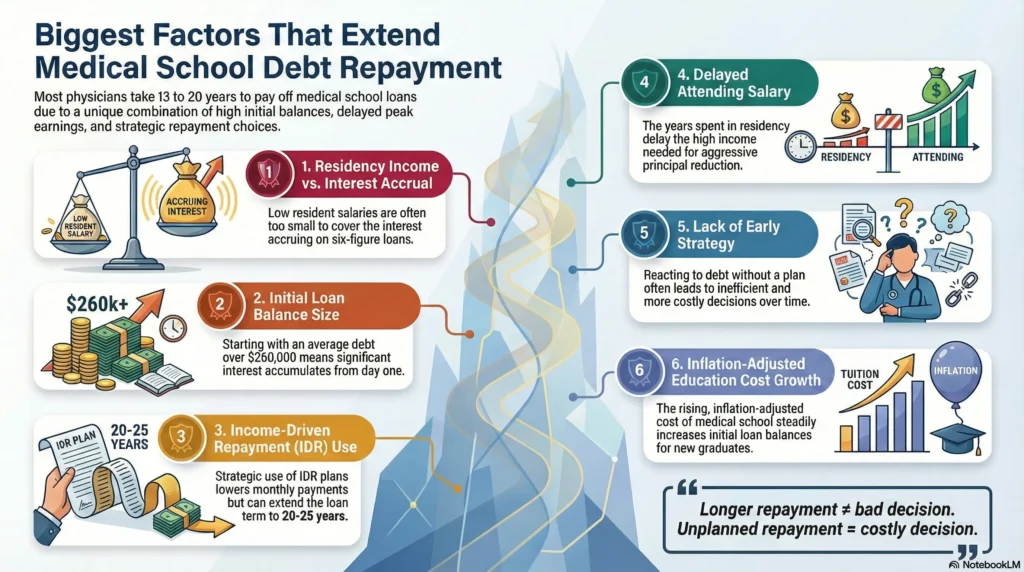

Most physicians take between 13 and 20 years to fully pay off medical school debt, not because they earn poorly, but because high balances, delayed earnings during residency, and strategic use of forgiveness or income-driven repayment stretch the repayment timeline. Some doctors finish faster by refinancing and aggressive payments, while others intentionally carry student loan debt longer to optimize cash flow, taxes, or loan forgiveness programs.

This guide is written for medical students, resident physicians, and practicing physicians who want a realistic, evidence-based answer to one question:

How long does medical school debt actually follow doctors—and why?

We’ll break down what doctors really owe, why payoff timelines are longer than expected, and how different repayment choices shape your financial future.

Average Cost of Medical Education

Medical school debt starts high—and that starting point determines everything that follows.

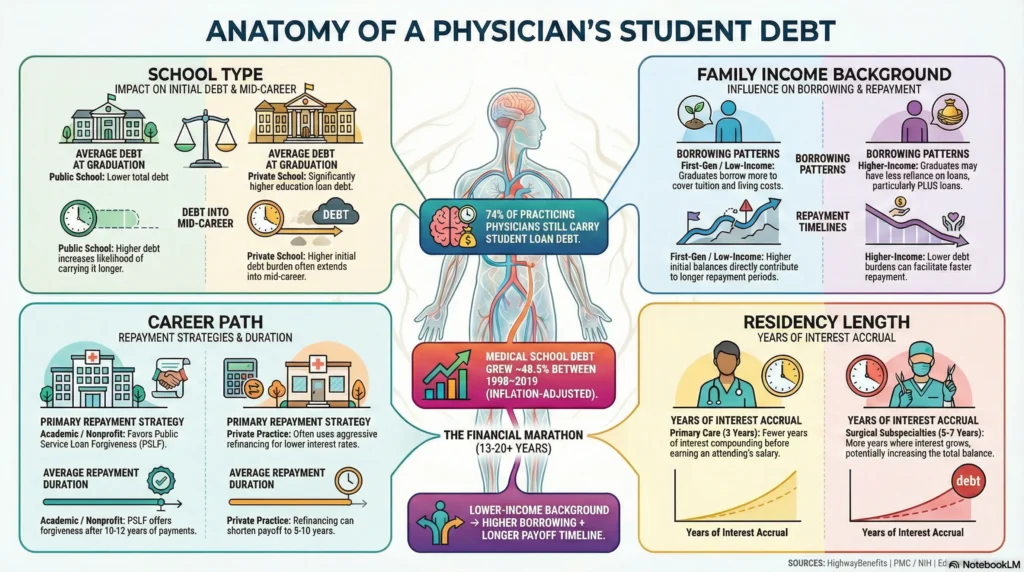

About 70% of medical school graduates leave with education loan debt, and the average total balance across premed and medical school is roughly $264,519.

This includes:

- Federal student loan balances from undergraduate years

- Unsubsidized loans accrued during medical school

- Federal Grad PLUS loans used to cover tuition gaps and living costs

Debt levels vary widely:

- Public medical schools often produce balances closer to $200,000

- Private schools frequently exceed $300,000

- Students from lower-income backgrounds borrow more and rely more heavily on PLUS Loans

Historical data shows this problem is getting worse. Medical school debt rose nearly 48.5% between 1998 and 2019, even after adjusting for inflation.

This matters because repayment timelines don’t start at graduation—they start with six-figure balances already compounding interest.

If you want the structural “why,” Read: [Medical School Debt Explained: Why Doctors Graduate With Six-Figure Loans]

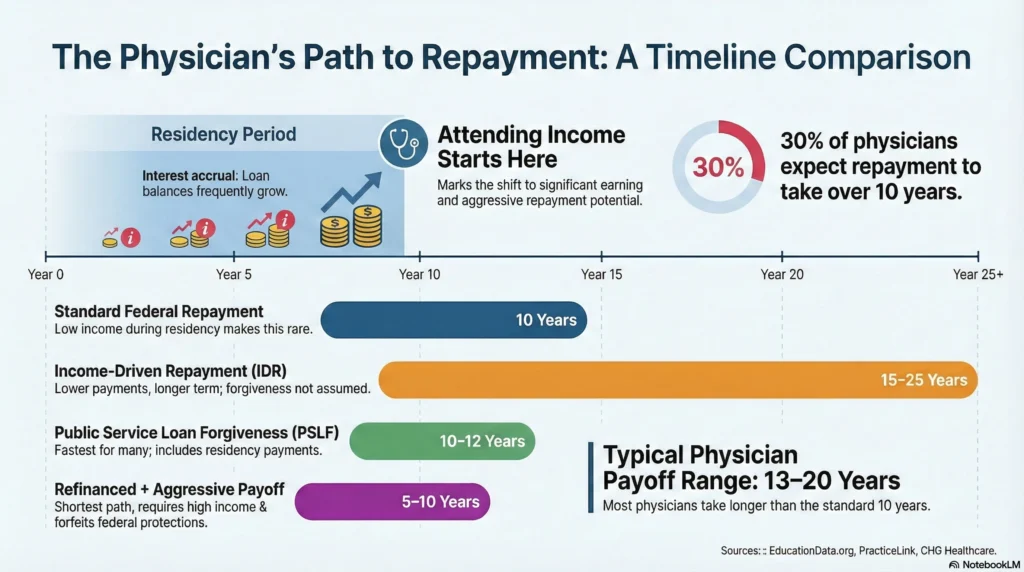

Typical Repayment Timelines

The standard federal student loan repayment term is 10 years, but most physicians do not finish anywhere near that window.

Why?

Because residency exists.

According to multiple physician surveys:

- 59% of physicians with student loan debt expect repayment to take more than 6 years

- 30% expect it will take over 10 years

- Many anticipate 15+ years when forgiveness is not used

More importantly, 74% of practicing physicians still carry some student loan debt, and many owe more than $250,000 well into their careers.

In practice, 13–20 years is the most common payoff range.

Why Doctors Take Longer to Pay Off Student Loans

1. Delayed Earnings During Training

A resident physician earns about $60,000 per year, while interest continues accruing on federal loans.

During this period:

- Monthly payments are often reduced or capped

- Interest rates continue compounding

- Balances frequently grow, not shrink

2. Large Initial Loan Balances

A 6–7% interest rate applied to $260,000 over multiple years creates tens of thousands in additional interest, even before attending income begins.

This raises the debt-to-income ratio early in a medical career and delays principal reduction.

3. Strategic Use of Repayment Plans

Many medical professionals choose longer repayment timelines because:

- Income-driven repayment lowers monthly payments

- Loan forgiveness programs erase remaining balances

- Cash flow is redirected to housing, family, or retirement

This is not financial failure.

It’s intentional debt management.

Loan Repayment Options and Their Impact on Payoff Time

Your repayment plan determines whether medical school debt lasts 10 years—or 25.

Income-Driven Repayment (IDR) Plans

Income-driven repayment plans cap monthly payments based on discretionary income rather than loan balance.

Key effects:

- Monthly payments stay affordable during residency

- Loan term often extends to 20–25 years

- Interest accrues if payments don’t cover it

About 65.1% of medical school graduates plan to pursue student loan forgiveness, usually through IDR plans combined with PSLF.

Best for:

- Medical students and residents

- Physicians pursuing nonprofit or academic careers

Tradeoff:

- Longer loan term

- Higher total interest without forgiveness

For a full breakdown of REPAYE, IBR, and RAP, Read: [Student Loan Repayment Strategies for Doctors]

Public Service Loan Forgiveness (PSLF)

Public Service Loan Forgiveness is the fastest exit for many physicians.

Under PSLF:

- Loans are forgiven after 120 qualifying monthly payments

- Payments are typically made during residency + early attending years

- Remaining balance is forgiven tax-free

This often results in 10–12 years total repayment, regardless of balance.

Standard repayment may say “10 years,” but PSLF is often the only way doctors actually finish in that window.

For eligibility details, Read: [Federal Student Loan Repayment Options Explained for Doctors and Physicians]

Refinancing Your Loans

Student loan refinancing shortens payoff timelines—but removes safety nets.

When you refinance:

- Federal loans become private student loans

- Loan forgiveness programs are permanently lost

- Interest rates may drop significantly

Doctors who refinance aggressively often eliminate medical school debt repayment in 5–10 years.

Best for:

- High-income attending physicians

- Those with stable employment

- Doctors not pursuing Public Service Loan Forgiveness

Risk:

- No income-driven repayment

- No federal protections

This decision should always be paired with a student loan calculator and careful cash-flow modeling.

Making Additional Payments During Residency

Most residents cannot make large payments—but small ones matter.

Even modest extra monthly payments:

- Reduce capitalization

- Shorten the overall loan term

- Lower total interest paid

For residents with manageable living expenses, early payments can shave years off repayment later.

That said, this only works if:

- Emergency savings exist

- No high-interest credit card debt is present

Otherwise, cash flow fragility outweighs the benefit.

Demographic Factors Influencing Debt Repayment

Not all doctors start from the same place.

Research shows:

- Graduates from lower-income families borrow more

- Private-school graduates carry higher education loan debt

- Debt burdens are heavier for first-generation physicians

Inflation-adjusted medical education costs rose sharply between 2008 and 2020, with debt growth disproportionately affecting these groups.

This directly influences how long student loan debt follows doctors.

How Long Debt Follows Doctors Into Mid-Career

Here’s the uncomfortable truth.

Many physicians still carry student loan debt into:

- Their late 30s

- Their early 40s

- Mid-career leadership years

This overlap affects:

- Home buying

- Family planning

- Retirement contributions

And it explains why high-income doctors can still feel financially constrained.

To understand the mental impact, Read: [How Student Loan Debt Affects Doctors’ Financial and Mental Well-Being]

What This Timeline Means for Long-Term Financial Planning

If medical school debt lasts 13–20 years, it must be planned around—not ignored.

That means:

- Coordinating debt payoff with retirement investing

- Using repayment plans strategically

- Avoiding emotional decisions driven by guilt or fear

This is where most doctors go wrong—not by borrowing, but by reacting without a plan.

For a numbers-based comparison, Read: [Should Doctors Pay Off Student Loans Early or Invest Instead]

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

On average, doctors take 13–20 years to fully pay off medical school loans, depending on loan balance, repayment plan, residency length, and whether they pursue forgiveness.

Paying off $100,000 typically takes 10 years on standard repayment, 15–25 years on income-driven repayment, or 5–7 years with aggressive payments after residency.

The 32-hour rule refers to a study guideline suggesting medical students should not exceed 32 hours per week of structured studying, as productivity and retention drop sharply beyond that.

Most doctors finish paying off student loans between ages 40 and 50, especially those who did not pursue PSLF or had long residency training.

It means medical school debt often overlaps with peak earning, family-building, and investing years, making early repayment strategy critical to long-term wealth.

You can shorten repayment by refinancing after residency, making extra principal payments, using signing bonuses, and avoiding unnecessary lifestyle inflation early in your career.

Medical students at private schools graduate with $300,000+ in total education debt on average, significantly higher than public school graduates.

Yes, public in-state medical schools and military or service-based programs generally have much lower tuition and reduce total debt significantly.

Starting repayment during residency usually reduces long-term interest costs, but income-driven plans are often necessary to keep payments affordable.

Over a lifetime, physicians often repay $1.3–1.7× the original loan balance, depending on interest rates, repayment length, and strategy.