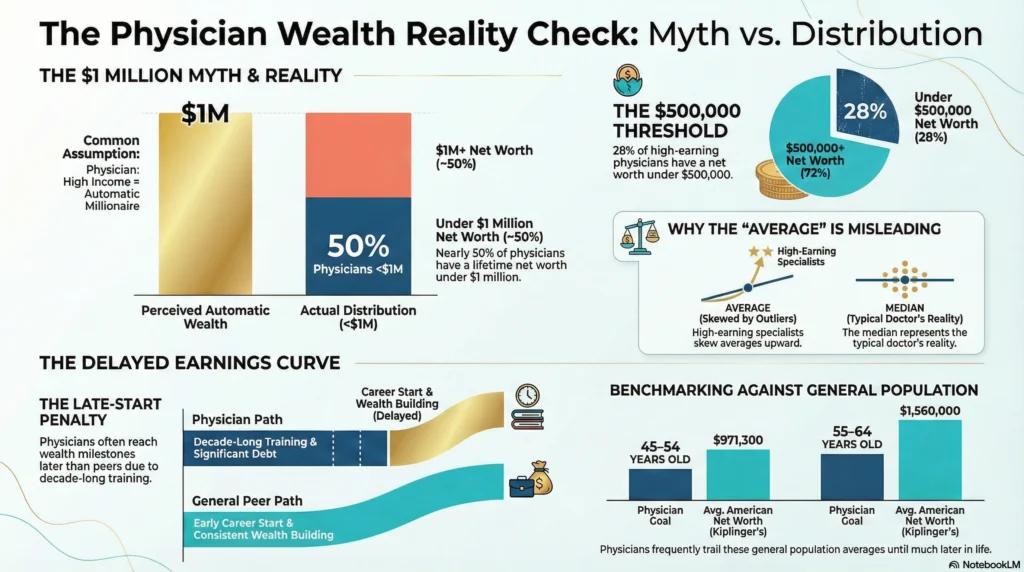

When physicians talk about net worth, most comparisons are misleading. The “average physician” number is skewed upward by a small group of very high earners and long-tenured specialists. The median tells a more accurate story of where most doctors really stand.

GlobalRPH’s physician finance analysis shows that about 28 percent of physicians have a net worth under $500,000, despite high incomes. Nearly half of physicians have less than $1 million in lifetime net worth, and negative net worth early in careers is common due to medical school debt that often exceeds $200,000. These figures surprise many medical students and early attendings who assume wealth accumulation is automatic once income rises.

Context matters even more when comparing physicians to the general population. Kiplinger’s average net worth by age data shows that Americans aged 45–54 average about $971,300, while those 55–64 average roughly $1.56 million. Many physicians reach these levels later, not because they failed, but because their earnings curve starts much later.

Milestones by Age Group

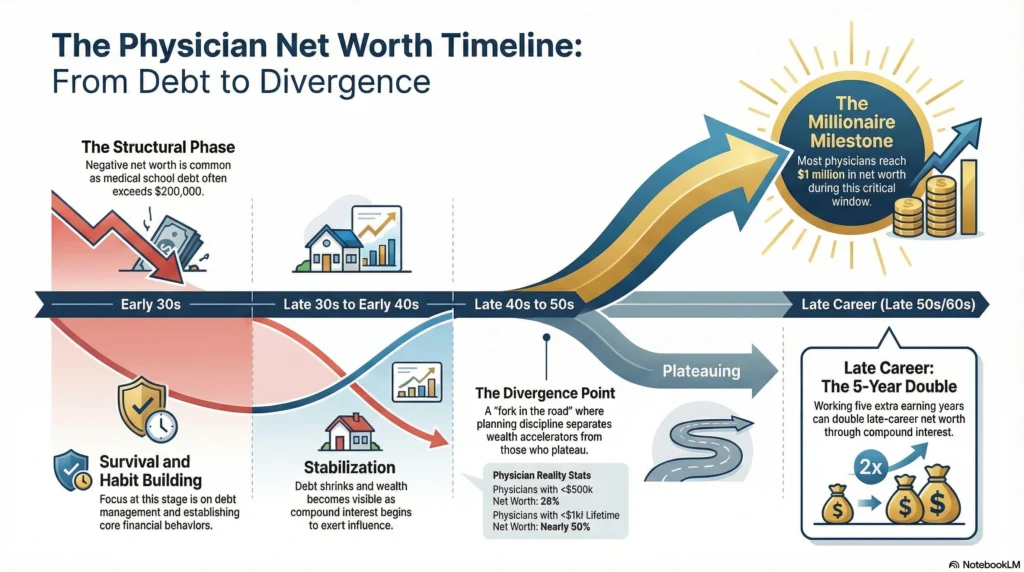

In your early 30s, negative net worth is common. Medical students and residents are often balancing debt, modest pay, and delayed saving. This is not a personal finance failure. It is structural.

By the late 30s and early 40s, the average physician begins to stabilize. Student loan payments shrink, retirement accounts start compounding, and wealth building becomes visible for the first time. This is where compound interest begins to matter, even if balances still feel small.

In the late 40s and 50s, divergence becomes obvious. Some physicians accelerate toward a net worth of $1 million, while others plateau. The difference is rarely income alone. It is driven by retirement planning discipline, investment strategies, and financial literacy.

Factors Influencing Physician Net Worth

Income and Specialty

The average physician income sits around $339,000 annually, with specialists earning more. Yet income alone does not guarantee financial security. High earners often increase spending faster than savings, delaying wealth accumulation.

According to GlobalRPH’s physician myth breakdown, many high-income doctors still struggle to build net worth because peak income arrives late, usually in their 30s, after a decade or more of training. This compressed earning window makes early mistakes more costly.

Financial Planning Strategies

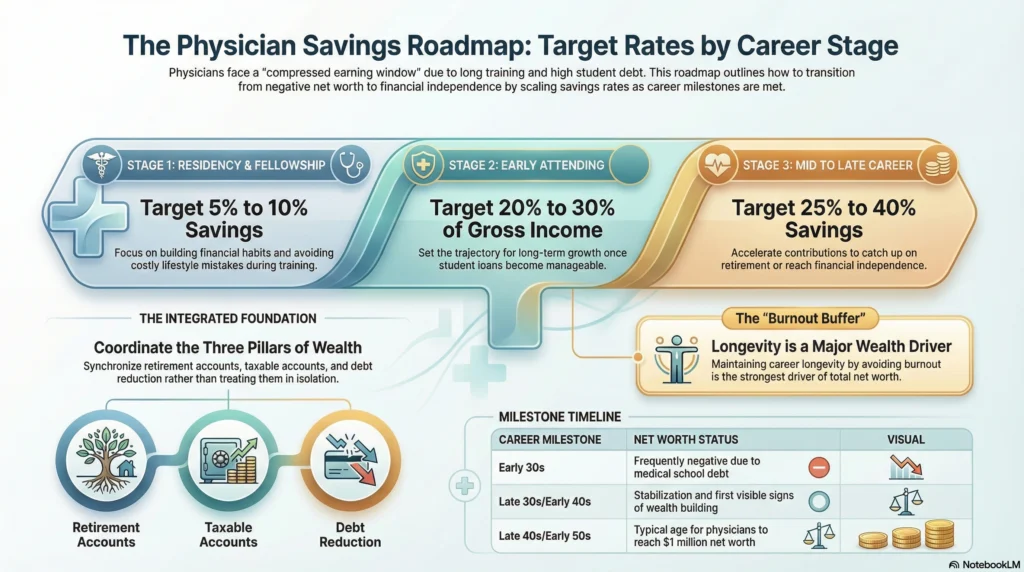

Doctors who build lasting wealth usually follow a written financial plan. They coordinate retirement accounts, taxable accounts, insurance, and debt reduction rather than treating each decision in isolation. This planning reduces stress and improves long-term investment returns by avoiding emotional decisions.

Physicians who skip planning often overfund a single account or chase returns without understanding risk. Read: [Savings Account vs Investing: What Doctors Should Do With Extra Cash] to see how idle cash decisions affect net worth growth.

Impact of Career Longevity

Career length matters more than most doctors realize. Those who maintain flexibility and avoid burnout often work longer by choice, which dramatically improves physician retirement outcomes. Even five extra earning years can double late-career net worth through continued contributions and compound interest.

Investment Approaches

Investing regularly and in different ways works better than investing only sometimes. Doctors who rely on retirement accounts, taxable accounts, and simple asset allocation tend to outperform those chasing complex products. Read: [Best Cash Flow Investments for Doctors Who Want Predictable Income] for examples of stability-focused approaches.

Myths and Misconceptions

Income Assumptions

A common myth is that high income equals automatic wealth. Data shows otherwise. Nearly half of physicians never reach a net worth of $1 million. Income enables wealth building, but behavior determines outcomes.

Financial Security Misunderstandings

Another misconception is equating cash flow with safety. High income without savings is fragile. True financial security comes from assets that do not depend on working more hours. This distinction becomes critical as retirement age approaches.

Importance of Early Financial Planning

Benefits of Early Saving

Starting early matters even if contributions are small. Compound interest rewards time more than intensity. A physician who saves modestly in their first attending years often outpaces peers who wait for “perfect timing.”

Financial planning for doctors consistently shows that early habits matter more than late optimization. Read: [Financial planning for doctors] to see how early structure compounds into long-term stability.

Compounding and Investments

Compound interest works quietly but powerfully. Each contribution builds on the last, especially inside tax-advantaged retirement accounts. Missing early years is difficult to recover, even with higher income later.

Preparing for Retirement

Retirement Age Trends by Specialty

Physician retirement age varies by specialty and health. Procedural specialties often retire earlier due to physical demands, while cognitive specialties work longer. Planning must account for this reality rather than assume a universal timeline.

Developing a Retirement Plan

Physician retirement planning is complex because lifestyle goals, cost of living, and family needs differ widely. MDM’s physician retirement guidance emphasizes that target net worth numbers must reflect personal context, not generic rules.

A solid retirement plan integrates retirement accounts, taxable accounts, and predictable income sources. Read: [Where Doctors Should Invest After Maxing Out Their 401k and Roth IRA] to understand how advanced saving fits into long-term planning.

Role of Social Security and Pensions

While Social Security is a smaller portion of physician retirement income, it still provides baseline stability. Some physicians also retain pension-like benefits through academic or hospital systems, which should be integrated into the broader financial plan.

Protecting Income

Necessity of Disability Insurance

Your earning power is your largest asset. Disability insurance protects your income. It is especially important early and in the middle of your career. Without it, years of wealth building can unravel overnight.

Insurance Options and Considerations

Coverage should match specialty risk and income trajectory. Poor coverage decisions undermine financial security more than most investment mistakes.

Strategies for Wealth Growth

Diversifying Investments

Diversifying your investments lowers ups and downs. It helps you build wealth steadily. Physicians who spread investments across retirement accounts, taxable accounts, and cash-flow assets are more resilient to market swings.

Balancing Risk and Safety

The goal is not maximum return but sustainable progress. Taking balanced risks helps you become financially independent. It stops you from making emotional choices during bad times.

How a Financial Advisor Fits and When

Many physicians reach a point where information overload becomes the problem. Knowing what to do next matters more than knowing everything.

This is where guidance should feel clarifying, not sales-driven. Over the years, we built Medicine and Money Show to fill that gap with education first.

Some doctors prefer a structured path.

If that resonates,

- 📘 Our book Freedom for Doctors offers a physician-written roadmap to financial independence, personal balance, and long-term financial security. Others want to test ideas first.

- 📥 Our free LIFTOFFNOW Physician Financial Flight Plan breaks the framework down without commitment.

- 📞 And if you want to talk through your situation, a short clarity call can help you decide next steps without pressure.

- 🎧 Listen to the audio version of this guide while commuting or between shifts

For deeper context, Read: [Student Loan Repayment Strategies for Doctors: A Clear Plan for High-Income Physicians] to see how debt fits into the bigger picture.

FAQ

Most physicians who reach a net worth of $1 million do so in their late 40s to early 50s, not earlier. This delay is driven by long training years, delayed peak income, and high student loan balances early in their careers.

During residency or fellowship, saving even 5% to 10% of income is enough to build habits and financial literacy. The main goal at this stage is survival, avoiding lifestyle inflation, and preventing financial mistakes rather than aggressive wealth accumulation.

Early attending physicians should aim to save 20% to 30% of gross income once loans are manageable. This is the most important phase for setting the trajectory of long-term net worth growth.

Mid to late career physicians often need to save 25% to 40% of income, especially if they want to catch up on retirement planning or pursue financial independence. Higher income does not eliminate the need for disciplined saving.