High-income doctors stop living paycheck to paycheck by fixing how they manage cash flow. They do not do this by earning more money. This guide shows you step by step the exact choices that lead to financial stability and long-term control.

If you are an average physician earning well into six figures yet still watching your account balance reset every month, the problem is not discipline or intelligence. The real problem is fragmentation. Fragmented spending. Fragmented debt strategy. Fragmented retirement accounts. Fragmented planning.

You are solving financial problems in isolation instead of as a system.

This guide gives you a unified, physician-specific framework to move from financial stress to financial security. It is built on real physician experiences and supported by evidence from retirement planning and medical finance research.

Retirement planning reviews and studies about doctors’ money problems show that doctors use many savings accounts without a clear plan. This makes their cash flow seem tighter than it really is.

Physicians often use multiple retirement accounts without a unified approach, fragmenting savings and increasing cash flow stress.

What follows is not theory. It is a practical sequence designed to help you stop reacting to money and start directing it.

Managing High Expenses Relative to Income

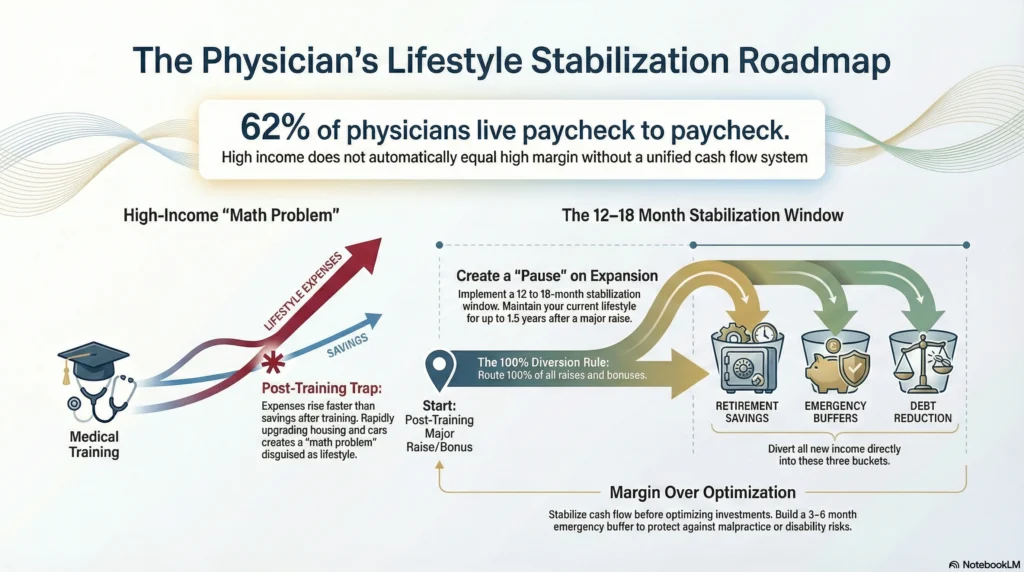

The first decision is recognizing that paycheck-to-paycheck living is usually a math problem disguised as a lifestyle problem.

Doctors leave medical school with delayed earnings, then jump rapidly into a higher tax bracket. Expenses scale quickly because life has been on hold. Housing improves. Cars upgrade. Family responsibilities grow larger. Professional costs increase.

Waverly Advisors say doctors often live paycheck to paycheck after training. This happens because their living costs grow faster than their savings when they start earning full income. This transition period is where long-term financial independence is often delayed.

What to do starts with clarity.

You need a true monthly baseline that includes fixed obligations, professional costs, and minimum student loan payments. This is not budgeting every coffee. This is defining the minimum income your life requires to operate.

Why it matters is simple. Without knowing this number, every financial decision feels risky. You hesitate to save. You hesitate to invest. You hesitate to pay down debt aggressively.

What usually goes wrong is doctors assume high income automatically means high margin. Margin must be built deliberately.

This is also where many private practice physicians feel extra pressure, because income variability increases stress even when annual income is strong.

Addressing Lifestyle Creep

Lifestyle creep is not about luxury. It is about automatic upgrades without intentional tradeoffs.

When income rises, spending follows unless stopped intentionally. This is especially common for doctors who delayed gratification throughout medical school and residency.

What to do here is not cut everything. It is to pause expansion.

Create a stabilization window of 12 to 18 months after major income increases. During this time, any raise or bonus goes first to retirement savings, emergency buffers, or debt reduction.

Why this matters is that stabilization creates breathing room. It converts income into flexibility.

What usually goes wrong is doctors try to optimize investments before stabilizing cash flow. That sequence almost always fails.

Tackling Extensive Student Debt

Student loans are the single most common reason doctors feel trapped financially.

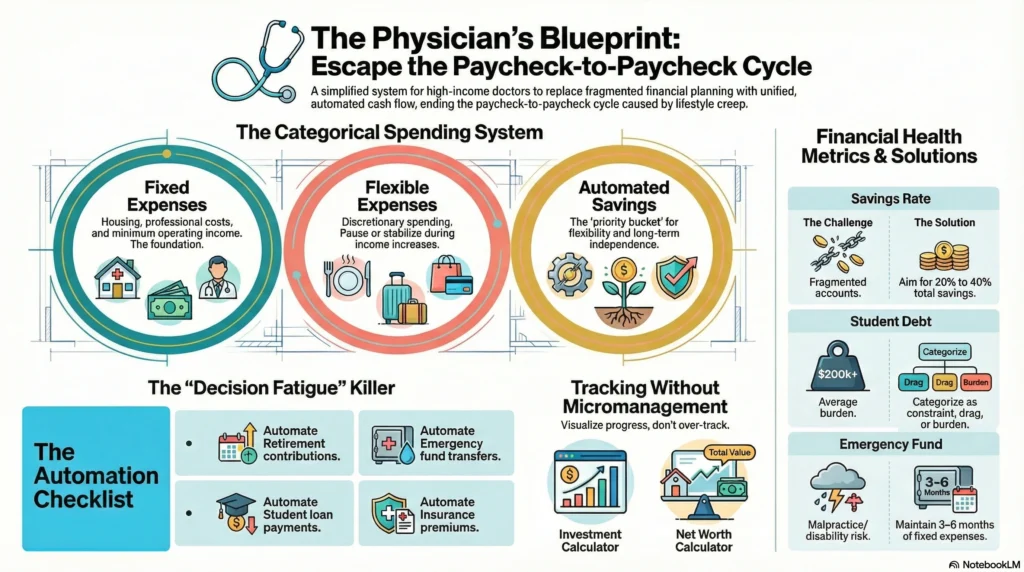

Medical school debt often exceeds $200,000. Interest compounds quietly. Required payments anchor your monthly cash flow before you make a single choice.

In Medical Economics, one physician describes living paycheck to paycheck through medical school and residency due to tuition costs exceeding $50,000 per year plus living expenses. Financial relief only came after committing to a clear debt and savings strategy.

What to do begins with categorization.

Your student loan debt fits into one of three categories:

- Cash flow constraint

- Interest drag

- Psychological burden

Each category demands a different response.

You may choose aggressive payoff, income-driven repayment plans, or loan forgiveness depending on specialty, private practice plans, and career horizon.

Why this matters is that unclear debt strategy creates hesitation everywhere else. Savings stall. Investing feels unsafe.

What usually goes wrong is mixing strategies or changing plans every year.

Developing Robust Personal Financial Management Skills

Doctors are rarely taught personal finance. You are trained to earn, not to manage.

This step is about systems, not willpower.

Budgeting and Expense Tracking

What to do is adopt a category-based spending system.

Instead of tracking every transaction, define:

- Fixed expenses

- Flexible expenses

- Automated savings

Why it matters is patterns reveal leverage. You cannot improve what you cannot see.

What usually goes wrong is overtracking. Complexity destroys consistency.

This is where tools matter.

Check out: [Investment and Savings Calculator for Doctors]

Check out: [Future Net Worth Calculator for Doctors]

These tools help you visualize progress without micromanagement.

Leveraging Financial Tools

Automation is a form of discipline.

What to do is automate:

- Retirement contributions

- Emergency fund transfers

- Student loan payments

- Insurance premiums

Why it matters is decision fatigue disappears.

What usually goes wrong is using too many tools without a clear system.

This is also the point where many doctors benefit from a financial advisor, not for stock picking but for coordination. A good financial advisor helps unify retirement accounts, taxable accounts, and insurance into one plan.

Building a Strong Emergency Fund

An emergency fund is foundational to financial stability.

Doctors face unique risks such as malpractice exposure, disability risk, and income disruption.

What to do is build 3 to 6 months of fixed expenses in a liquid account.

Why it matters is emergencies do not ask permission. A medical emergency, family problem, or job change can be survived instead of causing disaster.

What usually goes wrong is doctors skip this step because income feels reliable.

Emergency funds also protect your Net worth by preventing forced withdrawals from retirement accounts or reliance on credit cards.

Strategic Goal Setting for Retirement

Retirement planning is not about age. It is about control.

Doctors often add money to many retirement plans without coordinating them. These plans include 401(k), 403(b), 457(b), Roth IRA, and taxable accounts. They work separately unless combined on purpose.

What to do is define one retirement planning goal and align all accounts toward it.

Why it matters is fragmentation creates inefficiency and confusion.

What usually goes wrong is maxing accounts without considering cash flow impact.

Read: [Savings Account vs Investing: What Doctors Should Do With Extra Cash]

Exploring Diverse Retirement Accounts

Retirement accounts provide tax leverage.

You should understand how Roth IRA contributions, employer retirement plans, and taxable accounts interact with your tax bracket.

Why it matters is tax efficiency accelerates retirement savings.

What usually goes wrong is ignoring future tax exposure.

Understanding Tax Implications

Taxes are often the largest lifetime expense for an average physician.

What to do is align savings with marginal tax rates.

Why it matters is lower taxes equal higher flexibility.

What usually goes wrong is chasing deductions without a broader financial planning lens.

Leveraging High-Yield Savings and Treasury Bills

Not all money should be invested.

What to do is allocate short-term money to high-yield savings and Treasury bills.

Why it matters is liquidity protects decision-making.

What usually goes wrong is holding too much cash long term or investing money needed soon.

Creating Additional Income Streams

Additional income reduces pressure.

What to do is explore passive income aligned with your time constraints.

Options may include:

- Real estate partnerships

- Locum work

- Business ownership

Why it matters is diversified income increases financial security.

What usually goes wrong is chasing complexity too early.

Read: [Best Cash Flow Investments for Doctors Who Want Predictable Income]

Adopting a Holistic Approach to Financial Security

Financial freedom is not built in isolation.

It is built by aligning:

- Income

- Spending

- Debt

- Retirement savings

- Insurance

- Asset protection

Life insurance and disability insurance are not optional. They protect your income, your family, and your progress. Asset protection matters more as wealth grows.

What to do next is simple but powerful.

Revisit your structure. Clarify your priorities. Build systems before optimization.

This is how doctors stop living paycheck to paycheck.

Not by earning more.

But by finally directing what they already earn.

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Approximately 62% of doctors live paycheck to paycheck, even at high income levels, due to delayed earnings, student debt, and rapid lifestyle expansion after training. Studies and advisory firms consistently note that high fixed expenses and fragmented financial planning are the main drivers, not low income.

Yes, it is absolutely possible to stop living paycheck to paycheck by fixing cash flow structure, not by earning more money. Doctors who control their expenses, combine debt and retirement plans, and set up automatic savings usually reach financial stability in a few years.

Yes, the 20% savings rate typically includes retirement contributions such as 401(k), 403(b), Roth IRA, and other retirement accounts. For physicians, this total savings rate should reflect all long-term wealth building, not just cash saved in bank accounts.

During residency or fellowship, saving a small amount consistently, even 5% or less, is enough to build the habit and protect against emergencies. At this stage, the main goals are to keep cash flow steady, avoid high-interest debt, and keep basic retirement accounts active if possible.

If early retirement or accelerated financial independence is the goal, savings rates often need to exceed 25% to 40%. This requires tighter expense control, smarter debt decisions, and coordinated use of retirement and taxable accounts.

Lifestyle inflation is the tendency to increase spending automatically as income rises, without increasing savings at the same pace. It commonly occurs when physicians move from training into full earnings and begin upgrading housing, vehicles, and discretionary spending.

Lifestyle inflation can trap high-income doctors in paycheck-to-paycheck cycles despite earning more money each year. Over time, it delays retirement savings, increases financial stress, and makes financial freedom feel permanently out of reach.