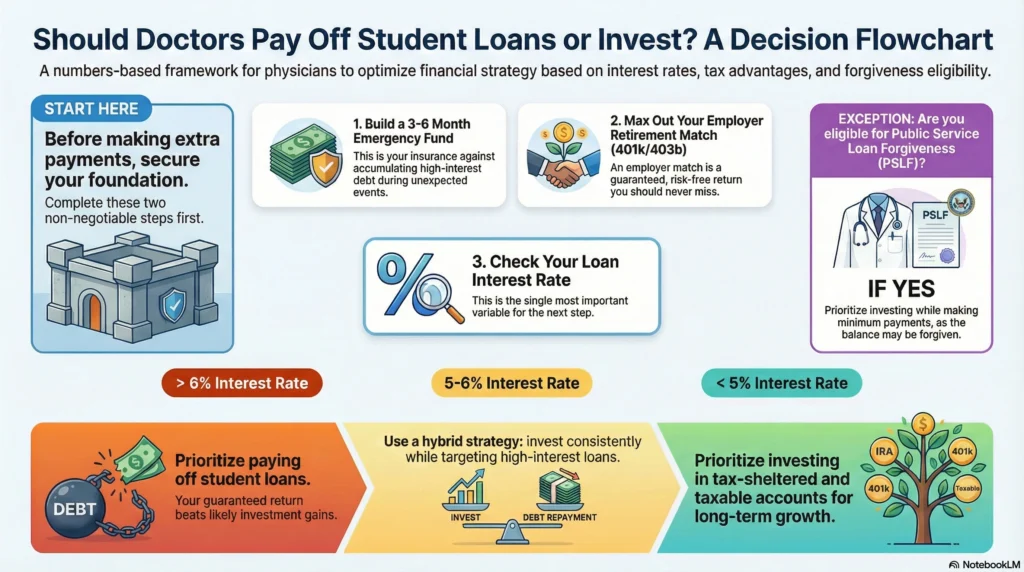

Doctors should generally pay off student loans early if their interest rate is above ~6%, and prioritize investing if their rate is below ~5%, with hybrid strategies making the most sense in the middle.

This rule changes based on your interest rate, income stability, tax bracket, loan forgiveness eligibility, and personal risk tolerance. There is a clear way to decide without guessing.

This guide walks you through that framework step by step, using real physician scenarios, real math, and real tradeoffs, not generic personal finance advice.

Evaluating Student Loan Interest Rates

Your interest rate is the single most important variable in this decision.

Why?

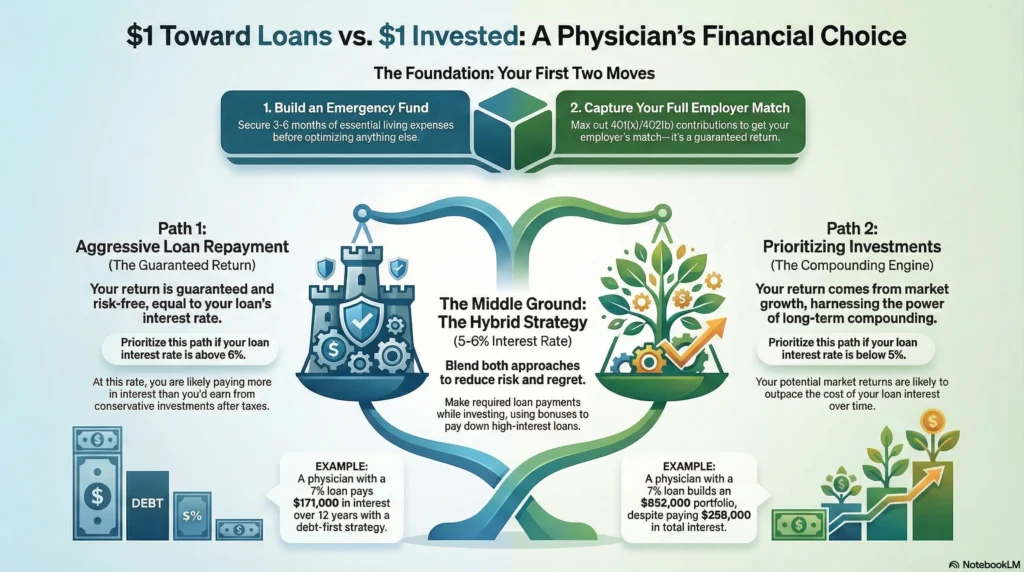

Because paying off student loans early gives you a guaranteed return equal to your interest rate—no volatility, no market risk, no downside.

According to OffCall’s physician finance analysis, if your student loan interest rate is above ~6%, you are mathematically paying more in interest than you’re likely to earn from conservative investing after taxes.

Assume a physician has student loans with a ~7% interest rate:

- A debt-first strategy results in paying ~$171,000 in interest and ~$471,000 total over ~12 years

- An invest-first strategy results in ~$258,000 in interest paid, but a larger long-term portfolio (~$852,000) due to compounding

The takeaway isn’t “investing is bad.”

It’s that high interest rates raise the bar for investing to win.

Practical rule doctors can actually use

- >6% interest rate → prioritize paying off student loans

- <5% interest rate → prioritize investing

- 5–6% range → hybrid strategy usually wins

If you’re unsure where your loans fall, pull your servicer statements and list every student loan balance, interest rate, and loan type in one place.

Leveraging Tax-Sheltered Accounts

Before you send a single extra dollar toward student loan repayment, check whether you’re fully using tax shelters.

This is where most physicians quietly lose hundreds of thousands over a career.

Why tax shelters change the math?

A dollar invested inside a 401(k), 403(b), or Roth IRA doesn’t behave like a taxable dollar.

It:

- Reduces current taxable income

- Grows tax-deferred or tax-free

- Lowers your lifetime tax bill

For a physician in a high bracket, that can add 30–45% effective value to every invested dollar.

According to Physicians Thrive, maxing out employer retirement plans should always come before deciding between extra loan payments and investing—because employer matches are guaranteed returns.

How physicians should sequence this (step-by-step)

- Contribute enough to capture 100% of employer match

- Max out tax-deferred retirement plan contributions

- Then decide whether excess cash goes toward:

- Paying off student loans

- Taxable investing

Skipping tax shelters to accelerate loan payoff is often a silent tax mistake, not a disciplined one.

Read: [Student Loan Repayment Strategies for Doctors: A Clear Plan for High-Income Physicians]

Utilizing Employer Retirement Benefits

Employer benefits are the easiest win in physician finance.

If your hospital offers:

- A 401(k)

- A 403(b)

- Or a 457(b)

You’re likely sitting on a risk-free return most investors would kill for.

CWG Advisors emphasize that employer matches should be prioritized before choosing between investing or paying off student loans.

Why this matters more for doctors?

Physicians often delay retirement savings while focusing on paying off student loans—but every missed match year is lost forever.

This is especially damaging early in your career, when compounding has the most power.

Weighing the Impact of Inflation

Inflation quietly works for borrowers and against savers holding cash.

When inflation runs at 3–4%, fixed-rate student loans effectively shrink in real terms over time.

That means:

- You repay loans with cheaper future dollars

- Investments that track inflation grow faster than debt

This is why moderate-interest Federal student loans often don’t require panic-level repayment.

But inflation doesn’t eliminate risk.

It just tilts the scale slightly toward investing—if your interest rate is reasonable.

Considering Current Tax Brackets

Doctors experience one of the steepest tax jumps of any profession.

- Residency: lower tax bracket

- Attending years: suddenly top marginal rates

That timing matters.

Paying aggressively during residency can feel responsible—but it may cost you flexibility later.

This is why many physicians benefit from:

- Lower student loan payments early

- Higher investing once income stabilizes

This approach protects cash flow while positioning you for long-term growth.

Read: [Average Medical School Debt: What Doctors Really Owe and How Long It Takes to Pay Off]

Assessing Personal Risk Tolerance

No spreadsheet captures stress.

Some physicians feel constant anxiety carrying loan debt.

Others panic when markets dip.

Both reactions matter.

If paying off student loans gives you clarity, focus, and peace of mind, that’s a valid return—just not one Excel tracks.

But ignoring math entirely can also cost you decades of growth.

The goal isn’t to eliminate emotion.

It’s to design around it.

Importance of Maintaining Emergency Funds

Before optimizing anything, build an emergency fund.

At least 3–6 months of core expenses.

Doctors without an emergency fund often:

- Accumulate credit card debt

- Pause investing during downturns

- Make rushed refinancing decisions

Liquidity buys time.

Time prevents mistakes.

An emergency fund is not an investment.

It’s insurance for decision-making.

Balancing Investment with Loan Repayment: Hybrid Strategies

According to CWG Advisors, blended strategies often produce the best long-term outcomes for physicians, especially when life goals are involved.

Hybrid strategies might include:

- Investing consistently while making required loan payments

- Accelerating payments only on high-interest loans

- Using bonuses or locums income for debt reduction

Hybrid approaches reduce regret because you’re never “all in” on one path.

Exploring Federal Student Loan Repayment Plans

Federal student loans give physicians options private loans do not.

Income-driven repayment plans:

- Lower monthly student loan payments

- Improve cash flow

- Preserve student loan forgiveness eligibility

But they can also:

- Increase total interest paid

- Extend repayment timelines

These plans work best when used intentionally—not automatically.

Read: [Federal Student Loan Repayment Options Explained for Doctors and Physicians]

Examining Alternative Student Loan Repayment Options

Student loan refinancing can reduce interest rates—but removes federal protections.

It makes sense when:

- You don’t qualify for forgiveness

- Your income is stable

- Your debt-to-income ratio is improving

It’s dangerous when used prematurely or emotionally.

Refinancing is a strategy—not a milestone.

Attitudes Toward Debt and Financial Decision-Making

Debt isn’t just math.

It’s identity, upbringing, and culture.

Some doctors see debt as leverage.

Others see it as failure.

Your plan must align with how you think—or you won’t stick to it.

Aligning Financial Decisions with Personal Priorities

Money is a tool.

Not the score.

Your decision should support:

- Career flexibility

- Burnout prevention

- Family goals

- Optionality

If your plan makes you resent your career, it’s broken—even if it’s optimal on paper.

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

The PAYE (Pay As You Earn) repayment plan is ending for new borrowers. Eligible doctors must now consider alternatives like SAVE or IBR. These change how monthly payments and forgiveness timelines work.

If your debt-to-income ratio is greater than 1, paying down student loans often takes priority because your loan balance meaningfully limits cash flow and financial flexibility.

If you work for a nonprofit or government employer that qualifies for PSLF, investing while making minimum payments is often smarter because remaining loan balances may be forgiven tax-free.

Only Direct Federal Student Loans qualify for income-driven repayment and PSLF. This affects whether investing instead of paying loans aggressively makes sense.

You should generally pay off loans first if your interest rate is above ~6% and invest first if it’s below ~5%, with hybrid strategies often working best in between.

It is better to pay off loans when interest rates are high and invest when rates are low, assuming you are also capturing employer retirement matches.

Most doctors do not pay off student loans quickly because long training periods, high balances, and strategic use of forgiveness or investing slow aggressive repayment.

The 50/30/20 rule suggests allocating 50% to needs, 30% to wants, and 20% to savings or debt, but for doctors, this often needs adjustment due to high loan balances and delayed earnings.

Paying off loans provides guaranteed returns equal to the interest rate, while investing offers higher potential growth but with market risk and volatility.

Medical student loan interest rates often range from 5 to 8%. These rates can be higher than safe post-tax investment returns, especially in unstable markets.

Investing makes more sense when loan interest rates are low, markets are expected to deliver reasonable long-term returns, and the doctor has stable income and emergency savings.