Yes, being a doctor can be worth it financially—but only over the long term, and only if high income is converted into net worth and financial freedom rather than higher spending.

In the short and medium term, doctors often look worse off than peers in tech, finance, or business because of delayed earnings, heavy student loans, and lifestyle inflation. The payoff comes later—and it is not automatic.

That distinction matters. Because many physicians earn a great salary and still feel financially behind.

This guide explains why that happens, what the real numbers look like, and how doctors who “win financially” actually do it.

The Real Financial Question Behind Becoming a Doctor

The real question is not “Do doctors make a lot of money?”

They do.

The real question is whether medicine creates wealth relative to the time, debt, and opportunity cost required to get there.

Most people outside healthcare see doctors as rich because they focus on income. Doctors who feel disappointed focus on time, stress, and net worth.

Those perspectives collide.

To evaluate whether medicine is financially “worth it,” you have to look at:

- Lifetime earnings

- Debt accumulation

- Net worth by age

- Financial freedom, not just salary

Read: [Are Doctors Really Rich? Income vs Net Worth vs Financial Freedom]

The True Cost of Medical School and Training

Medical education is one of the most expensive professional paths in the United States.

Tuition alone for medical or dental school often exceeds $60,000 per year. That does not include living expenses, exam fees, or lost income during training.

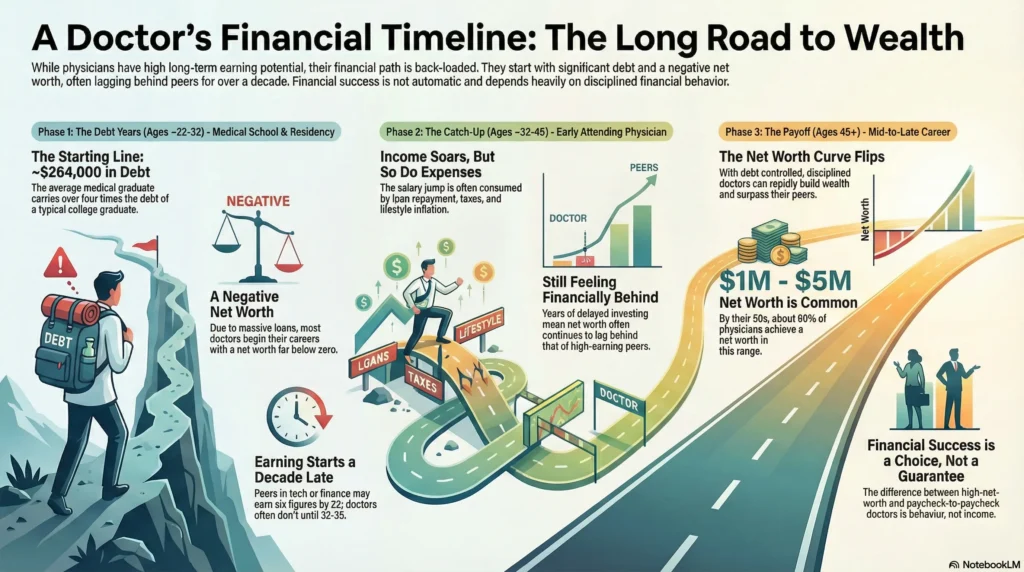

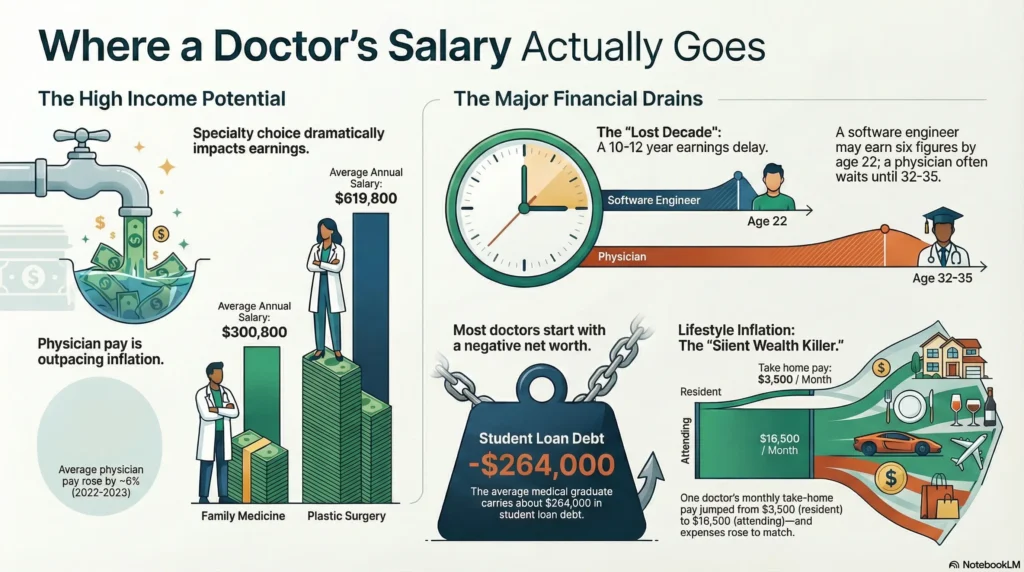

According to recent data, the average medical graduate carries about $264,000 in student loans

That number is more than four times the debt of a typical college graduate.

And that debt starts accumulating before residency, fellowship, or intern year.

The MCAT, application cycles, relocation, and unpaid research years add hidden costs that never appear in salary comparisons.

Student Loans and the Early Net Worth Reality

Because of medical school debt, most doctors begin adulthood with a negative net worth.

Residents often earn $60,000–$70,000 per year. After taxes, rent, and basic expenses, there is little room to build assets.

That means:

- No investing

- Minimal retirement contributions

- Delayed home ownership

This is why many physicians in their early 30s look “behind” financially.

According to physician finance analyses, most residents and early attendings have a net worth below zero due to student loan balances and minimal savings

Read: [Net Worth by Age for Doctors in Training vs Attending Physicians]

Why Doctors Start Earning Late Compared to Other Careers

Doctors start earning meaningful income far later than peers in:

- Tech

- Finance

- Consulting

- Entrepreneurship

A software engineer may earn six figures by age 22.

A physician often does not until age 32–35.

That 10–12 year gap is pure opportunity cost.

Those peers are:

- Investing earlier

- Benefiting from compound interest

- Buying appreciating assets

This delay explains why doctors often feel frustrated even with high pay.

Physician Income: High, But Not Immediate

Physicians earn well—but the curve is back-loaded.

According to the Doximity Physician Compensation Report, average U.S. doctor income is roughly $376,000 per year

From 2022 to 2023, physician pay rose by ~6%, outpacing inflation.

That matters. Because once debt is controlled, physicians have exceptional cash-flow potential.

But early on, most of that income is consumed by:

- Loan repayment

- Taxes

- Housing

- Catch-up lifestyle spending

Read: [Average Doctor Salary by Specialty (And Why Salary Alone Won’t Make You Wealthy)]

How Specialty Choice Changes Lifetime Earnings

Not all medical specialties are equal financially.

According to Doximity data:

- Family medicine averages $300,800/year

- Plastic surgery averages $619,800/year

- Psychiatry, cardiology, emergency medicine often fall between $300K–$500K

But higher income often comes with:

- Longer training

- More stress

- Higher burnout

- Worse work-life balance

Orthopedics and anesthesiology may pay more—but at real personal cost.

Money alone should not drive specialty choice. But ignoring income differences is equally dangerous.

Net Worth by Age: How Doctors Compare Over Time

Doctors usually lag peers in their 30s.

But the curve flips later.

According to physician wealth studies, by their 50s, roughly 60% of doctors have a net worth between $1–$5 million, while about 25% remain far below that

The gap is not income.

It is behavior.

Read: [Doctor Net Worth vs Financial Freedom: Why They’re Not the Same Thing]

Why High Income Doesn’t Automatically Create Wealth

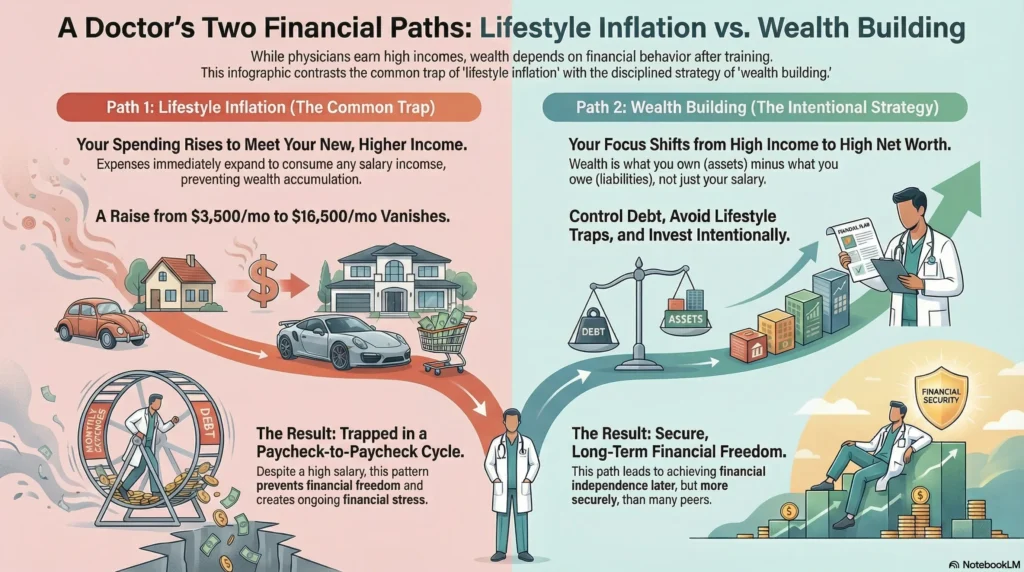

Income does not equal wealth.

Net worth = assets − liabilities

Many physicians earn high salaries but:

- Carry mortgages

- Finance expensive cars

- Delay investing

- Rely solely on 401(k) or 403(b) plans

Without intentional wealth management, income leaks away.

This is why some doctors earning $500K still feel broke.

Lifestyle Inflation and the Cost of “Finally Making It”

Lifestyle inflation is the silent wealth killer.

As one physician recounts, their take-home pay jumped from $3,500/month as a resident to $16,500/month as an attending—and expenses expanded immediately to fill it

Bigger house.

New car.

Private school.

Expensive vacations.

The raise disappears.

This pattern explains why some doctors never escape paycheck-to-paycheck living.

Job Security, Demand, and Long-Term Stability in Medicine

Even with financial challenges, medicine offers unmatched stability.

The **Association of American Medical Colleges projects a shortage of up to 86,000 physicians by 2036

An aging U.S. population amplifies demand.

That security lowers long-term financial risk—something many high-earning careers cannot offer.

The Non-Financial Benefits That Still Matter

Money is not everything.

Surveys show that 70% of physicians say helping patients recover is the most fulfilling part of their work

A Harvard Medical School alum put it bluntly:

“If you want to make a palpable difference in or literally save someone’s life, become a doctor.”

That sense of purpose is rare.

The Hidden Costs: Burnout, Stress, and Time

Burnout is real.

Long work hours, emotional strain, HIPAA compliance, EMRs, and administrative burden weigh heavily.

Many doctors trade:

- Time with family

- Personal health

- Mental bandwidth

These costs must be counted in any honest financial analysis.

How Early Financial Planning Changes the Outcome

Doctors who win financially start early.

They:

- Track net worth

- Control lifestyle inflation

- Invest beyond retirement accounts

- Understand FIRE principles

- Build passive income streams

Early planning changes the slope of the curve dramatically.

Comparing Medicine to Other High-Earning Career Paths

Compared to tech or finance:

- Medicine earns later

- Carries more debt

- Offers greater stability

Compared to entrepreneurship:

- Medicine has lower upside

- Much lower risk

There is no perfect choice. Only trade-offs.

So, Is Being a Doctor Worth It Financially in the Long Run?

Yes, if you treat medicine as a high-income platform, not a guarantee of wealth.

Doctors who:

- Control debt

- Avoid lifestyle traps

- Invest intentionally

- Think long-term

Often reach financial freedom later—but more securely—than peers.

Doctors who don’t often feel trapped despite great salaries.

That choice is the difference.

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Yes, becoming a doctor is financially worth it over the long term for most physicians, but the payoff is delayed and depends heavily on debt management, specialty choice, and spending behavior.

Yes, the investment can pay off over a full career, but only if student loans are controlled and high income is converted into net worth rather than lifestyle inflation.

Doctor salaries are high relative to most professions, but medical school debt and lost earning years mean it often takes 10–15 years after graduation to financially “break even.”

Yes, many doctors struggle financially early in their careers due to high student loans, modest residency pay, and delayed investing, despite strong long-term earning potential.

During residency, doctors face low income, high debt, limited savings ability, and negative net worth, which often continues into the first few attending years.

Student loans delay wealth building by increasing fixed expenses, reducing investing capacity, and keeping net worth negative well into a doctor’s 30s or early 40s.

Doctors improve their long-term financial health by choosing the right way to repay loans. They avoid spending more as they earn more. They invest early when they have money. They follow a written financial plan.

A small number of doctors earn $1 million per year. They usually do this through high-demand surgical specialties, owning practices, offering extra services, or running non-clinical businesses.

Doctors often earn more later in life, but engineers frequently build higher net worth earlier due to lower education costs, earlier investing, and less debt.

Yes, residents are paid a salary, but it is relatively modest and usually insufficient to significantly reduce debt or build meaningful wealth.

Work-life balance changes a lot depending on the specialty and practice setting. Primary care and outpatient specialties often have better balance than surgical or hospital jobs.

Yes, being a doctor is demanding in many ways. It is hard mentally, emotionally, and physically. Doctors have long training, high responsibility, and constant pressure during their careers.

Yes, medicine is a high-stress profession due to long hours, life-and-death decisions, administrative burden, and burnout risk, though stress levels vary by specialty.

Medical school is extremely challenging due to the volume of material, high-stakes exams, long hours, and constant performance pressure.

Becoming a doctor takes more time and is more emotionally demanding than engineering. Both paths are intellectually challenging in different ways.

There is no single best age to start. Entering earlier lowers opportunity cost. Entering later can still be good if you have realistic expectations about money and lifestyle.