Doctors should choose investment types based on how much risk they can handle, how long they can stay invested, and what financial goals they are trying to reach. The right mix changes depending on debt, career stage, income stability, and family needs, but every physician portfolio is built by combining low, moderate, and high risk asset classes in a structured way.

You earn well. But your financial life is not simple. Long training in medical schools, delayed earning years, student loans, complex tax situations, and intense clinical schedules mean your investing strategy must be intentional. Guessing is expensive. Overconfidence is worse.

You need a framework.

And it starts with understanding how investment types connect to risk.

Risk for the Medical Professionals

You deal with risk daily. Every diagnosis has chances of different outcomes. Every treatment has tradeoffs. Investing works the same way.

Your investment risk tolerance is your ability to handle portfolio ups and downs without panic, poor decisions, or needing to sell at the wrong time.

Your risk tolerance depends on:

- Income stability from your medical practice

- Debt load and required payments

- Years until you need the money

- Emotional comfort with market swings

- Existing savings account buffers

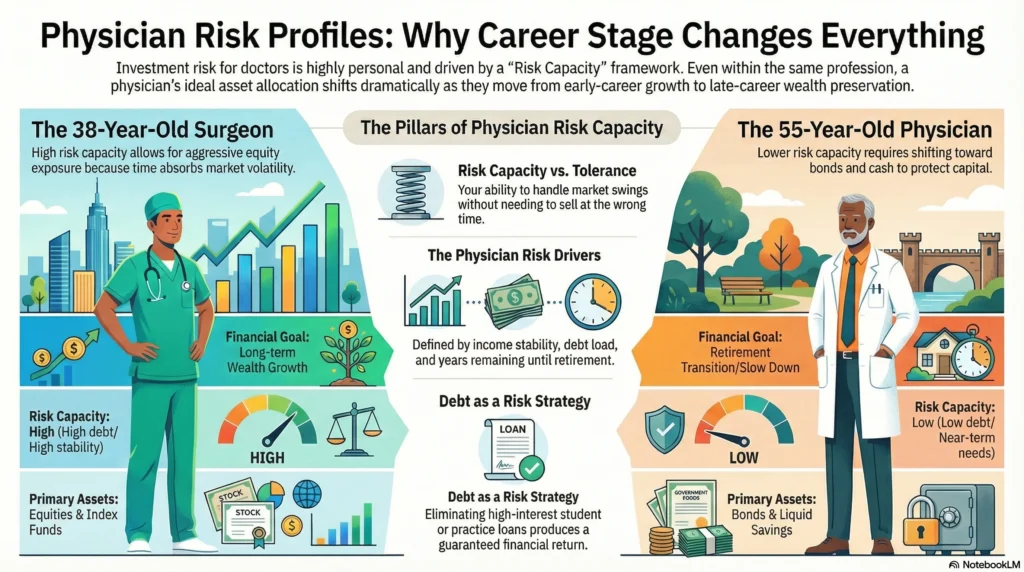

Doctors often underestimate how personal this is. A 38 year old surgeon with stable income and no major debt can handle more equity exposure than a 55 year old physician planning to slow down in five years.

You also face a unique psychological factor. You are trained to act when something goes wrong. Markets punish that instinct. The best investing strategy often requires patience, not reaction.

Risk is not something to eliminate. It is something to manage.

Read: [How Doctors Can Gain Financial Clarity Without Obsessing Over Every Decision]

A Physician’s Guide to Investment Types and Their Risk Spectrum

Most physician portfolios are built from familiar asset classes plus selected alternative investments. As explained in physician-focused investing resources discussing stocks, bonds, mutual funds, real estate, and ETFs as core portfolio building blocks, each investment type carries a different risk and return profile.

Think of these as layers.

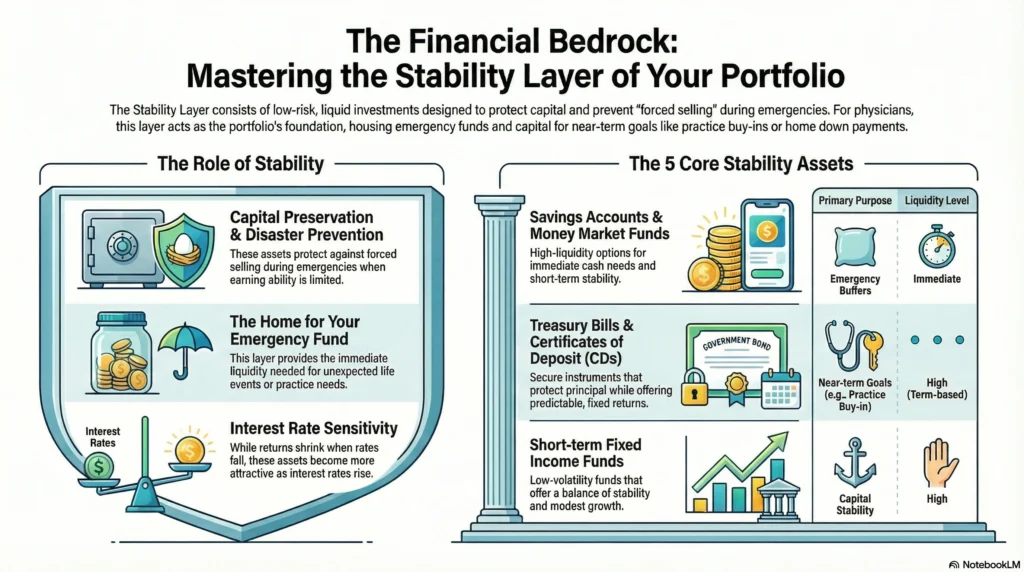

Low-Risk and Liquid Investments

These protect capital and provide stability.

Examples:

- Savings account balances

- Money market funds

- Treasury bills

- Certificates of deposit

- Short-term fixed income funds

A savings account and certificates of deposit will not grow wealth fast, but they protect against forced selling when emergencies happen. That is critical for doctors whose time is limited and whose earning ability depends on health and licensure.

Low-risk investments are where your emergency fund lives. They also fund near-term needs like a practice buy-in or home down payment.

Interest rates matter here. When interest rates rise, short-term fixed income becomes more attractive. When interest rates fall, returns shrink, but stability remains.

These assets do not build financial independence alone. But they prevent financial disaster.

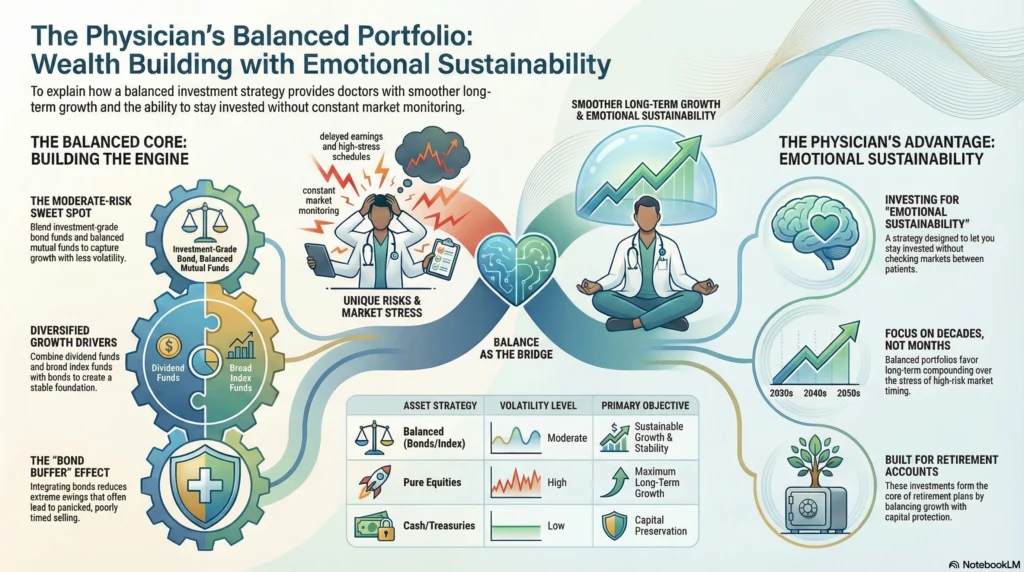

Moderate Risk: Balancing Growth with Stability for Core Portfolios

This is where many physicians should spend a large portion of their portfolio.

Moderate-risk investments blend stability and growth. As described in guidance on balanced portfolios using corporate bonds and diversified mutual funds, these include:

- Investment-grade bond funds

- Balanced mutual funds

- Dividend stock funds

- Broad market index funds combined with bonds

Moderate risk investments smooth the ride. They do not swing as wildly as pure equities, yet they grow faster than cash.

This is the core of many retirement accounts because it aligns with long-term financial goals while respecting that doctors cannot monitor markets all day.

Your target asset allocation often begins here, then adjusts depending on age and comfort level.

Higher Risk, Higher Reward: Strategic Growth Components

High risk assets drive long-term growth. They also test your discipline.

As explained in discussions of equities and commodities having larger price swings but higher potential returns, this group includes:

- Equity index funds

- Sector-specific stock funds

- Small-cap and emerging markets funds

- Commodities exposure

Index funds play a huge role here. Broad market index funds provide diversification at low cost and form the backbone of many physician portfolios.

Higher risk does not mean reckless. It means accepting short-term drops in exchange for long-term growth.

Doctors early in career often benefit from heavier exposure here because time absorbs volatility.

But only if your target asset allocation is intentional, not emotional.

Read: [Active vs Passive Investing: What Works Best for Busy Doctors?]

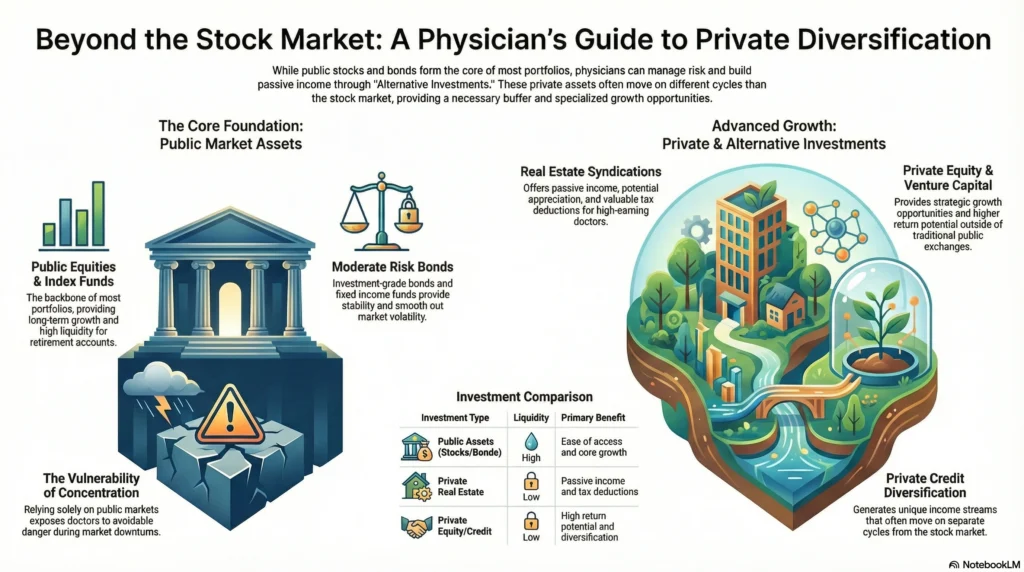

Alternative Investments: Specialized Risk and Opportunities for Accredited Doctors

For physicians with higher net worth, alternative investments expand investment opportunities beyond public markets.

As noted in physician-focused resources discussing private equity, hedge funds, venture capital, and real estate syndications, these include:

- Private equity

- Venture capital

- Real estate syndications

- Private credit

Real estate investing is common among doctors seeking passive income and diversification. Real estate provides income, potential appreciation, and tax deductions, but it also involves illiquidity and operational risk.

Alternative investments require more due diligence, longer timelines, and tolerance for complexity. They should supplement, not replace, core index funds and fixed income.

Robust Risk Management Strategy for Physicians

Choosing asset classes is step one. Managing them is step two.

The Power of Diversification: Spreading Risk Across Asset Classes

Diversification means spreading money across asset classes so one downturn does not wreck your portfolio.

Stocks fall. Bonds may hold. Real estate behaves differently. Alternatives move on separate cycles.

Your target asset allocation defines how much of each you hold. That allocation is the engine of your risk management.

Doctors who concentrate too heavily in one area, such as real estate or a single stock, expose themselves to avoidable danger.

Read: [The Biggest Financial Mistakes Doctors Make in Their 30s and 40s (And How to Avoid Them)]

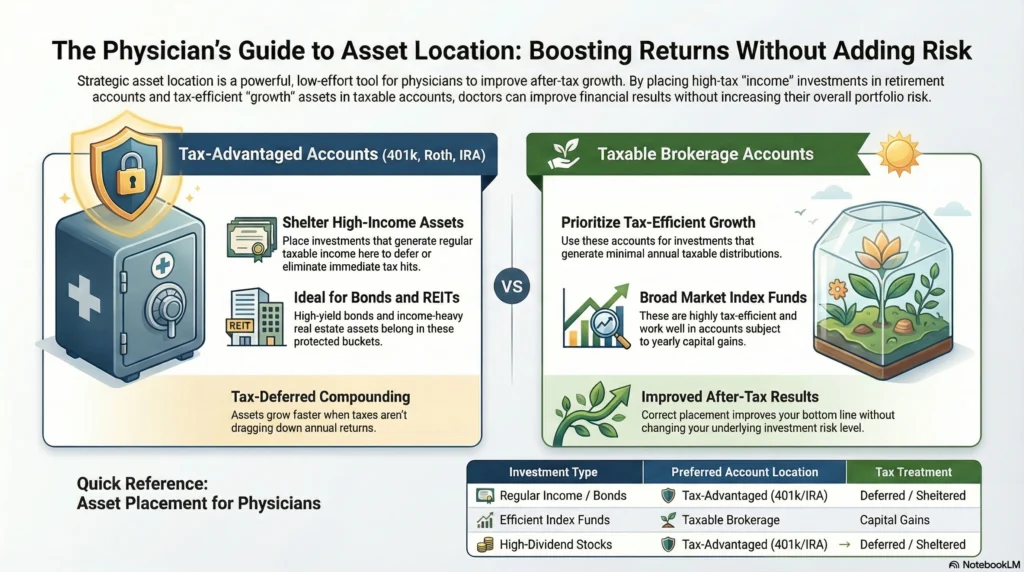

Strategic Asset Location and Tax-Efficient Investment Strategies

Where you place investments matters as much as what you buy.

Tax-advantaged accounts like 401(k)s and Roth IRAs are ideal for assets that generate regular taxable income. Taxable accounts may hold tax-efficient index funds.

Good asset location improves after-tax growth without changing risk.

Interest rates also affect bond strategy inside retirement accounts versus taxable accounts.

Active Management of Your Investment Strategy

Active management does not mean day trading. It means review.

Life changes. Market conditions change. Your target asset allocation should be revisited yearly.

Rebalancing means selling some of what grew and buying what fell to restore balance. This keeps risk steady and prevents drift.

An investing strategy without review becomes accidental.

Debt Management as a Core Risk Strategy

Debt is part of your risk profile.

High interest rates on loans reduce flexibility. Student loans, mortgages, and practice loans affect how aggressively you can invest.

Balancing debt payoff and investing is part of risk management. Eliminating toxic debt often produces a guaranteed return equal to the loan interest rate.

Read: [Lifestyle Inflation: The Silent Wealth Killer for Doctors]

Accelerating Wealth Building for High-Earning Physicians

Once your foundation is stable, you can lean into growth.

High income allows larger investments into equities, index funds, and real estate investing. The key is calculated exposure, not blind risk.

Physicians with strong cash flow can increase equity exposure while maintaining emergency reserves and appropriate insurance.

Experience in medicine helps. You follow protocols. You track outcomes. Apply that same discipline to your investing strategy.

Stick to a target asset allocation. Ignore noise. Focus on decades, not months.

Common Pitfalls and Professional Guidance

Physicians often:

- Overestimate their risk tolerance

- Chase hot investment opportunities

- Ignore tax implications

- Delay investing due to busy schedules

Education is important..

🎧 Listen to the audio version during commutes

📘 Read the book on Amazon for a structured wealth framework

📥 Download the free ebook on investment tips and risk

📞 Book a free 10-minute clarity call

🧑⚕️ Join MedMoneyIncubator to connect with other physicians

FAQ

The four main types of investment risk are market risk, interest rate risk, credit risk, and inflation risk. Market risk is the chance that stock or real estate values fall. Interest rate risk affects bonds when rates rise or fall. Credit risk is the chance a borrower cannot repay. Inflation risk is the loss of purchasing power over time. Most physician portfolios face all four, which is why diversification across asset classes matters.

The best investments for doctors are diversified index funds, high-quality bond funds, and selected real estate, matched to their time horizon and risk tolerance. Doctors usually benefit from low-cost index funds for long-term growth, fixed income for stability, and real estate for diversification and passive income. The right mix depends on debt level, income stability, and financial goals.

A physician’s guide to investing is a structured approach that aligns asset allocation, risk tolerance, taxes, and time constraints with a doctor’s career and income pattern. It focuses on automation. It also focuses on diversification, tax-advantaged accounts, and avoiding emotional investment decisions. The goal is steady long-term growth without constant monitoring.

Alternative investments are assets outside traditional stocks and bonds, such as private equity, venture capital, and real estate syndications. They can offer diversification and higher return potential, but they come with lower liquidity, more complexity, and higher risk. Doctors with strong cash flow, a solid core portfolio, and long time horizons may consider a small allocation.

You manage investment risk by diversifying across asset classes, keeping an emergency fund, and sticking to a target asset allocation. Rebalancing periodically, using a mix of equities and fixed income, and avoiding panic selling during downturns reduce long-term damage. Risk is controlled through structure, not prediction.

If you do not have access to complex investments, focus on low-cost index funds, a solid savings account buffer, and steady contributions to retirement accounts. Simple portfolios often outperform complicated ones because they reduce fees, emotional decisions, and mistakes. Being consistent matters more than being sophisticated.