Doctors usually have negative net worth during residency. Their net worth grows slowly in the early attending years. It only grows significantly in mid-career if they plan their finances well, control expenses, and invest consistently.

This pattern exists because U.S. doctors start earning their highest salaries late. They have large medical school debt, pay high taxes and living costs. They also often increase their spending right after residency.

If you are a doctor comparing yourself to others and wonder if you are behind, the truth is simpler and less comfortable. Most doctors delay building wealth not because they earn little, but because they start late and have poor financial habits.

The Financial Reality of Doctors in Training

Medical School Costs and Student Loan Debt

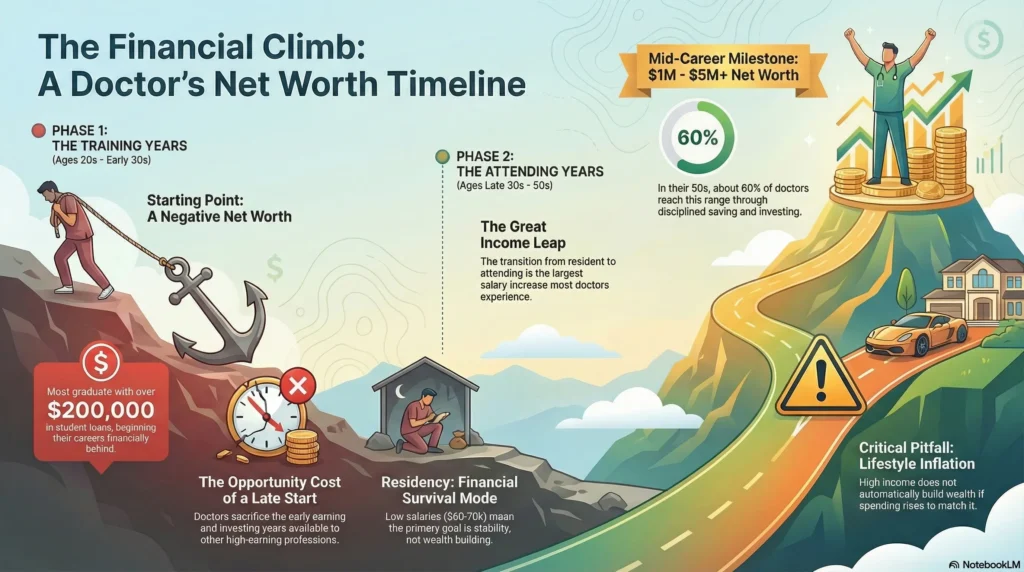

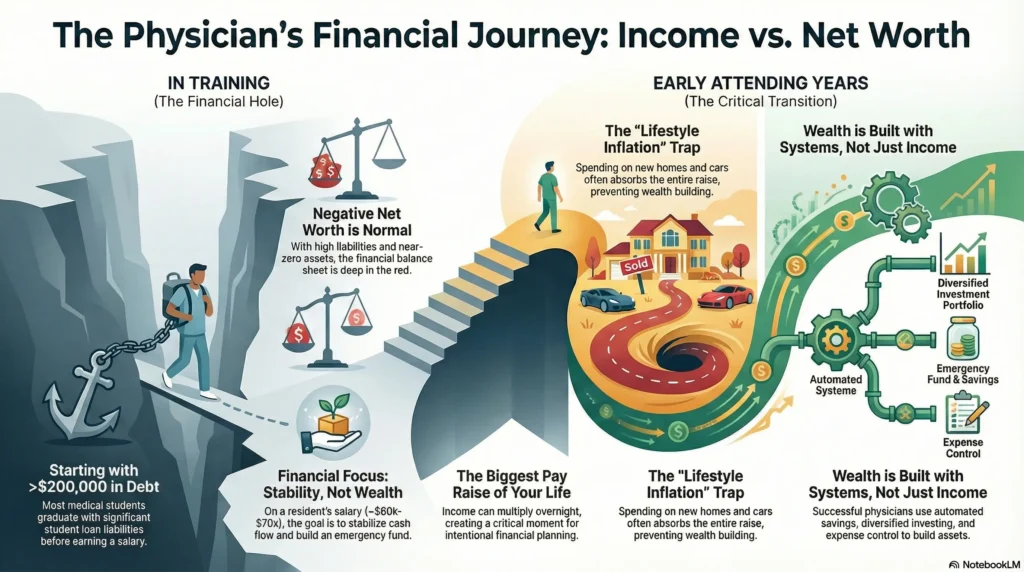

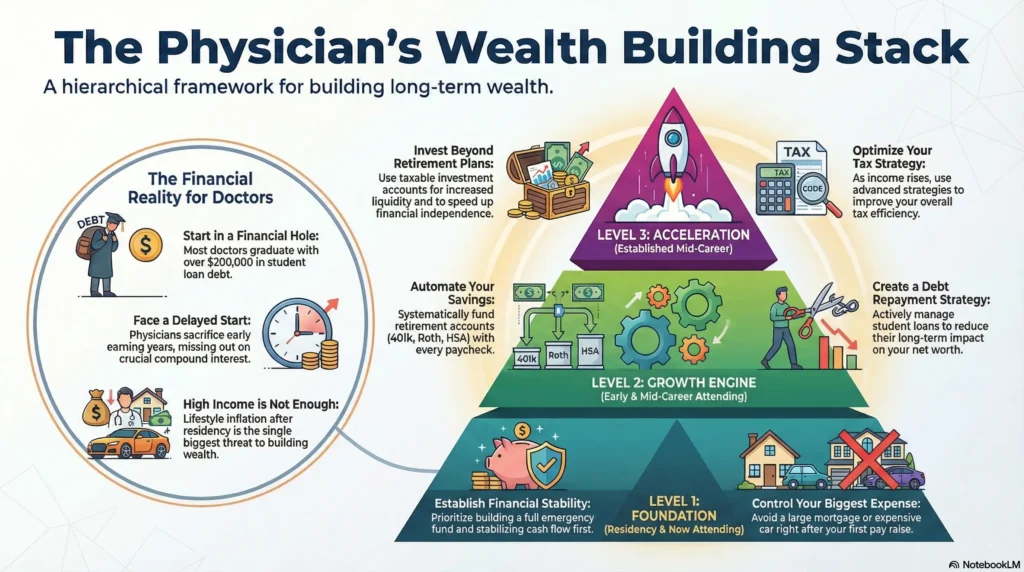

Most medical doctors begin their financial lives in a deep hole.

Experts point out that most medical students graduate with well over $200,000 in loans

According to data referenced by the Association of American Medical Colleges, the cost of medical school has risen faster than inflation for decades. Tuition, living costs, and education expenses during medical school add up. By the time residency starts, many doctors owe more than they earn in a year.

From a balance-sheet perspective:

net worth = assets − liabilities

During medical school and residency:

- assets are close to zero

- liabilities are dominated by medical school debt

- net worth is almost always negative

This is not a personal failure. It is a structural consequence of the U.S. medical education system.

Delayed Earnings and Opportunity Cost

Physicians earn later than nearly every other high-earning profession in the United States.

While peers may begin earning and saving in their early 20s, doctors spend those years preparing for the MCAT, completing medical school, and finishing residency. That delay creates an opportunity cost that shows up clearly in net worth by age data sets.

Money invested earlier benefits more from compound interest.

Doctors sacrifice those early compounding years in exchange for higher long-term earning potential.

This explains why:

- a physician assistant or nurse practitioner may show higher early net worth

- doctors often lag peers until their late 30s or 40s

- early comparisons feel discouraging

Why Net Worth Is Often Negative in Your 20s and Early 30s

At the residency stage:

- income is limited

- expenses remain high

- savings are minimal

- emergency funds are often underdeveloped

Residents earn roughly $60,000–$70,000 per year, which is barely enough to cover living costs in many metro areas, let alone build assets.

At this stage, financial planning should focus on:

- stabilizing cash flow

- building a basic emergency fund

- avoiding unnecessary lifestyle upgrades

- tracking expenses with simple tools, even an Excel spreadsheet

Wealth building comes later. Stability comes first.

The Transition From Resident to Attending Physician

Income Jump and Cash Flow Changes

The jump from residency to attending physician is the largest income increase most doctors will ever experience.

Annual salary can increase multiple times over, depending on specialty, clinical revenue, and geographic cost of living. Income categories expand rapidly, but so do taxes, especially when state’s income tax rates are high.

This is the moment when financial planning matters most.

Why Net Worth Does Not Immediately Catch Up

Despite the income jump, many new attendings see little improvement in net worth.

One major reason is lifestyle inflation.

Doctors transitioning to attending status often increase spending proportionally with income

A commonly cited example describes a physician moving from roughly $3,500 per month take-home during residency to over $16,000 per month as an attending, then immediately filling that gap with:

- a larger mortgage

- higher car payments

- increased loan payments

- rising fixed expenses

The raise gets spent, not saved.

This is why high income does not automatically lead to financial freedom.

Read: [Doctor Net Worth vs Financial Freedom: Why They’re Not the Same Thing]

Net Worth by Age Benchmarks for Doctors

Typical Net Worth in Your 30s as a Physician

According to Medscape survey data and physician finance data sets:

- early 30s physicians often have negative or low net worth

- late 30s physicians show wide variance based on savings habits

The median net worth in this age bracket is heavily skewed by:

- specialty choice

- student loan repayment strategy

- cost of living

- gender wage gaps

- career differences between primary care and specialists

Extreme outliers distort averages. Median values tell the real story.

Typical Net Worth in Your 40s and Early 50s as a Physician

This is where behavior compounds.

These differences reflect:

- long-term savings discipline

- automated savings plans

- investment consistency

- expense control

- tax-efficient use of 401ks, 403bs, Roths, HSAs, and taxable accounts

Income alone does not explain the gap. Habits do.

Common Mistakes That Slow Net Worth Growth After Training

Lifestyle Inflation After the First Big Paycheck

Lifestyle inflation increases fixed expenses faster than income.

High housing costs, frequent travel, and expensive vehicles raise the amount of income required just to break even. This delays retirement savings and the formation of a real nest egg.

Lifestyle inflation also reduces work-life balance by increasing financial pressure.

Over-Reliance on Retirement Accounts Alone

Retirement accounts are powerful but incomplete.

Tax-Deferred vehicles like 401ks and 403bs reduce current tax liability. Roths and backdoor Roth IRAs offer tax-free growth. HSAs provide triple tax advantages.

But relying only on retirement savings creates limitations:

- limited access before retirement

- reduced flexibility

- delayed financial independence

Doctors who want to retire early or optionally often use retirement accounts and taxable accounts together. This gives them easy access to money.

How Attending Physicians Can Accelerate Net Worth Growth

Aligning Career Stage With Investment Strategy

Net worth growth accelerates when strategy matches career stage.

Early attending years:

- complete an emergency fund

- automate retirement savings

- establish an automated savings plan

- fund a home down payment fund intentionally

Mid-career:

- diversify investments

- optimize tax strategies through LLCs if applicable

- increase savings rate as income rises

Late career:

- preserve assets

- manage withdrawal strategy

- plan retirement income

Financial planning is not static. It evolves.

Turning High Income Into Long-Term Financial Security

Doctors who build wealth do not rely on motivation.

They rely on systems:

- automated savings

- disciplined expense tracking

- diversified investments

- tax efficiency

They understand that:

- income is temporary

- assets create stability

- time rewards consistency

For a deeper framework that connects net worth to real freedom, read:

Read: [Doctor Net Worth vs Financial Freedom: Why They’re Not the Same Thing]

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

- 🎧 Listen to the audio version of this guide while commuting or between shifts

- 📘 Read our book on Amazon for a structured walkthrough of financial freedom for doctors

- 📥 Download the free LIFTOFFNOW ebook to understand the full framework

- 📞 Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Yes, a doctor can make $1 million a year, but it is rare and limited to specific specialties, practice models, and career stages.

Most doctors who reach this level are specialists like orthopedic surgeons, neurosurgeons, or cardiologists. Others own busy private practices, surgical centers, or related businesses. The majority of doctors earn far less.

Yes on average, but not always in early or mid-career, and not when adjusted for time, debt, and stress.

Doctors usually earn more money over their lifetime. But blue-collar workers who start working earlier, avoid student debt, and invest regularly can build similar or more wealth earlier.

Most doctors should aim to save 20–30% of gross income once they reach attending-level pay.

Early in residency, this may not be realistic. After training, saving rates matter more than income growth because savings drive net worth and financial independence.

Being a doctor offers high income potential, job security, and meaningful work, but comes with long training, debt, stress, and delayed wealth building.

Pros include stability and purpose. Cons include burnout risk, long hours, and late financial payoff compared to other careers.

Yes, being a doctor is objectively hard both intellectually and emotionally.

The work requires high responsibility and long hours. It involves constant decision-making and emotional strength. This is especially true in clinical settings with patient outcomes.

Yes, becoming a doctor is generally harder and longer than becoming an engineer.

Medical training requires more years of education, licensing exams, residency, and delayed earnings. Engineering usually allows people to earn income earlier. It also offers more career flexibility.

Medical school is very demanding academically. It is also emotionally and physically challenging.

Students face intense coursework, constant exams, long hours, and high pressure, often while accumulating significant medical school debt.

Physicians often have negative net worth in their 20s and early 30s, modest net worth in their late 30s, and higher net worth in their 40s and 50s if they save consistently.

Net worth varies widely by specialty, location, spending habits, and investment discipline. Averages are skewed by extreme outliers.

Estimates generally place this group in the low single digits, often under 5%, and usually tied to ownership, high-volume procedures, or multiple income streams.

Most doctors begin earning meaningful income in their early to mid-30s after completing residency or fellowship.

Before that, income during residency is relatively low compared to education level, which delays net worth growth despite high future earning potential.