Most doctors need a 401k with millions of dollars. This is part of a bigger retirement plan. The total savings depends on lifestyle, retirement age, and other income. The number changes based on spending level, when you stop working, and whether you plan to retire early, but the framework for calculating it stays consistent.

Many physicians feel behind because earnings start late after medical school, debt lingers, and lifestyle rises quickly. That creates pressure, confusion, and uncertainty around physician retirement. This guide solves that. You will see how to estimate your target, how the 401k fits into your retirement plan, and what actions actually move the needle. The structure here reflects how financial planners model retirement planning for high-income professionals and how doctors build real retirement savings over time.

Why Retirement Planning for Doctors is Different

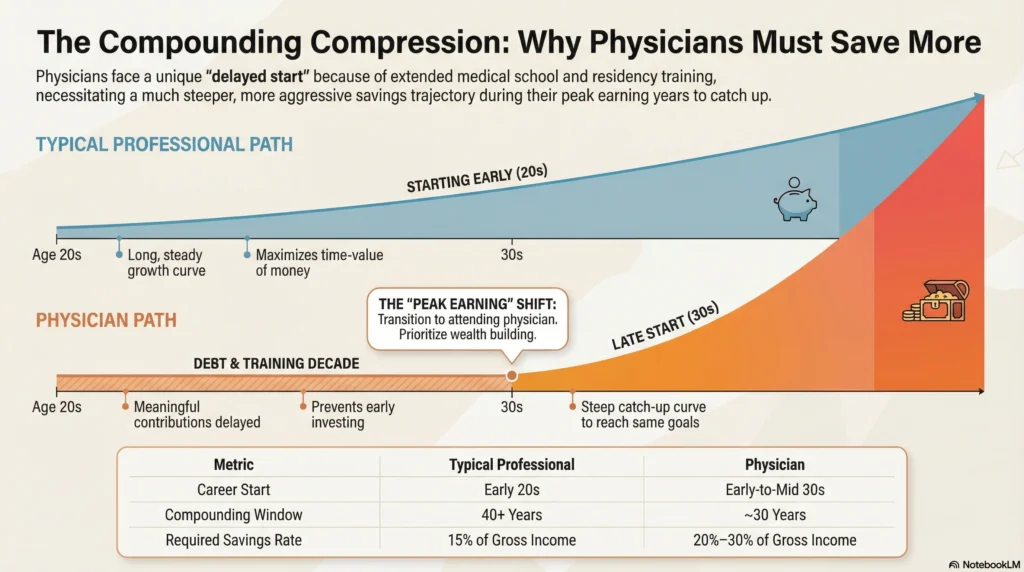

Physicians do not follow a normal earnings timeline. Most professionals begin serious retirement savings in their 20s. Doctors often begin meaningful contributions in their 30s after medical school and residency. That delay compresses the timeline for compounding and forces higher saving intensity later.

At the same time, physicians face large fixed costs. Medical school expenses, student loan payments, insurance, and high cost of living in metro areas push spending up early. Then income jumps sharply. Without structure, that income increase leads to lifestyle expansion rather than wealth building.

Doctors also deal with:

- Long training and delayed investing

- High income taxes during peak earning years

- Pressure to maintain professional lifestyle

- Exposure to liability, making asset protection important

- Often supporting extended family

All of this makes retirement planning more technical and more urgent. You are not just saving casually. You are executing a structured retirement plan under time constraints.

Read: [Physician Retirement Planning: How Doctors Can Retire Confidently (Even If They Start Late)]

“Comfortable Retirement” for Physicians

Comfort means different things to different doctors. For some it is travel and flexibility. For others it is freedom from call schedules and financial independence. But comfort always ties back to spending.

Lifestyle and Expenses in Retirement

Physicians often expect spending to fall sharply after work. In reality, many maintain a similar or only slightly reduced lifestyle. Travel increases. Healthcare costs rise. Hobbies expand. Some continue helping children or parents.

Doctors usually have these retirement expenses:

- Housing or mortgage payments if not fully paid off

- Property taxes and maintenance

- Travel and leisure

- Healthcare costs before Medicare

- Supplemental health insurance

- Insurance like life insurance or long-term care

- Income taxes on withdrawals

- Charitable giving

- Family support

Doctors who want early retirement must intentionally control lifestyle during peak earning years. That means distinguishing between professional image spending and true personal finance priorities. If you aim for financial independence, you must convert a large portion of income into retirement savings instead of consumption.

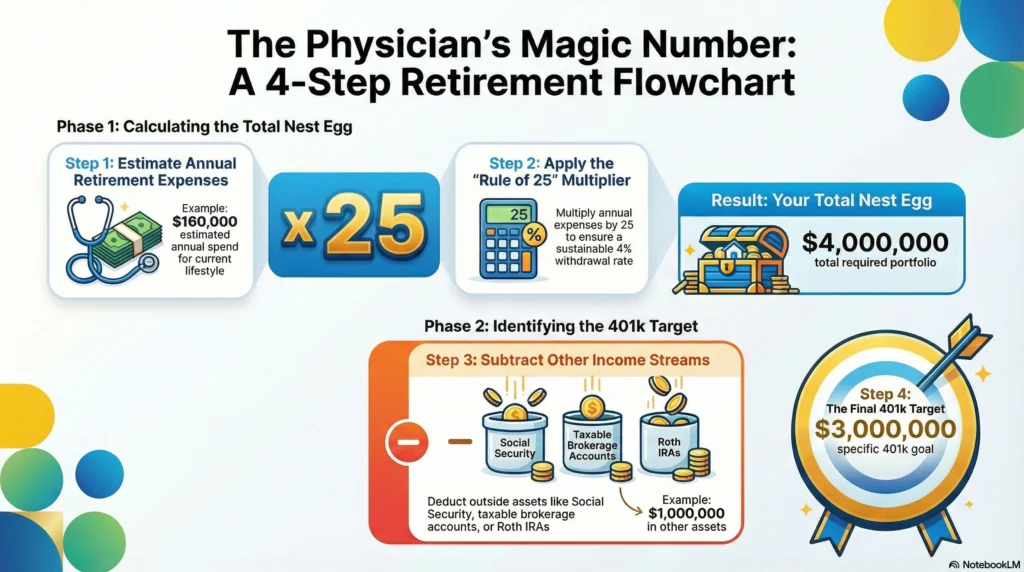

The “Magic Number” Concept: Total Retirement Nest Egg

Your magic number is the total nest egg required to generate sustainable income.

A commonly used planning approach is the Rule of 25. Multiply expected annual retirement expenses by 25 to estimate the total portfolio needed. This supports a withdrawal rate near 4 percent.

If a physician expects $160,000 per year in retirement expenses, the estimated nest egg is about $4,000,000. That aligns with survey findings where physicians cited around $4 million as a comfortable target physician retirement savings target.

That total includes 401k, retirement accounts, Roth IRA, taxable accounts, and other income streams. The 401k often becomes the largest component.

The 401k as a Core Engine for Physician Retirement Wealth

Your 401k is not just another account. It is a tax-advantaged wealth engine.

It matters because:

- High contribution limits allow large retirement savings quickly

- Contributions reduce taxable income in peak years

- Investments grow without annual income taxes

- Many plans offer employer contributions

- It builds disciplined saving automatically

Physicians who consistently maximize their 401k often build seven-figure balances faster than those who focus only on brokerage investing.

Physicians often need rates above those general rules because earnings start later.

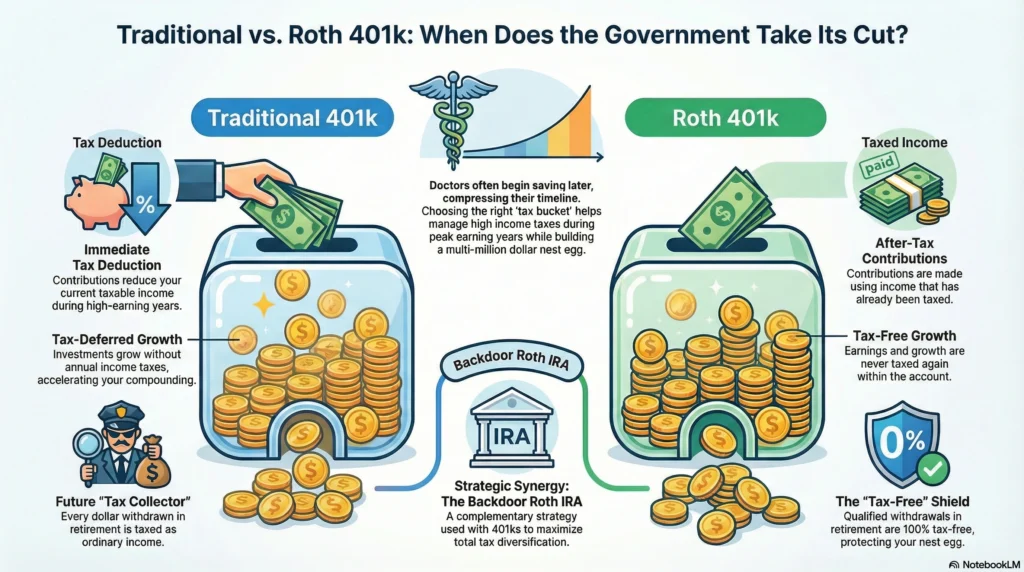

Understanding Traditional vs. Roth 401k for High Earners

Traditional 401k | Roth 401k | |

|---|---|---|

Taxes today | Lowers taxable income now | Contributions made after income taxes |

Taxes later | Withdrawals taxed in retirement | Qualified withdrawals tax free |

Best for | High tax bracket years | Early retirement flexibility |

Role | Reduces current tax burden | Helps manage future tax exposure |

High earners benefit from traditional contributions because they reduce income taxes when earnings peak. Roth contributions create tax-free income later, which helps manage taxes before social security benefits begin.

Doctors often pair 401k with Roth IRA through a backdoor roth IRA strategy for additional tax diversification.

Maximizing Contribution Limits

Standard 401k contribution limits are $23,500, with an additional $7,500 catch-up at age 50. Employer contributions can push totals above $70,000 401k limits for physicians.

Maximizing limits requires planning:

- Adjust payroll elections early in the year

- Coordinate profit-sharing if in private practice

- Use catch-up contributions once eligible

- Avoid front-loading mistakes that miss employer match

- Track limits across multiple retirement accounts

This is where a financial planner or financial advisor becomes valuable.

Tax-Advantaged Growth and Asset Protection

Inside a 401k, investments such as mutual funds grow without annual taxation. That tax deferral accelerates compounding. Over decades, this creates a significantly larger nest egg compared with taxable investing.

Employer retirement accounts often protect money from creditors. This is important for doctors who have private practices.

Quantifying “How Much” in Your 401k: Physician-Specific Scenarios

Your 401k target depends on when you start and how aggressively you save.

Estimating Your 401k Goal: A Step-by-Step Example

- Estimate retirement spending

- Multiply by 25 for total nest egg

- Subtract expected social security benefits and other income streams

- Assign portion to 401k based on other savings

If total need is $5M and you expect $1M outside retirement accounts, your 401k target may be $4M.

Use tools like the Financial Freedom Calculator for Doctors.

Scenario 1: The Early-Career Doctor (Residency/Early Attending)

Focus on habits, not size. Even modest contributions grow. Capture match. Start Roth IRA if possible. Keep lifestyle stable after training despite income jump. Control student loans strategically.

Scenario 2: The Mid-Career Attending (Peak Earning Years)

This is the wealth building phase. Maximize all retirement accounts. Use taxable accounts for overflow. Plan income taxes, where investments are held, and tax variety together. Doctors in private practice may add defined benefit plans.

Scenario 3: Nearing Retirement (50s and Beyond)

Shift focus to risk management. Lower the ups and downs in value. Plan withdrawal order. Figure out when to get Social Security benefits. Model how long assets must last.

Read: [When Do Doctors Retire? Average Retirement Age for Physicians Explained]

Beyond the 401k: Building a Comprehensive Physician Retirement Portfolio

A strong retirement plan uses multiple buckets.

Complementary Retirement Account Options

Options include Roth IRA, SEP IRA, defined benefit plans, and backdoor roth IRA strategies. These increase retirement savings beyond 401k limits.

Taxable Investment Accounts for Additional Growth

Taxable accounts provide flexibility for early retirement before age 59½. Use tax-efficient mutual funds and index funds.

Actionable Strategies to Optimize Your Physician 401k

- Automate contributions

- Rebalance annually

- Minimize fees in mutual funds

- Increase savings with each raise

- Work with a financial planner

- Integrate life insurance and estate planning

- Align investments with your retirement plan

Read: [How Do Doctors Retire Early? What Makes It Realistic (and What Doesn’t)]

Also Read: [How Much Money Do Doctors Need to Retire at 50? A Realistic Breakdown]

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Yes, a 401k remains one of the most powerful retirement tools for physicians because of high contribution limits, tax-deferred growth, and potential employer contributions. High earners in top tax brackets get a tax deduction upfront. The long time for growth can greatly increase retirement money. This is better than investing only in taxable accounts.

For most physicians, $1 million in a 401k alone is not enough for a comfortable retirement unless expenses are very low or there are other large income sources. Using common planning rules, $1 million may support roughly $35,000 to $40,000 per year in sustainable withdrawals, which is often below a doctor’s expected retirement lifestyle.

The amount needed in a 401k depends on your total retirement income plan, but many physicians still require well over $1 to $2 million in their 401k even with Social Security and pensions. Those additional income sources reduce the burden on the 401k, but doctors often have higher lifestyles, taxes, and healthcare costs that still require a large investment base.

Many physicians aim for a seven-figure 401k balance, often $2 million or more, as part of a broader retirement portfolio. The exact number depends on spending needs, retirement age, debt status, and whether other accounts or income streams exist.

There is no single “correct” balance, but planning models often suggest your 401k plus other investments should be able to support about 70% to 80% of your pre-retirement income. High-earning doctors usually have millions in retirement accounts. The 401k is a main part of this.

Doctors can improve their 401k by contributing the maximum each year. They should get full employer matches. After age 50, they can add extra catch-up contributions. They should pick a mix of investments that is diverse and low cost. Consistency, tax planning, and avoiding early withdrawals are key to long-term compounding.