You typically need around 25 times your expected annual retirement expenses saved by age 50, which for many physicians lands in the multi-million-dollar range. The exact number changes with lifestyle, taxes, and location, but the structure of the goal does not. You must replace income for decades, cover healthcare costs before Medicare, and fund a long life after clinical work ends.

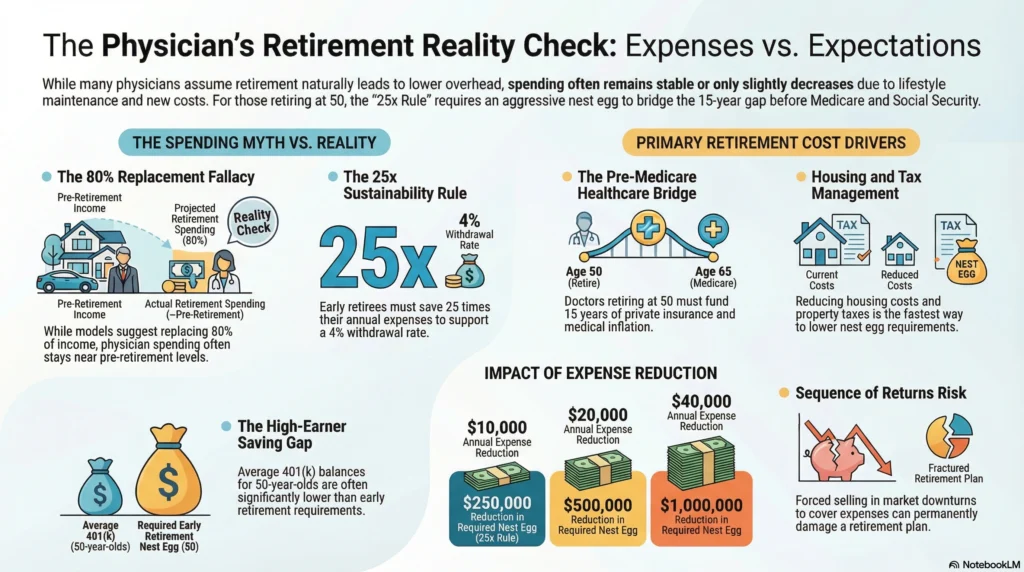

Many planning models suggest retirees aim to replace about 80 percent of preretirement income when estimating needs. A widely used rule multiplies expected annual expenses by 25 to estimate the required nest egg under a 4 percent withdrawal framework. That math alone explains why early retirement requires more aggressive retirement savings than traditional timelines.

This guide is built for physicians in peak earning years who want a clear path to that number. Not theory. Not vague motivation. Concrete milestones that increase net worth and push you toward financial independence before 50.

Navigating Retirement Account Types

Your strategy begins with where money lives, not just how much you save. Doctors often juggle multiple retirement accounts but rarely use them strategically.

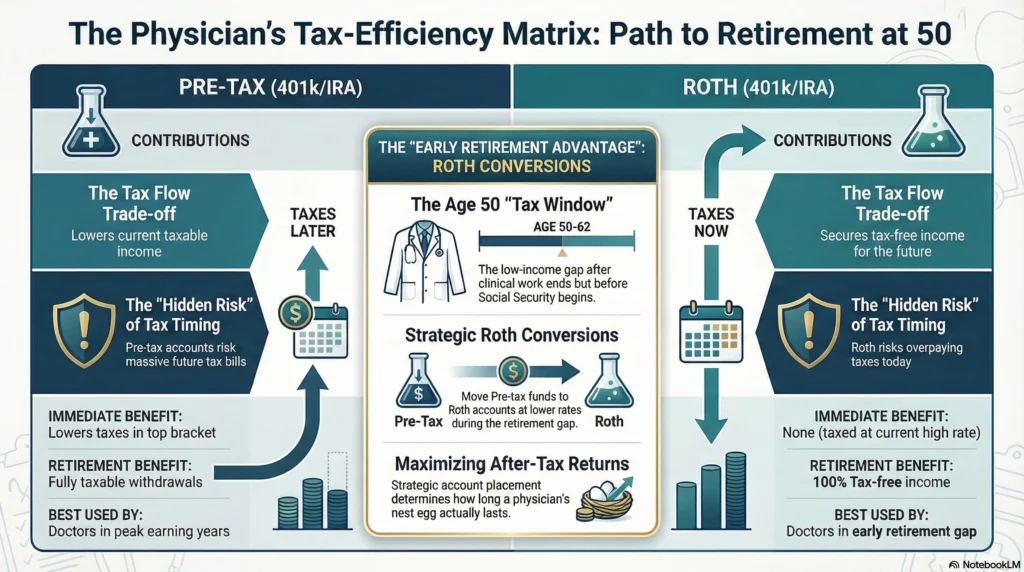

Pre-Tax vs. Roth Retirement Accounts

Account Type | How Taxes Work | When It Helps Most | Hidden Risk if Ignored |

|---|---|---|---|

Pre-tax 401(k) / traditional IRA | Lowers taxes now, taxed later | High earners in top tax bracket | Large taxable withdrawals later |

Roth IRA / Roth 401(k) | Taxed now, tax free later | Early retirement years with low income | Paying high taxes now if poorly timed |

High earners benefit from lowering taxes today through pre-tax contributions. But retiring at 50 creates a long window before social security benefits start. Having Roth IRA money gives tax flexibility during that gap.

Contribution limits matter here. Physicians who do not max employer plans and IRAs every year leave thousands in tax-advantaged growth on the table. Over a 15 to 20 year horizon, missed contribution limits can cost hundreds of thousands in retirement savings.

Average 401(k) balances for people in their 50s often sit well below what early retirement requires, sometimes under $200,000 and in many cases under $635,000 . That gap shows how much more physicians targeting 50 must accumulate.

Read: [How Much Do Doctors Need in a 401k to Retire Comfortably?]

Key Tax Advantages in Peak Income Years

• Lowers taxable income in top tax bracket years

• Increases net investable capital

• Reduces lifetime tax drag

• Accelerates retirement savings compounding

• Creates flexibility for Roth IRA conversions later

Doctors often sit in top brackets. Reducing taxable income through pre-tax retirement accounts and a traditional IRA lowers current taxes while boosting retirement savings. This is not optional for an early retirement target. It is structural.

If you earn $400,000 and fail to maximize contribution limits, you are choosing higher taxes instead of compounding. Over 10 to 15 years, that decision alone can shrink your nest egg by seven figures.

Roth Conversions and Their Benefits

Early retirement creates a tax window. Use it.

Advantages of converting traditional IRA money to Roth IRA after leaving work:

• Pay tax at lower rates before social security begins

• Reduce required taxable withdrawals later

• Lower lifetime tax burden

• Provide tax-free income flexibility

• Protect retirement savings against future tax increases

Without conversions, physicians risk high taxable income later, shrinking net worth faster than planned.

Tax Planning Strategies

Developing a Tax-Efficient Portfolio

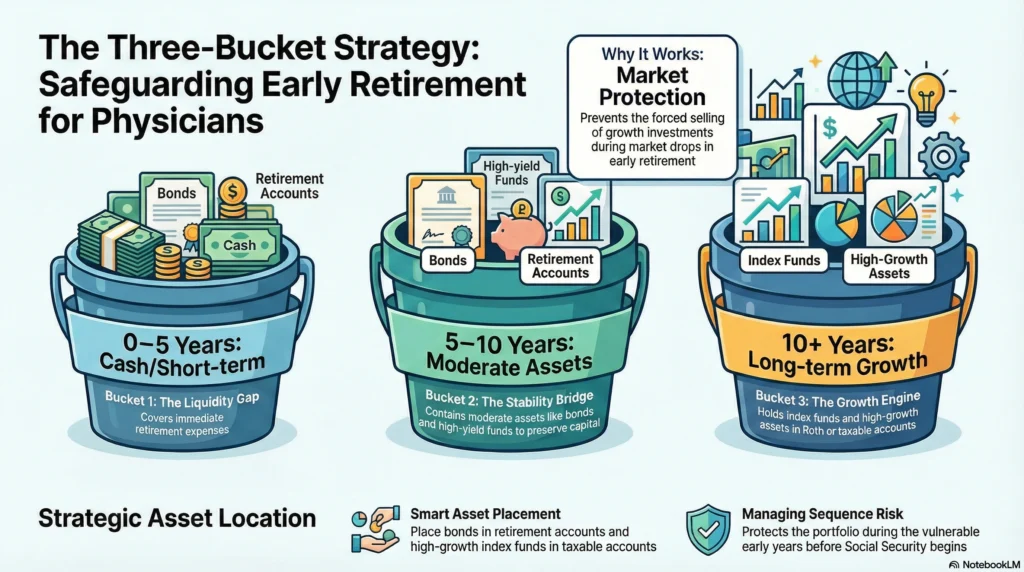

A tax-efficient portfolio means putting each asset in the right account.

How it works:

• Bonds and high-yield funds go inside retirement accounts

• Index funds with low turnover go in taxable accounts

• Roth IRA holds highest growth assets

• Taxable accounts focus on tax-efficient funds

Why it matters:

After-tax return, not the headline return, determines how long retirement savings last.

Where people fail:

They hold tax-inefficient assets in taxable accounts, increasing annual taxes and slowing compounding.

Implementing the “Three Bucket” Plan

This strategy organizes money by time horizon.

Bucket 1: Cash and short-term needs

Bucket 2: Moderate assets for 5 to 10 years

Bucket 3: Long-term growth investments

Why it works:

It prevents selling growth investments during market drops in early retirement. Forced selling in a downturn permanently damages retirement planning outcomes.

Who benefits most:

Doctors retiring before social security age who face sequence of returns risk.

Read: [How Do Doctors Retire Early? What Makes It Realistic (and What Doesn’t)]

Biggest Retiree Expenses and Cost Reduction

Housing Considerations and Cost Management

Housing is often the largest line item.

Smart moves:

• Pay off mortgage payments before retirement

• Downsize if current home exceeds needs

• Relocate to lower tax states

• Reduce property tax exposure

Each $10,000 reduction in annual expenses lowers required nest egg by $250,000 under the 25x rule.

Managing Healthcare Costs in Retirement

Doctors retiring at 50 must fund healthcare costs privately until Medicare.

Steps:

• Budget realistic insurance premiums

• Include out-of-pocket estimates

• Plan for rising medical inflation

• Use HSA funds strategically if available

Underestimating this category is a common retirement planning mistake.

Age-Based Saving Goals and Emergency Funds

Below is a practical framework physicians can use.

Age | Retirement Savings Target | Emergency Fund Target | Why This Stage Matters |

|---|---|---|---|

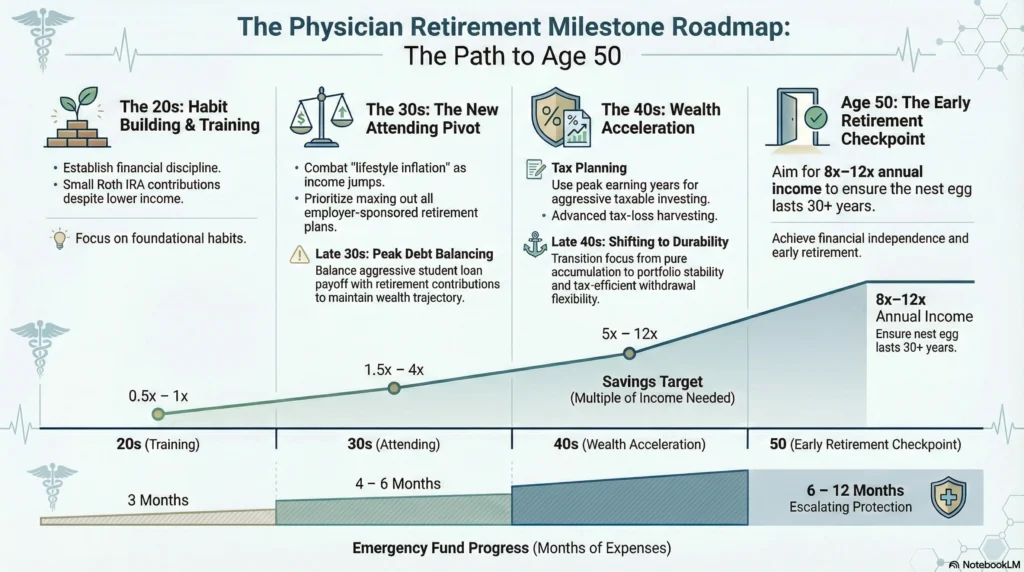

20s (training years) | 0.5 to 1x annual income | 3 months expenses | Habit building matters more than amount. Even small Roth IRA contributions establish compounding and financial discipline. |

Early 30s (new attending) | 1.5 to 2x income | 4–6 months expenses | Income jumps fast. Lifestyle inflation risk is high. This stage determines whether you build wealth or just upgrade spending. |

Late 30s | 3 to 4x income | 6 months expenses | Peak debt payoff years. Student loans, mortgage payments, and retirement accounts must be balanced carefully. |

Early 40s | 5 to 6x income | 6–9 months expenses | Catch-up phase. Savings rate, not investment return, drives net worth growth here. |

Age 50 goal | 6x+ income minimum, 8–12x ideal for early retirement | 9–12 months expenses | This is the checkpoint for early retirement feasibility. Falling short here means working longer. |

Planning benchmarks show saving about six times income by age 50 is a strong baseline age 50 retirement savings multiple. But physicians aiming for early retirement often need more because retirement savings must last longer and bridge the gap before social security benefits begin.

Emergency funds grow as responsibility increases. A physician with dependents, private practice overhead, or variable income needs more liquidity than a salaried hospital employee.

Setting Effective Saving Goals by Age

Saving strategy changes with career stage. The mistake many doctors make is applying the same approach at 32, 42, and 52. Each decade has a different job.

In your 20s, especially during medical school or residency, the focus is not large retirement savings. It is learning personal finance habits and avoiding destructive debt behaviors. Even small Roth IRA contributions matter. Starting early builds the psychological identity of an investor, not just an earner. Doctors who skip investing entirely during training often struggle to switch into saving mode once income rises.

In your 30s, income jumps dramatically. This decade sets the trajectory of your net worth. Retirement accounts must be maxed early, not at the end of the year after spending decisions are already made. Student loans should be structured intelligently, but not every extra dollar should go to debt if employer retirement matches or tax advantages are missed. This is also the decade where lifestyle creep can quietly block financial independence.

In your 40s, your income is likely at or near peak. This is the wealth acceleration window. Retirement savings contributions, taxable investing, and tax planning must work together. Doctors who under-save in this decade often find themselves with strong incomes but insufficient assets to retire early. The difference between retiring at 50 and 60 is often decided in these years.

In your late 40s approaching 50, the goal shifts from accumulation alone to durability. Your retirement planning now focuses on portfolio stability. It also focuses on tax positioning and withdrawal flexibility. At this stage, mistakes hurt more because there is less time to recover.

Check out: [Financial Freedom Calculator for Doctors]

Building and Maintaining an Emergency Fund

An emergency fund protects retirement savings from being interrupted by life. Without it, every unexpected event becomes a reason to stop investing or to use credit cards.

A physician should build an emergency fund in stages. First, aim for one month of expenses quickly. This creates immediate breathing room. Then grow it to three months while continuing retirement account contributions. After reaching that level, gradually expand to six to twelve months depending on job stability, practice structure, and family responsibilities.

Where you keep this fund matters. It should be in a high-yield savings account or money market account, not invested in the market. The purpose is stability, not growth. When markets fall, your emergency fund must remain intact so you do not sell investments at the worst time.

Maintaining the fund requires discipline. When you use part of it for a true emergency such as a medical emergency, job transition, or major repair, refilling it becomes the next financial priority before new investing goals. Many physicians build the fund once but fail to rebuild it after using it, leaving retirement savings exposed to the next disruption.

Understanding Medicare for Retirees

Medicare becomes a major pillar of healthcare coverage later in retirement. Before eligibility, physicians retiring at 50 must cover healthcare costs privately, which can be one of the largest expenses in early retirement.

Having Medicare later reduces uncertainty around major medical costs. It helps cover hospital stays, physician services, and other essential care. Without it, retirees rely fully on private insurance or self-funding, which can significantly increase annual expenses and stress retirement savings.

Even with Medicare, costs do not disappear. Premiums, supplemental plans, and out-of-pocket expenses still exist. Planning for Medicare means understanding that it reduces catastrophic risk, but it does not eliminate healthcare budgeting. Doctors who ignore this often underestimate how long their nest egg must last.

Read: [When Do Doctors Retire? Average Retirement Age for Physicians Explained]

Identifying and Prioritizing Outstanding Debts

Debt reduces flexibility in early retirement. A structured approach prevents debt from quietly extending your working years.

Start by listing every liability. Include student loans, mortgage payments, practice loans, credit cards, and personal loans. Next, note the interest rate and required monthly payment for each. This creates clarity about which debts are costing you the most.

High-interest debt, especially credit cards, is eliminated first because the guaranteed cost exceeds typical investment returns. Student loans require more nuance. Federal loans may offer income-driven repayment plans or forgiveness paths, while private loans often demand faster payoff. Refinancing can lower interest, but removes federal protections, so decisions must be deliberate.

Mortgage strategy depends on retirement timeline. If you plan to retire at 50, entering retirement with large mortgage payments reduces cash flow flexibility. Many physicians want to retire with little required debt payments. This way, their retirement savings can cover their lifestyle instead of liabilities.

Overcoming Unique Challenges for Physicians

Physicians face a compressed wealth-building window. Long training delays serious retirement savings, while income spikes later. That creates pressure to save aggressively in fewer years. Add student loans, high expectations for lifestyle, and potential burnout, and retirement planning becomes more complex than for most professionals.

The solution is not just higher income. It is structured, intentional saving, coordinated retirement accounts, and tax-aware investing. Doctors who treat retirement planning like a clinical protocol, with clear benchmarks and adjustments, are far more likely to reach financial independence on time.

For a complete framework tailored specifically to physicians starting late, see:

Read: [Physician Retirement Planning: How Doctors Can Retire Confidently (Even If They Start Late)]

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

There is wide variation, but many physicians retire with several million dollars in combined retirement accounts and taxable investments. Surveys show some doctors still feel unprepared despite high earnings. Outcomes depend on savings rate, debt load, lifestyle, and years worked.

Yes, but only if your annual expenses are low enough for that amount to last 30 to 40 years. A $2M portfolio using a 4% withdrawal rate provides about $80,000 per year before tax, which may be enough in low-cost lifestyles but tight for physicians used to higher spending or facing rising healthcare costs.

You generally need enough savings to replace about 70 to 80% of your working income, adjusted for taxes, lifestyle, and healthcare. Early retirees need more because retirement lasts longer and Social Security begins later.

Your money lasts as long as your withdrawal rate, investment returns, inflation, and spending habits allow. Lower withdrawal rates and flexible spending extend portfolio life, while high spending and market downturns early in retirement can shorten it.