Doctors retire early when they turn their high income into long-term investments on purpose. They control how their lifestyle grows. They use tax-efficient accounts. They follow a clear financial plan that focuses on financial independence instead of spending to show status. The path changes based on debt, income from your specialty, family needs, and career goals. But the main formula stays the same. Earn good money. Save a lot. Invest wisely. Build many income sources that reduce the need to work full-time.

Many physicians want early retirement but few reach it without deliberate strategy. Training delays income, and doctors often finish with debt exceeding $200,000.

That postpones investing during years when compound interest matters most. Add long hours, rising lifestyle costs, and burnout, and it is easy to see why 58% of physicians retire after age 65.

Early retirement is realistic, but it must be engineered.

Read: [How Much Money Do Doctors Need to Retire at 50? A Realistic Breakdown]

How Doctors Achieve Realistic Early Retirement

Early retirement in the medical profession does not come from luck. It comes from understanding leverage points doctors uniquely have and using them correctly.

High Earning Potential as an Accelerator

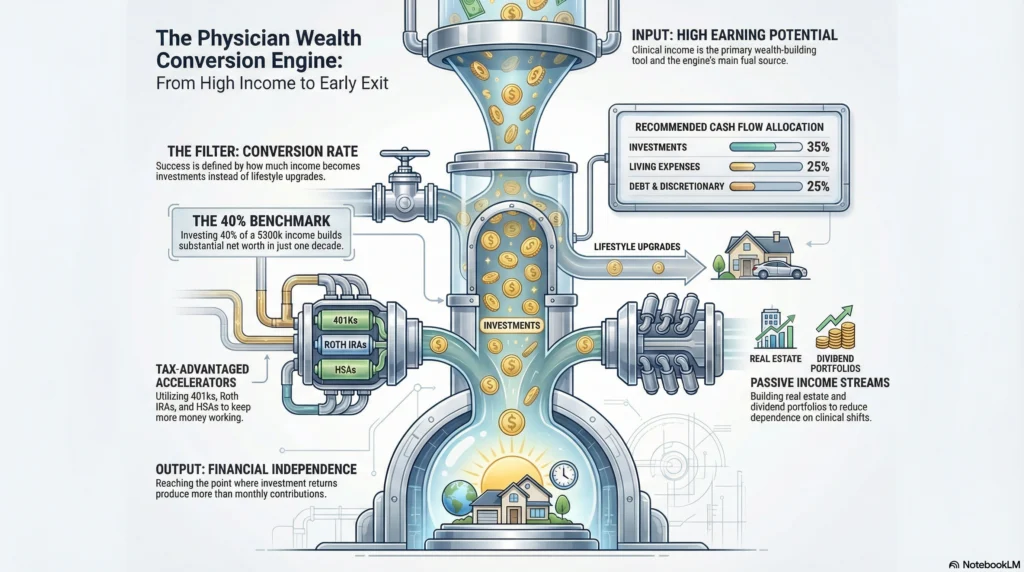

Your income is your primary wealth-building tool. Once attending-level pay begins, your earnings jump dramatically compared to most professions. That income, directed properly, shortens the timeline to financial independence.

The key difference between doctors who retire early and those who work into their late 60s is not intelligence. It is conversion rate. How much of income becomes investments instead of lifestyle upgrades.

If a physician earning $300,000 invests 40 percent of income, that is $120,000 per year compounding. At a moderate 6 to 7 percent return, that level of contribution builds substantial net worth in a decade. Someone saving 10 percent will need much longer and remain tied to full-time work.

This is why high income is an accelerator. But it only works if spending does not expand equally.

Leveraging Powerful Tax-Advantaged Accounts

Tax-advantaged accounts help doctors keep more of their money working instead of losing it to income taxes each year.

Physicians can use:

• 401k or 403b plans

• Traditional IRA

• Roth IRA

• Backdoor Roth IRA

• Health Savings Accounts

• Defined benefit plans for high savers

These accounts matter because money grows faster when taxes are deferred or eliminated. A Roth IRA is especially powerful for young doctors because withdrawals later can be tax free. Using tax-advantaged accounts early increases investment returns over time.

Doctors who delay contributions often try to “catch up” later but lose years of growth that compound interest would have delivered.

Read: [How Much Do Doctors Need in a 401k to Retire Comfortably?]

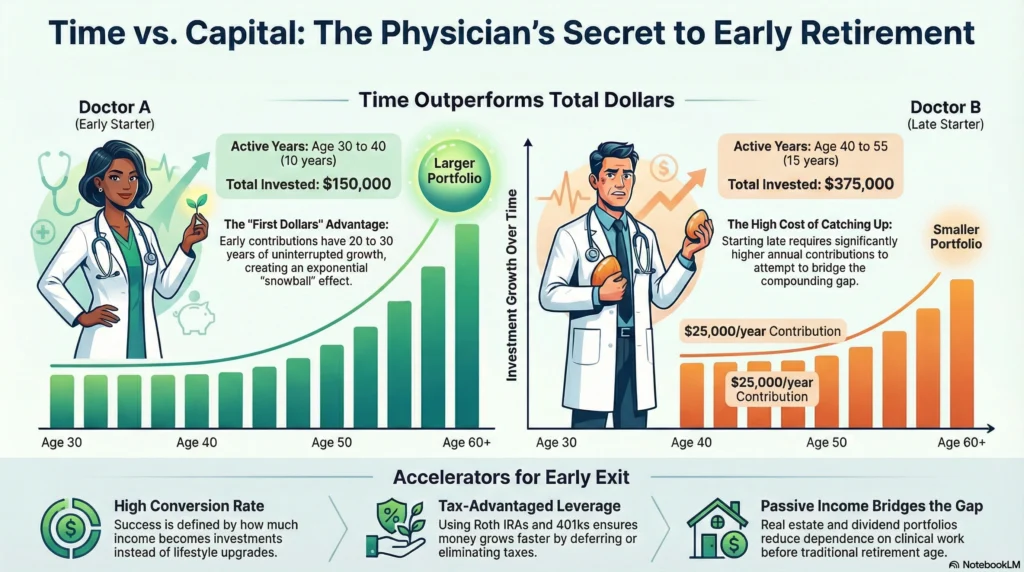

The Magic of Compound Interest and Early Investment

Compound interest rewards time more than contribution size. This is one of the most misunderstood aspects of early retirement.

Example:

Doctor A invests $15,000 per year from age 30 to 40 and then stops. Doctor B waits until 40 and invests $25,000 per year until 55.

Despite investing less total money, Doctor A can still end up with more because the first dollars had 20 to 30 years to grow.

Compound interest works quietly. But once growth accelerates, investment returns begin producing more than contributions. That is when financial independence becomes visible.

Doctors who begin investing during medical school or residency, even with small amounts, dramatically improve outcomes.

Strategic Financial Planning and Professional Guidance

You can build a retirement plan alone, but physicians face unique complexities such as irregular income, medical expenses, practice ownership, and late savings start. Structured financial planning provides clarity.

Planning means:

• Estimating future lifestyle spending

• Determining required portfolio size

• Choosing asset allocation

• Setting savings rates

• Creating a distribution strategy for retirement income

A financial advisor or planner experienced with physicians can help map the path. Planning transforms early retirement from abstract hope into a measurable timeline.

The Blueprint for Early Exit: Actionable Financial Strategies

Early retirement needs financial actions that work together. It is not about making single decisions.

Fast Debt Repayment

Medical school debt often delays investing. Paying down high interest loans is like earning a guaranteed return equal to the interest rate.

Strategies include:

• Refinancing student loans when possible

• Using bonuses toward principal

• Applying extra shifts income toward debt

Reducing medical school debt improves cash flow planning and frees money for investments.

Aggressive Saving and Investment Discipline

Early retirement demands high savings rates. Many early retirees in the FIRE movement save 30 to 50 percent of income.

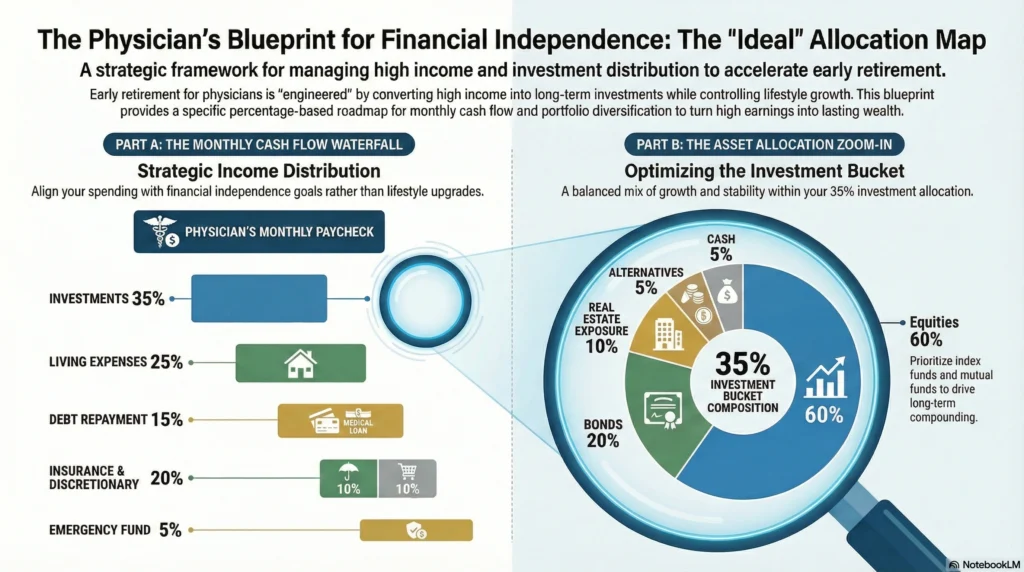

A structured asset allocation could look like:

• 60 percent equities through index funds and mutual funds

• 20 percent bonds

• 10 percent real estate exposure

• 5 percent alternatives

• 5 percent cash

This allocation balances growth and stability. Investment strategies should be automated so saving happens before money reaches spending accounts.

Diversifying Income and Building Passive Streams

Doctors pursuing early retirement reduce dependence on clinical work by creating passive income.

Examples include:

• Real estate rental properties

• Dividend focused portfolios

• Digital education products

• Consulting

Rental properties can produce steady passive income with property management support. Real estate also diversifies income away from the hospital paycheck.

Passive income helps bridge the gap before traditional retirement age and reduces pressure to maintain full-time work.

Smart Budgeting and Cash Flow Planning

Cash flow planning aligns spending with goals. A physician budget might allocate:

• 35 percent investments

• 25 percent living expenses

• 15 percent debt

• 10 percent insurance

• 10 percent discretionary

• 5 percent emergency fund growth

This structure ensures money flows toward financial independence rather than disappearing into lifestyle creep.

Cash flow planning is ongoing. As income rises, investment contributions should rise too.

A Roadmap for Residents and Young Attendings

Habits built early determine outcomes later.

The Power of Early Planning During Residency and Fellowship

Even on lower pay, residents should:

• Open a Roth IRA

• Build an emergency fund

• Avoid luxury upgrades after training

• Understand loan repayment options

Starting early gives compound interest more time. A small Roth IRA contribution in residency can outperform a larger one started years later.

Learning from the Physician Community and Resources

Learning about money helps you make progress faster. Many doctors pursuing early retirement share strategies, mistakes, and lessons learned. Learning from peers shortens the trial and error phase.

This includes reading physician-focused financial guides, joining communities, and using structured planning frameworks designed for doctors.

Read: [When Do Doctors Retire? Average Retirement Age for Physicians Explained]

Also Check Out: [Financial Freedom Calculator for Doctors]

You do not have to figure out early retirement alone.

Most doctors never learned personal finance in medical school. Yet you are expected to make six figure decisions about investing, debt, insurance, and long term wealth. That gap is exactly why having the right environment and guidance changes everything.

If this guide opened your eyes but also feels like a lot, that is normal. Early retirement and financial independence are built step by step, not in one weekend of reading.

Here are simple ways to move forward without pressure:

🎧 Listen to the audio version of this guide during your commute or between shifts so learning fits your schedule.

📘 Read the Freedom for Doctors book on Amazon for a structured walkthrough of how physicians turn high income into lasting wealth and optional work.

📥 Download the free Physician Financial Flight Plan ebook to understand the full LIFTOFFNOW framework and how the pieces connect.

📞 Book a free 10 to 15 minute clarity call if you want to talk through your situation and identify your next best step. No pitch. Just direction.

🧑🧒🧒 Sign up on the MedMoneyIncubator platform for free and connect with physicians across the globe who are actively working toward early retirement, better investing habits, and smarter money decisions.

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into real financial independence and the freedom to choose how long they keep working.

FAQ

Early retirement is realistic for doctors who consistently save a high percentage of income, invest early, and control lifestyle inflation. It becomes difficult when spending rises with income, debt lingers, or investing starts late.

No, it is not too late, but the strategy changes from slow compounding to high savings and focused investing. Doctors starting later often need to save 30 to 50 percent of income, reduce big expenses, and use tax advantaged accounts aggressively to catch up.

Some doctors are retiring early, but most still retire in their 60s because high spending, late starts, and career demands delay financial independence. Early retirement happens more often among physicians who plan intentionally and invest aggressively.

Doctors often wait to retire because of lifestyle costs. They support their family. Their identity is tied to being a doctor. They feel they are not ready financially. Some also continue working because they enjoy medicine when workload and stress are manageable.