Doctors are not automatically rich because high income does not equal high net worth or financial freedom.

Some physicians build real wealth over time, but many remain financially stressed for decades due to student loans, lifestyle inflation, taxes, and delayed investing. The outcome depends less on salary and more on financial planning, savings behavior, and long-term decision making.

That distinction matters because most people judge doctors by income alone.

And income is only one variable in a much larger equation.

This article explains the difference between income, net worth, and financial freedom. It uses real data from doctor pay surveys, federal sources, and doctor-led finance platforms. More importantly, it shows how doctors can move from high earnings to real wealth.

Why “High Income” Doesn’t Automatically Mean Wealth

High income looks impressive on paper.

Wealth is what remains after decades of decisions.

Physicians earn some of the highest salaries in the United States, but they also face unique financial friction that other high-earning professionals never encounter. Long training pipelines, heavy debt loads, and delayed asset accumulation create a slow start that compounds over time.

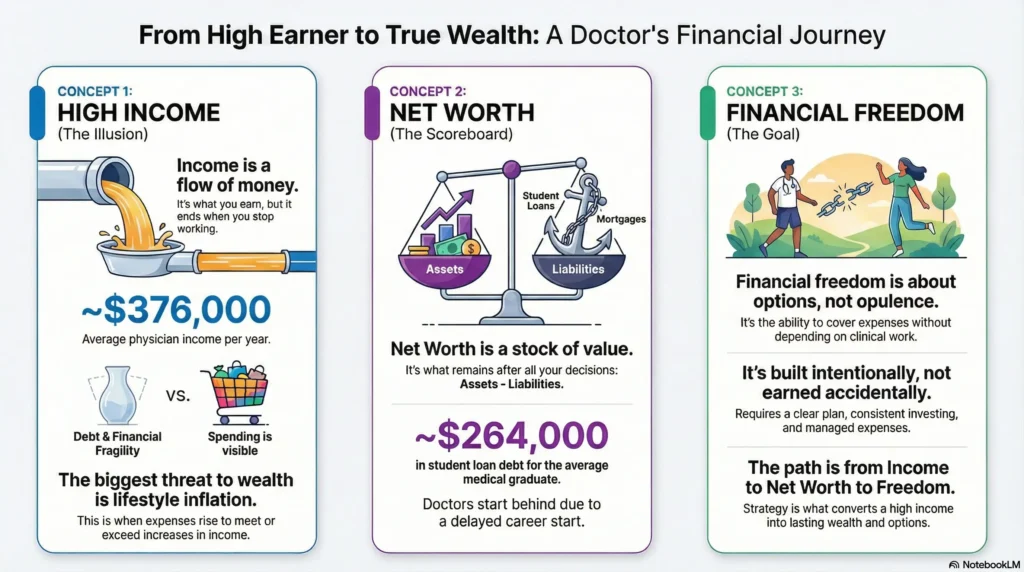

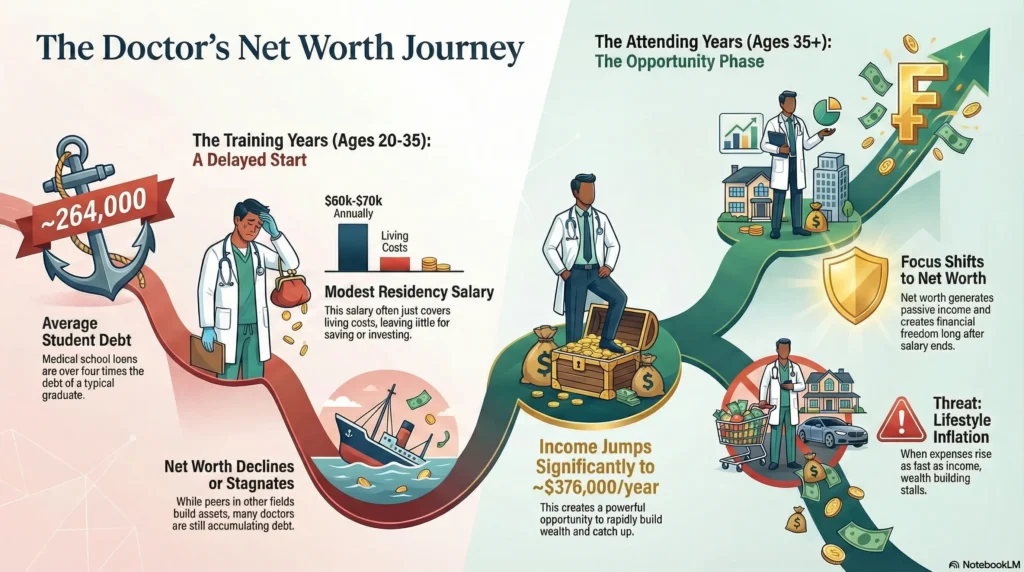

Medscape reports average physician income around $376,000 per year, with specialists earning significantly more

Yet income alone does not measure progress.

A doctor earning $400,000 who saves little and carries large liabilities may build less wealth than a lower-earning professional who starts earlier and invests consistently.

This is the first mental shift most physicians need to make.

Income varies a lot by medical specialty, practice setting, location, and whether a doctor works in private practice, hospital employment, or locum tenens roles. Some specialists earn multiples of what primary care physicians make, yet still struggle to convert that income into long-term wealth if spending and planning are misaligned.

Read: [Average Doctor Salary by Specialty (And Why Salary Alone Won’t Make You Wealthy)]

Income vs Net Worth: The Difference Most People Miss

Income is flow.

Net worth is stock.

Net worth = assets – liabilities

Assets include:

- Savings

- Stocks

- Retirement accounts like 401(k), 403(b), IRAs, HSAs

- Real estate

- Business equity

Liabilities include:

- Student loans

- Mortgages

- Credit card debt

- Practice loans

- Personal guarantees through LLCs

A physician can earn a high salary and still have a negative or stagnant net worth if liabilities grow as fast as income.

This misunderstanding causes many wrong ideas about money in medicine.

Read: [Doctor Net Worth vs Financial Freedom: Why They’re Not the Same Thing]

Net Worth by Age: Why Doctors Often Look Behind

Doctors often compare themselves to peers outside medicine and feel behind.

That comparison ignores timing.

Most physicians spend their 20s and early 30s in medical school, residency, and fellowship. During that time, net worth often declines instead of grows.

The average medical graduate carries about $264,000 in student loans, more than four times the debt of a typical college graduate

Meanwhile, residents earn modest salaries.

Most residents earn between $60,000 and $70,000 annually, which often barely covers living costs in high cost-of-living regions

So when physicians search for net worth by age, they’re often seeing benchmarks that don’t reflect their reality.

Read: [Net Worth by Age for Doctors in Training vs Attending Physicians]

This delay is normal.

Staying delayed forever is not.

The “Rich Doctor” Myth and Where It Comes From

The myth comes from visibility.

Doctors drive nice cars.

Doctors live in good neighborhoods.

Doctors earn high salaries.

What’s invisible:

- Debt balances

- Monthly expenses

- Stress tied to income dependence

A physician may appear wealthy while remaining financially fragile.

The myth persists because spending is visible.

Net worth is not.

Student Loans, Late Starts, and the Cost of Becoming a Doctor

The cost of medical education reshapes a physician’s entire financial trajectory.

Medical school requires:

- Four years of tuition

- Lost earning years

- Heavy borrowing

Residency and fellowship add:

- Opportunity cost

- Limited savings

- Delayed investing

By the time many physicians reach attending status, they are in their early to mid-30s with significant liabilities and little accumulated assets.

This delay matters because compound interest rewards time more than income.

Every year spent servicing debt instead of building assets pushes financial freedom further out.

This is not a personal failure.

It is a structural reality of the health care industry.

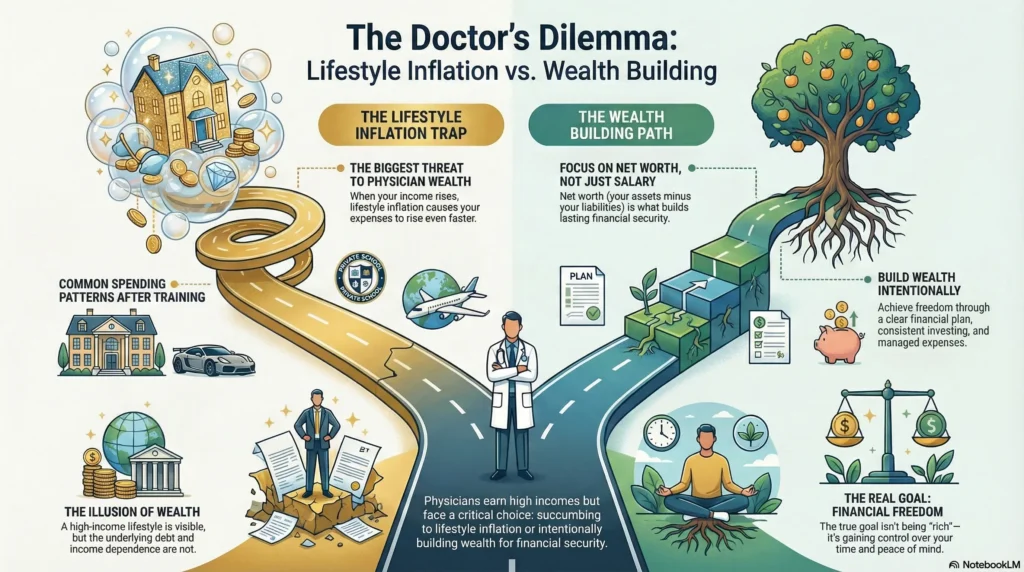

Lifestyle Inflation: How High Earners Stay Financially Stuck

The biggest threat to physician wealth is not debt.

It is lifestyle inflation.

When income rises, expenses often rise faster.

Common patterns include:

- Larger homes immediately after training

- New cars financed, not paid

- Private school tuition

- Expensive travel framed as “deserved”

- Costly convenience services

One physician describes going from $3,500/month take-home as a resident to $16,500/month as an attending, only to fill the increase with higher fixed expenses

That behaviour locks doctors into high monthly burn rates that require continued clinical revenue.

High income becomes a trap instead of a tool.

Why Net Worth Matters More Than Salary for Doctors

Salary ends when you stop working.

Net worth keeps working.

Net worth matters because it:

- Generates passive income

- Creates flexibility

- Reduces dependence on clinical revenue

- Protects against burnout, illness, or policy shifts

Assets like stocks, real estate, and diversified investments produce returns even when you step back.

This is especially important in a profession with:

- High burnout rates

- Physical demands

- Regulatory risk

- Reimbursement pressure

Net worth is not about status.

It is about options.

Financial Freedom vs Being “Rich”: What Doctors Actually Want

Most physicians do not want yachts.

They want:

- Control over their time

- The ability to reduce hours

- Freedom to change practice settings

- Security for family

- Peace of mind

That is financial freedom.

Financial freedom comes from:

- A clear financial plan

- Intentional savings

- Long-term investing

- Tax-efficient strategies

- Managed expenses

Not from salary alone.

Wealth is built quietly.

Freedom is built intentionally.

The First Step From Income to Financial Freedom

The first step is clarity.

Doctors must:

- Understand where money actually goes

- Track assets and liabilities

- Build a savings habit

- Invest consistently

- Avoid lifestyle inflation early

Many doctors work with a fiduciary financial advisor. This advisor understands challenges specific to doctors, practice ownership, taxes, and retirement planning.

Others educate themselves through trusted sources like Jim Dahle, The White Coat Investor, and long-form financial literacy content.

Read: [Is Being a Doctor Worth It Financially? A Long-Term Reality Check]

Income creates opportunity.

Only strategy converts it into wealth.

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

- 🎧 Listen to the audio version of this guide while commuting or between shifts

- 📘 Read our book on Amazon for a structured walkthrough of financial freedom for doctors

- 📥 Download the free LIFTOFFNOW ebook to understand the full framework

- 📞 Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Yes, a 401(k) is still worth it for doctors, but it should be treated as a tax tool, not a complete wealth strategy. Contribution limits, restricted access, and required minimum distributions mean it supports retirement savings but does not create early financial freedom on its own.

There is no single “best” investment for doctors because the right choice depends on income stability, debt level, risk tolerance, and time horizon. Most doctors do better with a mix of diversified stock investments, tax-advantaged retirement accounts, and long-term assets like real estate. This approach works better than chasing high-return opportunities.

Yes, many doctors struggle financially early and even mid-career despite high income. Student loans, delayed earnings, lifestyle inflation, and lack of financial planning often prevent income from translating into net worth.

Yes, being a doctor can be financially worth it over the long term, but only if income is converted into assets and not absorbed by expenses. Without intentional planning, high earnings alone do not guarantee wealth or financial freedom.

Most doctors accumulate retirement savings later than other professionals due to delayed earnings. Surveys show many physicians do not reach substantial retirement balances until their 40s or 50s, even with consistent 401(k) or 403(b) contributions.

Some doctors are wealthy, but many are not financially free. High income creates the appearance of wealth, while net worth and passive income determine real financial security.

Alternative investments are assets outside traditional stocks and bonds, such as real estate, private equity, private credit, hedge funds, commodities, and collectibles. These can diversify portfolios but often involve higher risk, lower liquidity, and greater complexity.

Most physicians are trained in medicine, not financial literacy. Time constraints, risk aversion after long training, and reliance on default retirement plans limit exposure to broader wealth-building strategies.

Doctors in the United States earn widely varying monthly incomes depending on specialty, location, and practice model. On average, physician income translates to roughly $20,000 to $30,000 per month before taxes, with specialists earning more.

Income translates into net worth only when excess earnings are saved and invested consistently. Without controlled expenses and asset growth, even high income fails to produce lasting wealth.

Key factors are student loan repayment plans, lifestyle inflation, investment choices, tax efficiency, practice ownership, cost of living in different places, and financial discipline.

Income is what you earn, net worth is what you own minus what you owe, and financial freedom is the ability to cover living expenses without relying on active work. Only net worth and cash-flowing assets create financial freedom.

Doctors often achieve financial freedom later than expected due to delayed earnings and high debt. Those who plan intentionally can still reach financial independence faster than average earners once income stabilizes.