Net worth measures accumulated wealth at a point in time, while financial freedom measures whether your assets can sustain your life without relying on active income.

A physician can have a high net worth and still lack financial freedom.

Another doctor can have a lower net worth and be financially independent.

The difference lies in cash flow, liabilities, lifestyle structure, and asset behaviour, not income alone.

This distinction matters because most doctors search for “doctor net worth” when what they actually want is control, flexibility, and long-term security.

Understanding Net Worth vs. Financial Freedom

Net worth = assets − liabilities

For example, a doctor might have a $1 million retirement portfolio, $300k equity in a home, and $100k in cash (assets = $1.4M). If that same doctor owes $400k in student loans and $300k in mortgage debt (liabilities = $700k), the net worth is $700k.

Assets include:

• Cash and savings

• Retirement accounts such as 401(k) and 403(b)

• Brokerage investment accounts

• Real estate and home equity

• Business or practice ownership

Liabilities include:

• Student loans and practice loans

• Mortgages

• Credit card balances

• Personal guarantees

Net worth is a static measurement.

It does not show how much cash you have, your income replacement, or if it is sustainable.

Concept of Financial Freedom

Financial freedom means your assets generate enough income to cover your living expenses without depending on earned income.

This concept is closely tied to:

• Financial independence

• Early retirement

• The F.I.R.E. framework

• Sustainable withdrawal strategies such as the 4% rule

Financial freedom is dynamic.

It depends on cash flow, risk tolerance, expense structure, and time horizon.

A physician reaches financial freedom when stopping work becomes a choice, not a crisis.

High Income vs Wealth Accumulation

High income increases earning potential.

It does not guarantee wealth accumulation.

This distinction explains why many high-earning professionals remain financially constrained.

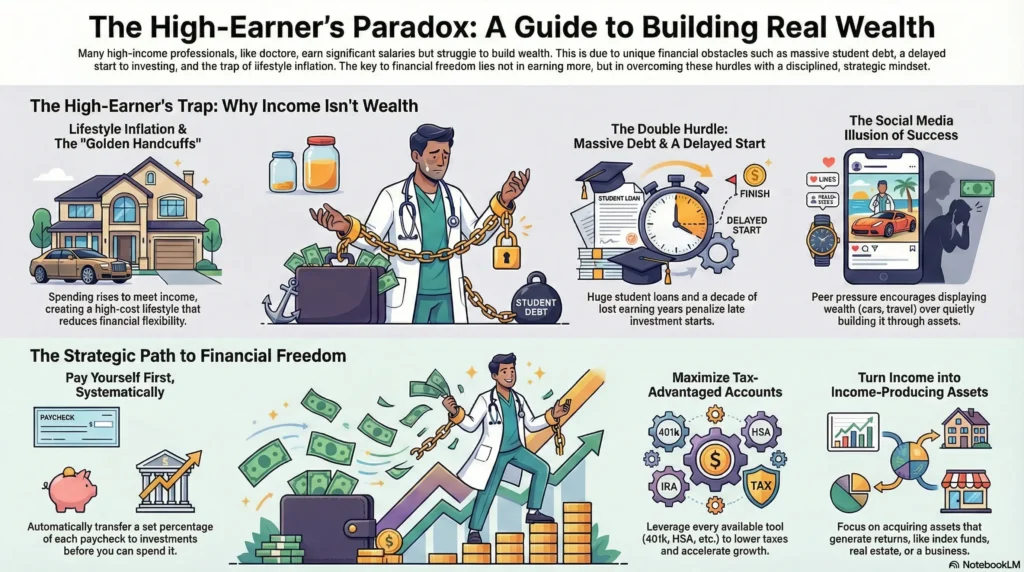

Impact of Lifestyle Inflation

Lifestyle inflation happens when spending increases at the same rate as income.

For example:

- Annual expenses of $120,000 require roughly $3 million to sustain under the 4% rule

- Annual expenses of $200,000 require roughly $5 million

The formula is simple:

Required portfolio = annual expenses ÷ withdrawal rate

Lifestyle inflation increases the required net worth faster than income growth.

This pattern is common among physicians transitioning from residency to attending status.

The Golden Handcuffs Phenomenon

Golden handcuffs describe a situation where high income supports a high fixed-cost lifestyle.

Common contributors include:

• Large primary homes with high mortgages

• Private school tuition and childcare

• High-end vehicles

• Travel and discretionary spending

These costs reduce optionality.

Physicians earning strong salaries may still feel unable to reduce hours, change roles, or exit clinical practice. (https://mergemedical.org/physicians-are-trapped-by-golden-handcuffs)

This is not a net worth problem.

It is a cash flow dependency problem.

Financial Obstacles for Doctors

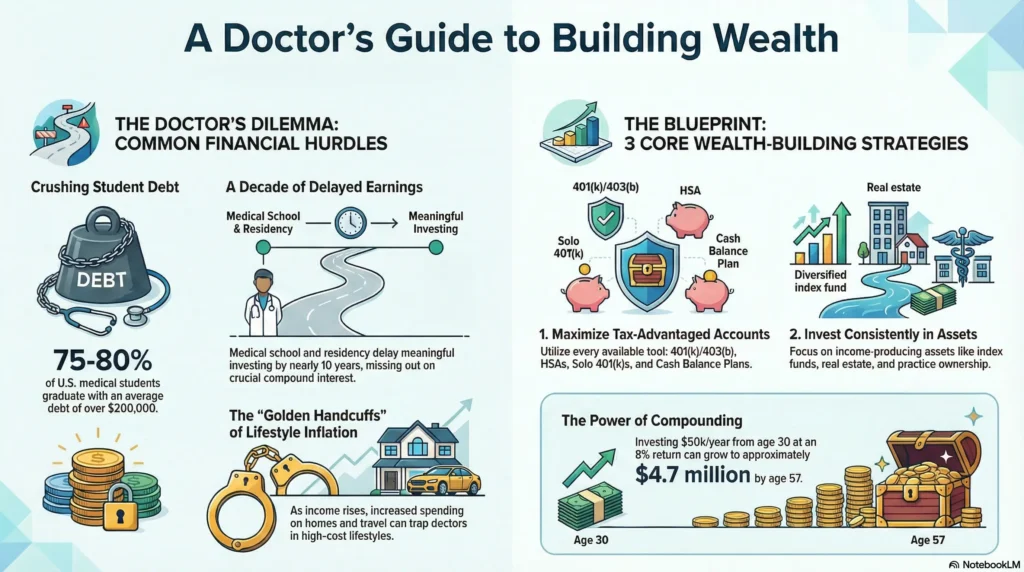

While high pay seems like an advantage, physicians face unique hurdles in wealth building. Two major obstacles are heavy student loan debt and years of delayed high earnings. These challenges mean many doctors start their “wealth journey” behind the curve.

Student Loan Burdens

Medical education costs a lot of money. Today, about 75–80% of U.S. medical students graduate with significant debt. Reports estimate the typical balance at graduation around $200K; some sources even put the average above $264K

Even when doctors qualify for loan forgiveness programs (e.g. Public Service Loan Forgiveness), the odds aren’t in their favour. Historically, only a small fraction of PSLF applications (around 5–6%) succeed. That means most doctors end up repaying loans in full, adding thousands of dollars of interest and delaying wealth accumulation.

Extended Path to High Earnings

Physicians typically reach peak earning years later than other professionals.

Factors include:

• Medical school

• Residency and fellowship

• Licensing and board certification

This delays meaningful investing by nearly a decade.

Compound interest penalizes late starts.

This explains why two doctors with identical salaries can have drastically different net worth outcomes by mid-career.

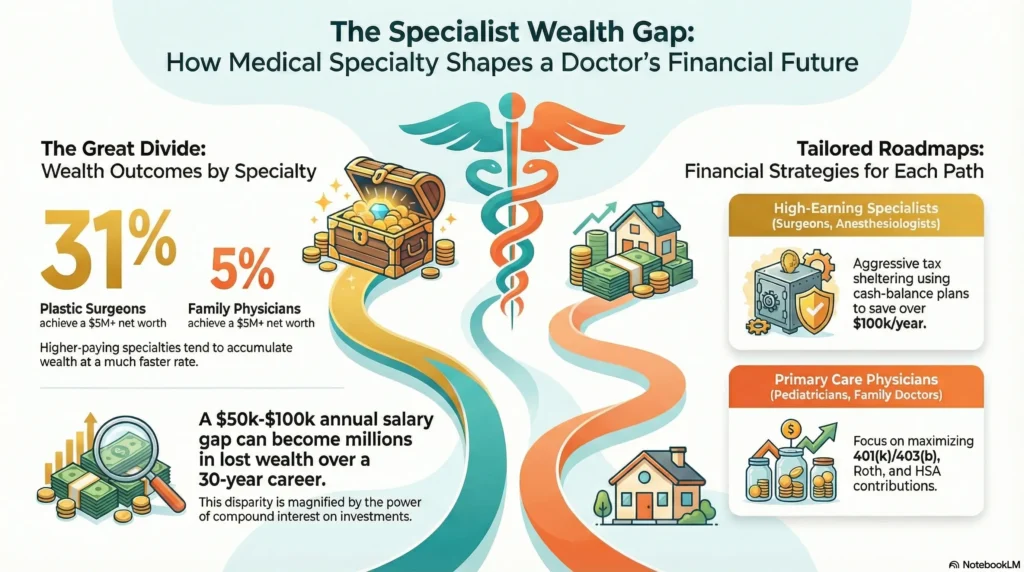

Role of Medical Specialties in Income Disparity

Variability in Income Levels

Physicians in high-paying specialties tend to accumulate wealth faster. For example, recent data show 31% of plastic surgeons report net worth over $5 million, while only about 5% of family physicians reach that level.

This disparity influences net worth outcomes. Over a 30-year career, a difference of even $50K–$100K per year in salary (common between specialties) translates to millions in additional gross income.

If much of that is saved or invested, the compounding advantage can leave primary care doctors significantly behind wealthier specialists, unless they adjust spending or increase savings rates.

Diverse Financial Planning Needs

Because income and cash flow differ by specialty, doctors often need tailored financial strategies.

High-earning specialists like surgeons and anesthesiologists can use aggressive tax-advantaged plans. These include cash-balance pension plans and large profit-sharing 401(k)s. These plans let them save hundreds of thousands of dollars each year in retirement accounts.

By contrast, pediatricians or family doctors (often employed with 401(k)/403(b) plans) might focus on maximizing Roth or HSA contributions and reducing debt.

In short, there is no universal plan.

There is only alignment with personal circumstances.

Influential External Factors

Two big influences are location and the healthcare system environment.

Geographic Impact on Earnings

Where a doctor practices has a major effect on both income and expenses. Some states or regions pay specialists much more due to higher demand or cost of living, while others offer loan forgiveness for practicing in underserved areas.

For instance, rural or inner-city clinics may provide loan repayment incentives (PSLF or state-based), but base salaries can be lower. Conversely, metropolitan areas like New York or San Francisco offer higher salaries but also far higher housing costs and taxes.

A $300,000 salary in a high-cost metro may produce less surplus than a $220,000 salary in a low-cost region.

Geography influences real purchasing power and net worth velocity.

Healthcare System’s Influence

Changes in Medicare and Medicaid reimbursement affect doctors’ take-home pay. Insurance negotiations also have an impact. Practice consolidation changes how much doctors earn.

For example, hospital-employed physicians may see different pay structures or bonus schemes than private practitioners. In countries or states with different healthcare models, physician net worth profiles shift.

In the U.S., the system often rewards high-volume specialists, but also imposes overhead and administrative costs that effectively reduce net pay.

In short, external forces – cost of living, policy, market dynamics – create a backdrop that magnifies income differences. A doctor’s net worth journey is not solely about personal habits; it’s also shaped by where and how they practice. Knowing these factors helps you set realistic expectations. Sometimes, improving financial security means moving to a new place. It can also mean negotiating better contracts or choosing sub-specialties carefully.

Social Media’s Role in Wealth Perception

Many physicians use platforms (Facebook groups, Twitter, Instagram) to share life milestones, travel, and purchases. This can create pressure to match peers’ lifestyles and fuel the “illusion of financial success.”

Comparison Among Peers

It’s human nature to compare. Doctors might see classmates owning fancy homes or sports cars and feel behind, even if their own finances are solid.

In other words, if your colleague’s Instagram feed shows a beachfront condo and world travel, you might subconsciously feel less wealthy—even if you have more in investments but “nothing exciting” to post.

The Illusion of Financial Success

Behind curated social media posts, many physicians carry the weight of student loans, mortgages, or business debt. For example, a surgeon’s Instagram may show a yacht trip, but that same person might have put all cash flow into loan repayment rather than long-term investing.

This illusion matters because it can distort priorities. Doctors may think financial success means having expensive vacations or cosmetic upgrades. They might ignore the importance of real financial security. As the adage goes, “wealthy people aren’t those who wear expensive watches, but those who pay their bills without worry.” For doctors, focusing on building assets and controlling liabilities is what brings true freedom, even if it looks “boring” compared to flashy displays.

Developing a Strategic Financial Mindset

Achieving financial freedom requires a plan and discipline. Doctors thrive on structured thinking, and applying that to money can pay dividends. The first step is acknowledging that high income is no excuse to delay planning: financial planning is as crucial as a treatment plan for long-term stability.

Importance of Financial Planning

Every doctor’s career should include a financial plan. This isn’t just for retirement; it’s how you set priorities (debt repayment, saving, investing) from day one. Research shows that many young physicians underestimate planning needs.

Good financial planning includes budgeting, insurance, and a timeline for goals. Early steps are especially vital. The math of compound interest favors the early bird: a doctor who contributes even 10–15% of income to retirement accounts in her 30s can gain an enormous head start.

For a deeper, tactical breakdown, Read: [Financial Planning for Doctors: How High Earners End Up Wealth-Poor (And What to Do Instead)]

Role of Retirement Accounts

Physicians have access to many retirement vehicles. Maximizing these tax-advantaged accounts is foundational to building wealth.

Typical employed doctors might use 401(k) or 403(b) plans; self-employed or locum docs have Solo 401(k)s and SEP-IRAs; employed docs may also use 457(b) plans in governmental systems.

For physicians, the devil is in the details: contribution limits vary and can add up. In 2025, a standard 401(k)/403(b) limit is $22,500 ($30K+ if over 50). But doctors can often contribute far more via additional vehicles.

- A Solo 401(k) – for independent practice or moonlighting income – allows contributions up to about $70,000 (including employee+employer parts)

- Cash Balance Plans (a type of defined benefit pension) can let late-career doctors tuck away well over $100K per year

- Health Savings Accounts (HSAs) are another powerful tool: contributions are pre-tax and withdrawals for medical expenses are tax-free, essentially a “triple tax-advantaged” account.

Wealth Building Strategies for Doctors

Net worth grows through consistent investment of savings. For doctors, this means turning post-tax dollars into income-generating assets, not just spending them.

Here are some strategic approaches:

Investing in Assets

Traditional assets like index funds, bonds, and real estate are fundamental. Many physician-finance experts (e.g. The White Coat Investor, Physician on FIRE) recommend broad-based, low-cost stock and bond funds to capture market returns over time.

For example, historical S&P 500 returns around 7-8% after inflation show why systematic investing pays off. If a doctor saves 20% of income and invests in a diversified portfolio, over decades that sum can grow into a substantial nest egg.

The key is to focus on income-producing or appreciating assets. For example:

- Stock market: Max out retirement accounts, invest in index funds, reinvest dividends. This provides long-term growth and compounding interest. As one calculation shows, a physician investing $50K/year from age 30 to 57 at 8% could accumulate about $4.7 million.

- Real estate: Buy rental property or real estate funds. This can yield both forced equity (paying down debt increases your stake) and rental income (cash flow).

- Business or practice ownership: For entrepreneurial doctors, owning a practice or medical-related business can vastly increase net worth if managed well. That said, it often requires higher risk tolerance.

Doctors should remember the 80/20 rule: focus on high-impact investments first. Paying off the student loans (often >6%) is effectively a guaranteed return (saving that interest).

Similarly, investing in tax-sheltered accounts yields immediate tax savings.

Once high-interest debts are handled, directing money into assets yields the wealth growth that high income alone won’t.

Over decades, even small annual investments can snowball into millions via compound interest and asset appreciation.

Leveraging Tax Strategies

Reducing taxes legally is a powerful wealth strategy. Doctors should use every tax-advantaged tool available:

- Retirement plan contributions (traditional 401(k)/403(b), Roth accounts, HSAs) lower taxable income and let money grow tax-deferred or tax-free.

- Itemized deductions: Mortgage interest, charitable contributions, and business expenses (for private practitioners) can substantially reduce AGI. For example, a physician who makes large charitable donations or funds a donor-advised fund can save on taxes while supporting causes.

- Tax-efficient investments: Placing high-growth or bond assets in tax-deferred accounts and keeping low-turnover, low-yield investments in taxable accounts can reduce annual tax drag. Also, doctors might favor funds or ETFs that distribute qualified dividends (lower tax rates) over ordinary income.

- Real estate depreciation: If owning rentals, depreciation shields some rental income from taxes. Over time, recaptured depreciation is taxed, but in the meantime it accelerates cash flow after-tax.

- Flexible spending/HSA accounts: Doctors with high-deductible health plans should max out HSAs. This can save taxes now and provide for future medical expenses. Similarly, dependent care FSAs and commuter benefits can trim taxes for eligible expenses.

Physician practices can use strategies like Section 179 expensing to buy equipment. They can set up fringe benefits such as health insurance for spouses and retirement matches. They might also switch to an LLC or PC structure to have more tax planning options.

Overcoming Financial Obstacles

Despite the challenges above, many doctors do achieve financial independence. The transition often requires both practical changes and mindset shifts.

Two common final hurdles are burnout and the temptation to focus on short-term gains over long-term wealth.

Understanding Career Burnout and Its Financial Impact in Medicine

Career burnout – emotional exhaustion from work – is widespread in medicine. While burnout is a clinical/psychological issue, it has financial implications.

A burned-out doctor may be tempted to make impulsive financial decisions: taking higher-paying but more stressful jobs, overspending in the short term, or rushing to quit without a plan.

Conversely, a clear financial plan can actually combat burnout by providing hope and control.

You can reduce financial stress and burnout by making a realistic budget that includes occasional rewards. You should also automate your savings to avoid constant worry. Try to balance work and life to protect your time. Sometimes, accepting a pay cut can reduce stress.

Also, engaging with communities like Physician on FIRE or financial mentors can provide support and ideas.

Remember: financial freedom can mean the option to work less or in a different way, which directly alleviates burnout.

Focusing on Long-Term Wealth Creation

The greatest mistake high earners can make is confusing current income with real wealth. Overcoming that requires discipline: consistently channeling money into investments, even when life is busy. It’s crucial to resist the lure of instant gratification.

For doctors, turning wealth creation into a habit helps. Simple strategies include paying yourself first. This means transferring a set percentage of each paycheck into investments before deciding on other expenses. Another strategy is keeping lifestyle growth slower than income growth.

For example, if a bonus or raise comes in, a rule of thumb is to save at least 50% of it rather than increasing spending by the full amount.

Building wealth isn’t a sprint, it’s a marathon. It involves choices like buying index funds instead of day trading, holding properties through market swings, and prioritizing retirement account contributions even when tempted by short-term purchases.

Over decades, these disciplined actions separate doctors who achieve freedom from those who don’t, regardless of how similar their early net worth looked.

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

- 🎧 Listen to the audio version of this guide while commuting or between shifts

- 📘 Read our book on Amazon for a structured walkthrough of financial freedom for doctors

- 📥 Download the free LIFTOFFNOW ebook to understand the full framework

- 📞 Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Yes, being a doctor is financially worth it over a full career, but only if income is converted into wealth deliberately.

Physicians have high earning potential, strong job security, and long-term income stability. Delayed earnings, student loan debt, and lifestyle inflation can reduce financial outcomes. This happens if people do not manage them carefully.

In short, medicine pays well, but wealth is not automatic.

Net worth is compared to a financial thermometer because it measures financial status at a single point in time, not financial sustainability.

Like a thermometer, it shows a snapshot, not the full story.

Net worth does not indicate:

• Cash flow

• Liquidity

• Income replacement ability

Financial freedom depends on how assets behave over time, not just their total value.

Being rich describes having a high net worth, while financial freedom means not needing to work to maintain your lifestyle.

A rich person may still rely on active income.

A financially free person does not.

Financial freedom is defined by cash flow and expense coverage, not appearances or account balances.

A doctor’s net worth measures accumulated assets minus liabilities, while financial freedom measures whether those assets can replace earned income.

Net worth answers “how much you own.”

Financial freedom answers “can you stop working if you choose?”

Doctors often achieve high net worth before achieving freedom because assets are illiquid or expenses remain high.

Because net worth can be tied up in illiquid assets while expenses and income dependence remain high.

Common examples include:

• Home equity that does not generate cash flow

• Retirement accounts locked until retirement age

• Practices that require active involvement

Financial freedom requires income-producing assets, not just asset accumulation.

The main factors are lifestyle inflation, debt obligations, delayed investing, and income dependence.

Additional contributors include these items.

• Student loan debt

• High fixed expenses

• Lack of investing outside retirement accounts

• Burnout limiting long-term earning capacity

These factors prevent net worth from translating into freedom.

Liabilities reduce cash flow and increase income dependence, even when net worth appears high.

Student loans, mortgages, and practice loans require ongoing payments.

High liabilities raise the income needed to maintain lifestyle, delaying financial independence.

Lifestyle inflation increases required income and investment size faster than wealth grows.

As expenses rise, the portfolio needed to support that lifestyle also rises.

This keeps doctors working longer despite increasing net worth.

Doctors achieve financial freedom by aligning expenses, assets, and cash flow with long-term independence goals.

Key actions include:

• Controlling fixed expenses

• Investing outside retirement accounts

• Reducing debt strategically

• Building income-producing assets

Freedom comes from structure, not income level.

Doctors should adopt habits that prioritize cash flow, automation, and long-term consistency.

Examples include:

• Paying themselves first

• Automating investing

• Avoiding lifestyle upgrades tied to income increases

• Using rules instead of emotions for decisions

These habits convert earnings into lasting independence.

Some doctors are rich by net worth standards, but many are not financially free.

High income creates the appearance of wealth, but debt and expenses often offset it.

True wealth is defined by optionality and control, not salary.