After you reach the maximum contribution to your 401(k), the next step is to keep saving for retirement. You can do this by using a mix of IRAs, brokerage accounts, and other tax-smart investment options. Use these in an order that keeps your options flexible, lowers taxes, and protects your long-term freedom.

The exact order can vary based on income limits, age, and goals, but the core framework stays the same for most physicians.

If you’re feeling unsure right now, that’s normal.

Very few people ever reach this point.

According to Investopedia, despite generous contribution limits, only a small percentage of workers ever max out their 401(k)s with the highest proportion found among those age 55–64.

So let’s slow this down and walk it through properly.

What “Maxing Out” Your 401(k) Really Means

To max out a 401(k) simply means you’ve hit the annual employee contribution limits set by the IRS.

According to IRS contribution limits for 2026, the maximum you can invest in a 401(k) as an employee is $24,500 with additional catch-up contributions of $8,000 if you’re age 50 or older.

For physicians, this often happens earlier than expected because income rises quickly after training.

But here’s the part many miss:

Maxing out a 401(k) does not mean you’ve optimized your retirement plans.

It means you’ve filled one container.

A very important container.

But still just one.

Why Doctors Should Look Beyond 401(k) Plans

401(k) plans are powerful because of three things:

- Pre-tax or Roth contributions

- Automated discipline

- An employer match (when available)

That employer match alone is free money, which is why it’s always step one.

But once you’ve captured the employer match and hit contribution limits, continuing to rely on 401(k) plans alone creates blind spots:

- Limited access before retirement

- Early withdrawal penalties if money is needed sooner

- Less control over tax timing later in life

That’s why expanding beyond a single account matters.

This is also where understanding the difference between accounts becomes critical.

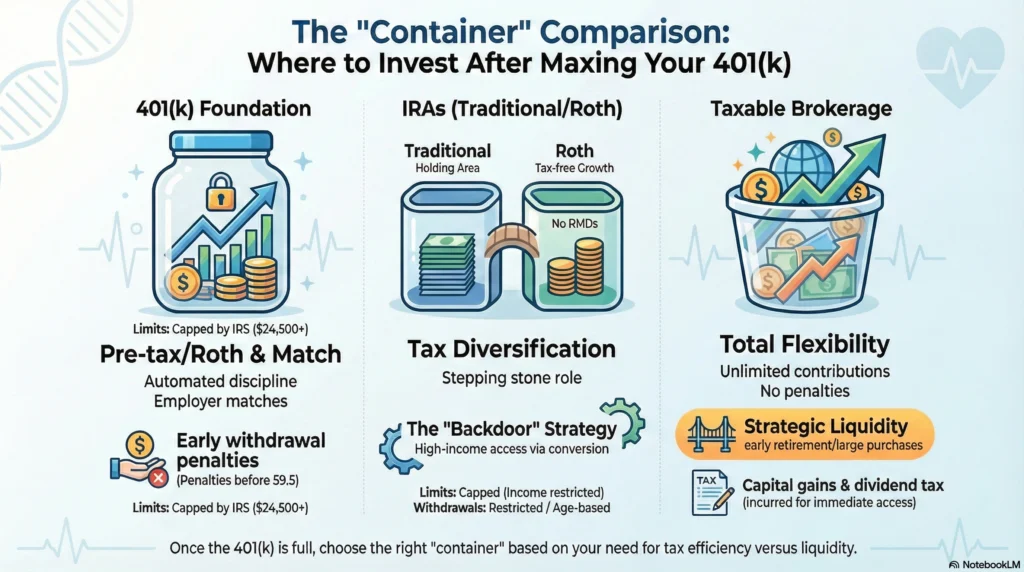

Exploring Individual Retirement Accounts (IRAs)

Once you max out a 401(k), the most common next step is an individual retirement account.

One common strategy after maxing a 401(k) is contributing to a Traditional or Roth IRA, which continues tax-advantaged retirement savings.

IRAs sit outside your employer.

You control them.

And they give you more tax flexibility long-term.

Traditional IRA: How It Fits After a 401(k)

A Traditional IRA allows you to contribute pre-tax dollars, depending on income and participation in employer plans.

For many doctors, the deduction may be limited due to income limits — but the account can still play a role in planning.

A Traditional IRA often acts as:

- A stepping stone for conversions later

- A tax-deferred holding area

- A planning tool, not just a deduction tool

Roth IRA: Why Doctors Care So Much About It

A Roth IRA flips the tax equation.

You pay taxes now.

But future withdrawals — including growth — are tax-free.

That’s why Roth IRA accounts are so valuable for physicians who expect higher lifetime income.

They provide:

- Tax diversification

- Protection against rising future tax rates

- No required minimum distributions

Because of income limits, many doctors cannot contribute directly.

That’s where planning comes in.

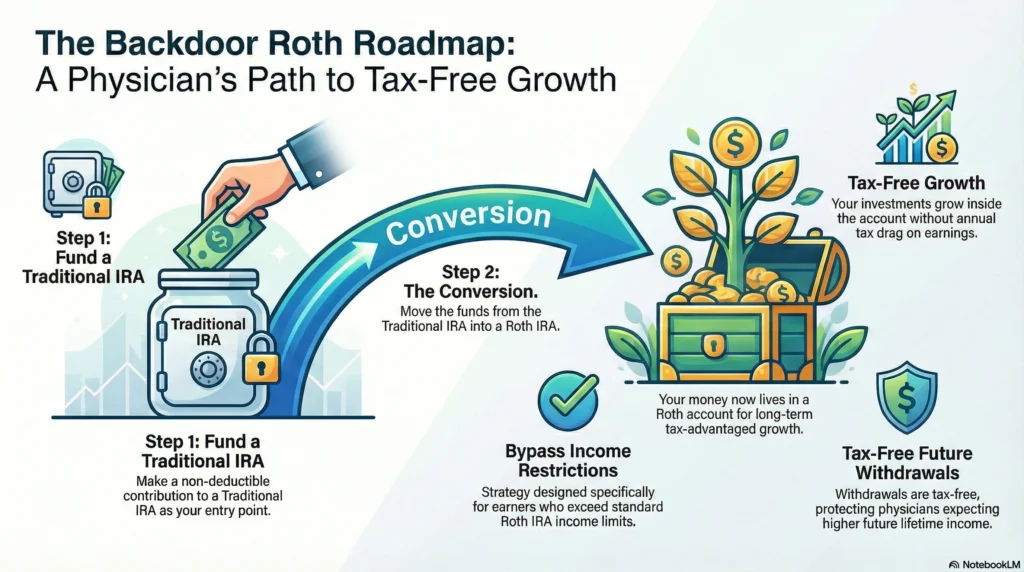

When the Backdoor Roth Comes Into Play

If your income exceeds Roth IRA income limits, you’re not shut out.

High-income earners often use a Backdoor Roth strategy to keep accessing Roth benefits.

At a conceptual level, the Backdoor Roth involves:

- Contributing to a Traditional IRA

- Converting it to a Roth IRA

No tactics here.

No execution steps.

Just awareness — because this option exists for many physicians.

In more advanced cases, some doctors also explore a Mega Backdoor Roth, which uses after-tax contributions inside certain 401(k) plans.

This is not beginner-level execution, but it’s important to know the term.

Read: [401k Investment Alternatives]

Using a Brokerage Account for Flexibility

Once retirement accounts are filled, the next bucket is often a brokerage account.

A taxable brokerage account is another good option after you reach the 401(k) limits. It offers flexibility and has no limits on how much you can contribute. However, it does not have the same tax benefits as retirement accounts.

A brokerage account gives you:

- Unlimited contributions

- No income limits

- No early withdrawal penalties

That flexibility is why doctors use it.

Taxable Brokerage Account: What You Need to Understand

A taxable brokerage account does not shield you from taxes.

You may owe:

- Capital gains when assets are sold

- Capital gains taxes on realized profits

- Taxes on dividends and interest

But this doesn’t make it bad.

It makes it strategic.

Used properly, brokerage accounts support:

- Early retirement planning

- Bridge income before retirement age

- Large purchases without penalties

This is where long-term thinking matters.

Read: [Where to Invest Money to Get Good Returns for Beginners]

The Role of Mutual Funds Inside and Outside Retirement Accounts

Whether inside a 401(k), IRA, or brokerage account, a mutual fund is simply a vehicle that holds many investments at once.

Doctors often prefer mutual fund investing because it:

- Reduces single-stock risk

- Simplifies diversification

- Supports long-term discipline

The key difference is where the mutual fund lives.

Inside retirement accounts, you get tax advantages.

Inside brokerage accounts, you trade tax efficiency for flexibility.

Health Savings Accounts: Often Missed, Still Powerful

If you’re eligible, health savings accounts deserve attention.

They combine:

- Pre-tax contributions

- Tax-free growth

- Tax-free withdrawals for qualified medical expenses

That’s a rare triple benefit.

Many physicians use an HSA as:

- A medical expense buffer

- A long-term retirement savings supplement

It’s not flashy.

But it’s efficient.

Why Emergency Cash Still Matters After You Max Out

Once income rises, many doctors feel tempted to invest everything.

Don’t.

A properly sized emergency fund protects your investments from forced selling.

This matters most during:

- Market downturns

- Job transitions

- Health or family disruptions

Liquidity isn’t wasted money.

It’s insurance for your plan.

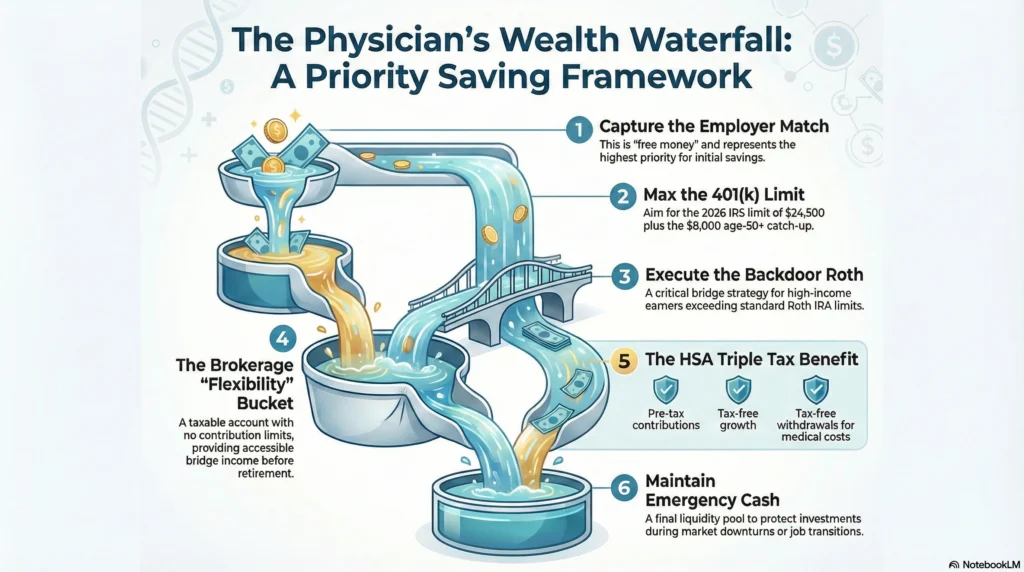

How All of This Fits Together

After you max out your 401(k), a balanced framework often looks like this:

- Capture full employer match

- Max out 401(k) plans

- Explore Roth IRA or Backdoor Roth options

- Use a brokerage account for flexible investing

- Layer in health savings accounts if eligible

- Keep emergency cash intact

Each step builds on the last.

No rush.

No panic.

No guessing.

If income goals shift toward predictable cash flow later, read: Where to Invest Retirement Money for Monthly Income

How a Financial Advisor Fits (and When)

At this stage, most doctors don’t actually need a traditional financial advisor.

What you need first is clarity.

Clarity on whether you’re even asking the right questions yet.

Clarity on which decisions matter now versus later.

And clarity on how all of this fits into your life, not just a spreadsheet.

That’s why we don’t start with products, portfolios, or projections.

We start with education.

Before you hire anyone, sign anything, or move large sums of money, it helps to step back and understand the full picture of your financial life — income, debt, investing, taxes, time, and burnout risk — together.

That’s the gap we built Medicine and Money Show to fill.

If you want a structured walkthrough, not advice shouted at you from every angle, many physicians start with our book:

Freedom for Doctors — a physician-written guide to financial and personal liberation.

It’s designed to help you see:

- Why high income alone doesn’t create freedom

- How doctors get stuck working harder even as net worth grows

- What real financial independence looks like for physicians

- How to build wealth without sacrificing your health, family, or sanity

It’s not a tactics manual.

It’s a mindset and framework reset — one that helps you make better decisions long before you ever “optimize” anything.

If you’d rather test-drive the framework first, we also offer a free physician financial flight plan built around our LIFTOFFNOW model.

This short ebook walks you through:

- Where you are right now

- What phase of the financial journey you’re actually in

- What deserves attention next — and what can wait

No selling.

No commitment.

Just a way to organize the noise into something actionable.

And if after reading, you’re still unsure how your situation fits into all this, you can book a free 10–15 minute clarity call.

Not to pitch.

Not to manage your money.

Just to help you think clearly about your next step — or confirm you’re already on the right path.

For doctors who don’t even have time to read right now, the audio version of this guide is also available.

Many listeners simply hit play during commutes or between shifts and come back later when they’re ready to act.

However you choose to engage, the goal is the same:

Give you confidence before complexity.

Understanding before action.

And a path forward that doesn’t rely on pressure or urgency.

You don’t need to figure this out alone.

But you do deserve guidance that respects your intelligence, your time, and your profession.

FAQ

The next step after maxing out a 401(k) is usually contributing to an IRA (Roth or Traditional) or investing through a taxable brokerage account. Which comes first depends on your income level, tax situation, and how much flexibility you need with your money.

Once you hit the 401(k) contribution limit, additional employee contributions are no longer allowed for that year. At that point, further investing must happen outside the 401(k), such as through IRAs, brokerage accounts, or other retirement vehicles.

Yes, for most doctors, maxing out a 401(k) is a strong foundation because of tax deferral and employer match benefits. However, it should not come at the expense of an emergency fund, high-interest debt payoff, or overall financial balance.

If you contribute more than the annual limit, the excess amount must be corrected or it may be taxed twice. Most plans allow you to fix this by withdrawing the excess and any associated earnings before the tax deadline.

Maxing out a 401(k) alone is often not enough for doctors, especially those starting late or planning higher retirement spending. Additional savings through IRAs, brokerage accounts, and other investments are usually required.

High-interest debt should usually be prioritized before aggressive investing beyond a 401(k). Lower-interest debt may be balanced alongside investing, depending on cash flow and risk tolerance.

A taxable brokerage account offers flexibility, no contribution limits, and access to funds at any time. The downside is less favorable tax treatment compared to retirement accounts, since dividends and capital gains are taxable.

The best options typically include IRAs, taxable brokerage accounts, HSAs, and sometimes real estate or employer-specific plans. The right mix depends on tax goals, time horizon, and how soon you may need access to the money.

Yes, alternatives include Roth IRAs, Traditional IRAs, HSAs, 457(b) plans, SEP IRAs, and cash balance plans. Each serves a different purpose and fits different stages of a physician’s financial journey.