You can retire confidently as a doctor even if you start late. You must align your income, savings, insurance, and tax plans into one coordinated retirement system. Your path will vary based on debt, specialty, practice model, and goals, but the core framework stays the same.

Right now the problem feels familiar. Income is strong, yet retirement feels uncertain. Years went to training. Lifestyle rose with pay. Practice costs, family needs, and taxes compete for every dollar. You know you should plan better, but the moving parts make it hard to see what actually matters.

This guide solves that. You will see the exact sequence that turns high income into lasting financial independence instead of delayed stress. These steps reflect how real physicians transition from earning well to building security. Surveys show doctors carry emotional and financial concern about retirement decisions, not just math. Physicians report major worries around retirement finances, health, and life quality. That is why structure matters more than guesswork.

You do not need perfection. You need alignment.

Balancing High Income with High Expenses

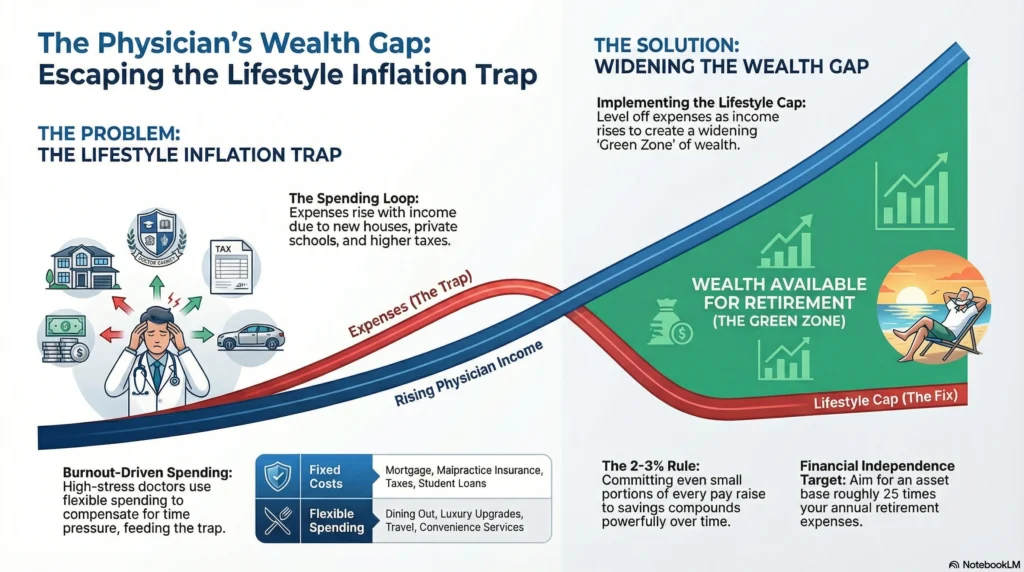

Doctors often earn in the top income brackets yet still feel tight on cash flow. The issue is rarely salary. It is expense growth tied to career progression.

Training ends. Income rises. A new house, better neighborhood, private school, upgraded lifestyle, higher taxes, and sometimes group practice buy-ins. Savings do not rise as fast as spending. This is how high earners delay financial independence for years.

You fix this by controlling the gap between earnings and lifestyle.

Start with visibility. Separate fixed costs from flexible spending. Fixed costs include mortgage, health insurance, malpractice coverage, loan payments, and taxes. Flexible costs include dining, upgrades, travel, and convenience spending.

Then lock in a rule. Every pay raise must increase savings before lifestyle. Even a 2 to 3 percent increase compounds powerfully toward retire early goals.

Where physicians slip:

They assume income growth alone solves retirement. It does not. Without discipline, income and spending rise together.

Burnout worsens this. Doctors under stress often spend to compensate for time pressure. That creates a loop where physician burnout feeds lifestyle inflation, which then delays retire early possibilities.

Read: [Doctor Net Worth vs Financial Freedom: Why They’re Not the Same Thing]

Also Read: [The Biggest Financial Mistakes Doctors Make in Their 30s and 40s (And How to Avoid Them)]

Setting Clear Retirement Goals

You cannot execute strong retirement planning without a target. Vague hopes create vague action.

Determining Your Ideal Retirement Age

Your retirement age drives every financial decision. It determines how long your assets must last, when accounts become accessible, and how much you must save yearly.

Many physicians delay retirement. 58 percent of physicians retire after age 65. Others aim to retire early due to physician burnout. A review of research shows most retire between 60 and 69, but workload and burnout push some earlier and others later.

Pick two ages. Ideal and backup. Example 58 and 63. This allows flexibility without drifting.

Doctors often assume they can “just work longer.” Health, policy, or group practice dynamics may remove that choice.

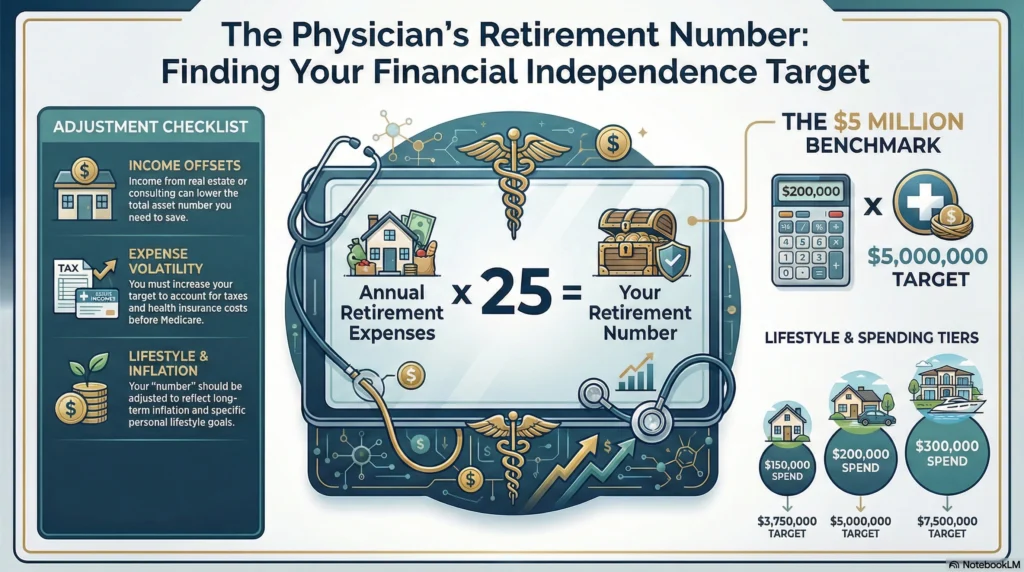

Defining Your Retirement Number

Your number is the asset base needed to support spending. A common starting point is annual retirement expenses multiplied by 25.

If you want $200,000 per year, you need roughly $5 million. But physicians adjust for:

• Real estate income

• Consulting income

• Taxes

• health insurance costs before Medicare

• Inflation and lifestyle goals

This number anchors your financial plan.

Also Read: [Physician Net Worth by Age: What Doctors Should Expect at Every Stage]

Maximizing Retirement Account Options

Doctors have access to multiple retirement accounts. Coordination matters more than volume.

Utilizing 401(k) Plans Effectively

Your 401(k) is the core engine of retirement planning.

Capture employer match first. Then aim for annual maximums. Choose diversified funds, not random picks. Rebalance yearly.

Many physicians leave large balances sitting in conservative funds long term. That slows growth and delays financial independence.

Exploring Backdoor Roth IRAs

High earners can still fund Roth space through Backdoor contributions. Growth becomes tax free. That supports retire early flexibility.

Physicians often skip this for years due to confusion, missing compounding.

Leveraging Solo 401(k) and SEP IRAs

Side income or group practice earnings allow additional contributions. These accounts accelerate savings beyond standard employer plans.

This is how late starters close gaps.

Also Read: [Where Doctors Should Invest After Maxing Out Their 401k and Roth IRA]

Exploring Additional Saving Opportunities

Retirement accounts alone may not cover early retirement needs.

Real Estate and Other Income Streams

Real estate gives you income from different sources and protects against inflation. But it requires capital and time.

Other options include consulting, teaching, or digital education work tied to your medical speciality.

These streams support partial financial freedom before full retirement.

Where doctors struggle:

They jump into complex deals without experience. Start small.

Strategic Asset Protection

Wealth building without protection is incomplete.

Evaluating Insurance Needs

Your earning power is your largest asset. Protect it.

Core coverages:

• Disability insurance

• Malpractice insurance

• Umbrella liability coverage

• Term life insurance

Disability coverage is critical given the physical demands of medicine. Loss of income derails retire early plans instantly.

Burnout plays a role too. Chronic stress linked to physician burnout increases disability risk.

Also Read: [Financial planning for doctors]

Understanding Tax Implications

Taxes shape retirement outcomes.

Navigating Taxation on Retirement Income

Retirement income sources are taxed differently.

401(k) withdrawals are ordinary income. Roth withdrawals are tax free. Taxable accounts may have capital gains treatment.

Diversifying tax types across retirement accounts helps manage brackets later. This flexibility supports both late and retire early paths.

Doctors often overfund only pre-tax accounts, creating future tax pressure.

Healthcare costs also matter. Health insurance and Medicare premiums depend on income. Planning withdrawals affects costs.

Also Read: [How Much Do Doctors Need in a 401k to Retire Comfortably?]

Avoiding Common Financial Pitfalls

Even high earners repeat predictable errors.

• Waiting too long to start structured retirement planning

• Overspending during income jumps

• Ignoring tax strategy

• Holding too much cash long term

• Buying products they do not understand

Burnout again appears here. Doctors facing physician burnout often delay financial decisions. That delay costs years of compounding.

Variation in retirement timing is real. Around 30 percent of physicians retire between ages 60 and 65 and fewer retire before 60. Planning earlier gives options.

Also Read: [Student Loan Repayment Strategies for Doctors: A Clear Plan for High-Income Physicians]

The Coordinated Path Forward

Strong Physician retirement outcomes come from sequence, not isolated moves.

- Control expense growth to widen savings

- Set a retirement age target

- Define your number

- Maximize tax-advantaged retirement accounts

- Add income streams outside practice

- Protect income and assets

- Manage tax exposure

- Avoid predictable mistakes

Confidence in retirement planning does not come from guessing markets. It comes from managing what you can control.

Your income is powerful. Directed properly, it converts into financial independence, optional work, and eventually the ability to retire early on your terms.

Also Read: [How Much Money Do Doctors Need to Retire at 50? A Realistic Breakdown]

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

The 7% rule means withdrawing 7% of your investment portfolio each year in retirement. This rule is usually aggressive and has higher risk than more cautious methods. Withdrawing money quickly may work during strong markets or short retirements. But it increases the risk of running out of money during long retirements or market downturns. That is why many planners recommend withdrawing less.

Doctors often retire later because of long training years, delayed peak earnings, high income attachment, and identity tied to medicine. Many doctors have ongoing financial responsibilities and work duties. They also may feel emotionally unprepared for life after clinical work.

Most physicians retire between 60 and 69 years old. Retirement timing varies by specialty, workload, and burnout levels, but this age band is the most common range.

Retirement age depends on income needs, savings, health, burnout, specialty demands, practice ownership, family situation, and confidence in financial security. Emotional readiness often matters as much as money.

Many doctors want to retire in their late 50s or early 60s. However, they often retire later because they are not financially ready, feel attached to their work, or are unsure about what to do after retirement.

Physicians often want to retire due to burnout, administrative burden, declining job satisfaction, desire for time freedom, health concerns, or wanting to spend more time with family.