Doctors graduate with six-figure debt because the average medical school education now costs well over $200,000, is primarily financed through federal student loans that accrue interest during training, and requires borrowing for both tuition and living expenses long before physician income begins.

While the exact amount varies by school type, location, and personal circumstances, most medical students rely on a layered mix of federal loans — and sometimes private student loans — that compound over time.

This article explains what average medical school debt really looks like, why it keeps rising, and why even high future income doesn’t make it harmless.

Understanding Medical School Debt

Medical school debt is the total borrowed amount medical students accumulate to pay for tuition, fees, and living expenses during medical education, primarily through federal loans and occasionally private lenders.

This matters now because:

- Tuition has risen faster than inflation

- Federal loan structures shift risk to borrowers

- Interest accrues before repayment starts

- Debt affects career flexibility, stress, and long-term wealth

This section is for medical students, med school applicants, and early medical school graduates who want clarity before the debt becomes invisible background noise.

Current Statistics and Trends

The numbers explain why six figures are common — not exceptional.

According to SoFi’s analysis of medical education borrowing

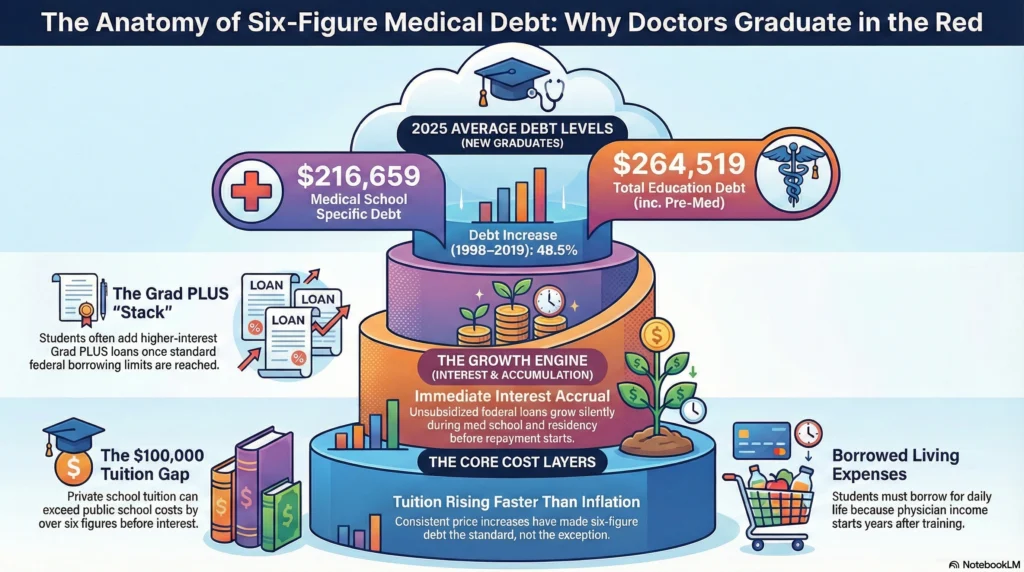

- The average medical school debt for graduates in 2024 was $234,597

- When including pre-med student debt, total education debt averages $264,519

- Medical school debt increased 48.5% between 1998 and 2019

EducationData.org confirms this trend, reporting that the average medical school debt balance in 2025 is approximately $216,659 among new indebted medical school graduates

What this means:

Medical school debt is not just high — it’s structurally designed to grow before repayment even begins.

Types of Loans for Medical Students

Most medical students don’t use a single loan.

They use a stack.

Medical students typically rely on:

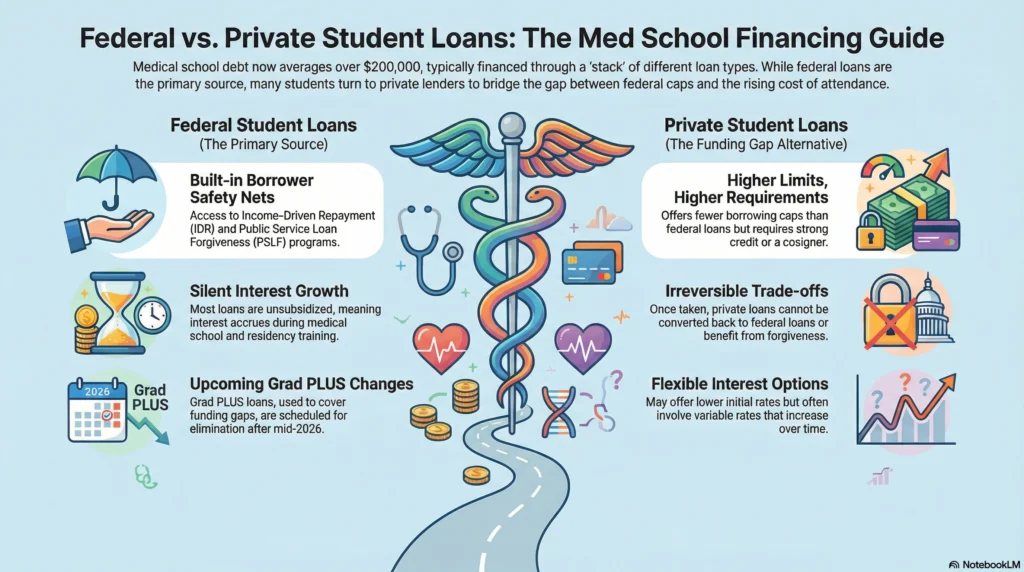

- Federal student loans (primary source)

- Grad PLUS loans (to cover gaps)

- Occasionally private student loans

EDvisors explains that medical students often need to combine federal and private loans to cover all expenses, especially as tuition and living expenses exceed federal borrowing caps

Tradeoff:

Federal loans offer protections. Private lenders offer flexibility — but remove safety nets.

Federal Loan Options

Federal loans form the backbone of medical student debt because they are accessible regardless of credit history and allow borrowing up to the cost of attendance.

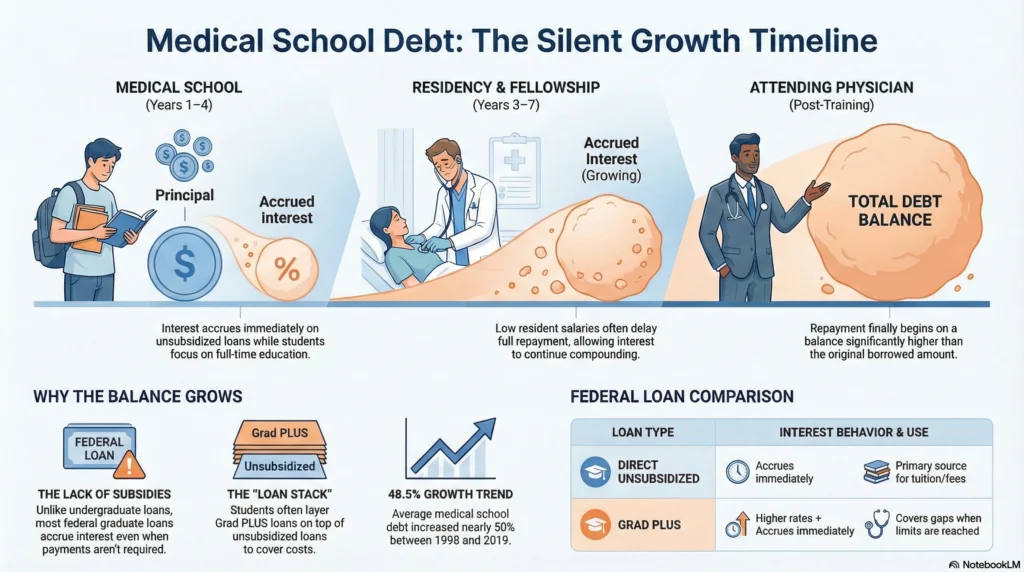

Subsidized vs. Unsubsidized Loans

Most medical students borrow unsubsidized loans, not subsidized ones.

Unsubsidized loans:

- Accrue interest immediately

- Grow during med school and residency

- Increase total student debt silently

A peer-reviewed study confirms that interest accrues on most federal graduate loans during medical school, even though monthly payments are not required

Why this matters:

Debt grows before you earn a physician salary.

Grad PLUS Loans

Grad PLUS loans exist to cover what unsubsidized loans cannot.

According to SoFi, Direct Unsubsidized Loans and Grad PLUS Loans have historically been the main federal options for medical students, though Grad PLUS loans are scheduled to be eliminated after mid-2026

Grad PLUS loans:

- Have higher interest rates

- Include origination fees

- Increase the debt-to-income ratio before residency

Best for: Students with no other funding options who plan forgiveness or structured repayment.

Private Loan Opportunities

Private student loans are sometimes used when federal student loans don’t fully cover tuition and living expenses. This usually happens at higher-cost medical schools or when borrowing limits are reached.

Before using private student loans, it’s critical to understand what you gain and what you permanently give up.

Pros and Cons of Private Loans

Pros of Private Loans | Cons of Private Loans |

|---|---|

May offer lower initial interest rates than federal loans | Interest rates are often variable and can increase over time |

Can cover full tuition and living expenses beyond federal limits | No access to income-driven repayment plans |

Fewer borrowing caps compared to federal loans | Not eligible for loan forgiveness or PSLF |

Faster approval in some cases | Require strong credit or a cosigner |

Useful as gap funding when federal loans are exhausted | Fewer hardship protections during residency |

May allow refinancing later if income increases | Lose federal borrower protections permanently |

Offered by multiple private lenders | Terms vary widely between lenders |

Why this matters:

Private loans are designed for repayment certainty, not for long medical training timelines. Once you take them, you cannot convert them back into federal loans.

Best used when:

- Federal student loans are fully maxed out

- You have a clear repayment plan

- You do not plan to use public service loan forgiveness

For most medical students, private loans should be a last resort, not a first choice.

Understanding Medical School Costs

Where you attend medical school has one of the largest impacts on how much student debt you graduate with, even before considering interest rates or repayment plans.

Cost Comparison: Public vs. Private Medical Schools

Cost Factor | Public Medical School (In-State) | Private Medical School |

|---|---|---|

Tuition | Significantly lower for residents | Consistently high regardless of residency |

Access to In-State Rates | ✅ Yes (often 30–50% lower) | ❌ No |

Average Borrowing Need | Lower overall student debt | Higher reliance on federal loans and Grad PLUS |

Living Expenses | Varies by location | Often higher in urban centers |

Total Cost of Attendance | More controllable | Less predictable, higher ceiling |

Impact on Debt-to-Income Ratio | ⬇️ Lower | ⬆️ Higher |

Long-Term Financial Flexibility | Greater | More constrained early career |

Why this matters now:

The difference between a public and private medical school can easily exceed $100,000 in additional borrowing — before interest accrues.

That gap:

- Increases monthly payments later

- Extends repayment timelines

- Pushes more graduates toward income-driven repayment or loan forgiveness

Who this matters most for:

Medical students deciding between:

- Multiple acceptances

- In-state vs out-of-state options

- Prestige vs long-term financial tradeoffs

Choosing a lower-cost medical school doesn’t limit career success — but it does reduce future financial pressure.

Repayment Strategies

Income-Driven Repayment Plans

Income-driven repayment ties monthly payments to discretionary income rather than loan balance.

Common features:

- Lower monthly payments during residency

- Extended repayment timelines

- Potential loan forgiveness

This is explained in detail here:

Read: [Federal Student Loan Repayment Options Explained for Doctors and Physicians]

Loan Refinancing

Student loan refinancing replaces federal loans with private loans.

It can:

- Lower interest rate

- Remove federal protections permanently

Before refinancing student loans, understand the tradeoffs:

Read: [Should Doctors Pay Off Student Loans Early or Invest Instead]

Service-Based Loan Forgiveness Programs

Public Service Loan Forgiveness (PSLF)

The public service loan forgiveness program forgives remaining federal student loans after:

- 120 qualifying monthly payments

- Full-time work at eligible nonprofit or government employers

Many hospitals qualify.

PSLF is covered in depth here:

Read: [Average Medical School Debt: What Doctors Really Owe and How Long It Takes to Pay Off]

Financial Planning and Budgeting

Building a Budget in Medical School

Budgeting during med school isn’t about comfort.

It’s about limiting future student debt.

Small choices around housing, lifestyle, and credit usage compound into long-term consequences — including financial stress.

Read: [How Student Loan Debt Affects Doctors’ Financial and Mental Well-Being]

Making Informed Decisions for Long-Term Success

Weighing Loan Options and Repayment Paths

Medical school graduates don’t fail financially because of debt alone.

They struggle when:

- They don’t understand loan structures

- They delay learning repayment plans

- They underestimate interest accumulation

Awareness changes outcomes.

Planning for a Debt-Free Future

Medical school debt is common.

Permanent financial pressure is not.

Doctors who understand their student loans early:

- Preserve flexibility

- Reduce stress

- Build real wealth later

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Doctors are in debt primarily because medical school is expensive and lasts four years, followed by low-paid residency years where loans continue accruing interest. Tuition, fees, exam costs, and living expenses compound the total balance.

Debt becomes risky when it exceeds a realistic post-residency repayment plan, often when total loans are significantly higher than expected early-career income. High debt is manageable for many physicians—but only with structured repayment strategies.

Yes, but it is rare and usually requires full scholarships, family support, military programs, or service-based commitments. Most medical students use loans because grants and scholarships rarely cover full medical school costs.

Yes, public in-state medical schools and certain accelerated or mission-based programs tend to have lower tuition. Cost differences can exceed $40,000–$60,000 per year between schools.

Medical students typically borrow federal Direct Unsubsidized Loans first, then Grad PLUS loans to cover remaining costs. Loans are disbursed each term and managed by a loan servicer during and after school.

You should borrow only what is needed for tuition and essential living expenses, not lifestyle upgrades. Every extra dollar borrowed accrues interest for years before repayment begins.

Loans are received after completing the FAFSA, accepting federal loan offers, and enrolling at an accredited medical school. Funds are sent directly to the school, with any excess refunded to you for living costs.

A student loan servicer is the company that manages your loans, processes payments, tracks balances, and administers repayment plans. Servicers do not set loan terms, but they control day-to-day account handling.

Your monthly payment depends on total debt, interest rate, and repayment plan, ranging from a few hundred dollars on income-driven plans during residency to several thousand dollars per month on standard repayment as an attending.