Managing investment risk as a doctor means making a clear plan that balances growth and safety. Your high income, limited time, and career pressures make unmanaged risk more dangerous for you than for most investors. The exact mix of protection and growth depends on career stage, debt load, and goals, but every physician needs a deliberate system that covers markets, inflation, liquidity, taxes, and career risk. Without that system, strong earnings alone do not guarantee financial security.

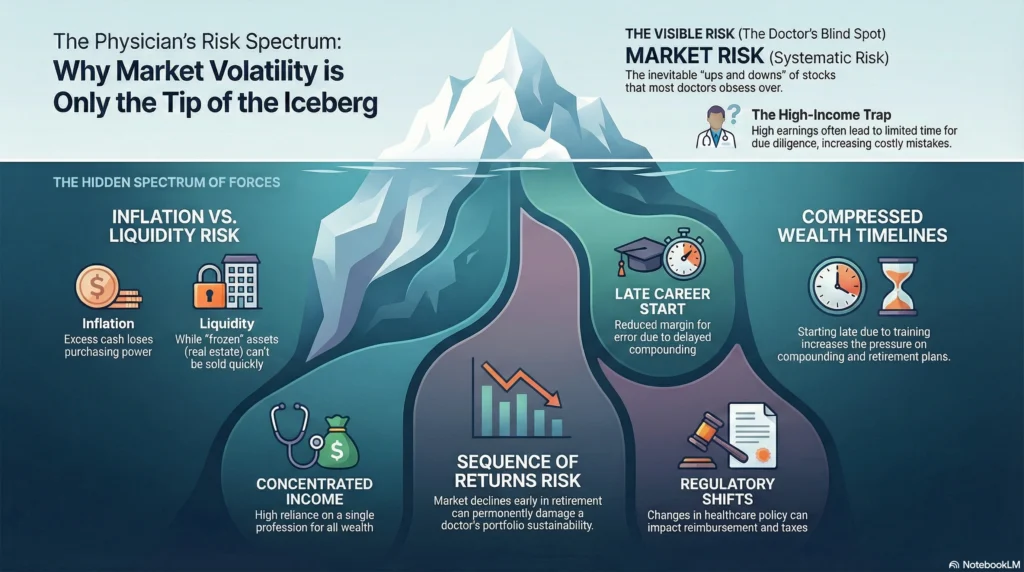

Doctors earn well, but your schedule leaves little room to deeply evaluate every opportunity. That combination creates blind spots. Doctors often have high income but limited time to question investments thoroughly, which raises the risk of costly mistakes. Risk management is not optional. It is the framework that protects your income, savings, and long-term wealth.

Read: [Lifestyle Inflation: The Silent Wealth Killer for Doctors]

Read: [How Doctors Can Gain Financial Clarity Without Obsessing Over Every Decision]

Understanding the Spectrum of Investment Risk for Physicians

Investment risk is the chance that your investment strategy does not produce the outcome your financial plan requires. It includes market losses, inflation damage, interest rate effects, liquidity limits, and policy changes. Physicians also face timing risk because many start serious investing later due to long training and debt from medical schools.

You often begin building wealth in your 30s while also managing student loans, mortgages, and family expenses. This compressed timeline increases pressure on retirement plans. Your income may be high, but delayed compounding reduces margin for error.

Wealth growth depends heavily on time in the market, and delaying investing reduces the power of compound interest. Small early contributions inside retirement accounts like 401k plans, 403b plans, Roth IRA, and Traditional IRA can grow dramatically over decades. Waiting even five years can change retirement outcomes by hundreds of thousands.

Physician-specific risk factors include:

• Heavy debt early career

• Irregular hours that limit financial literacy development

• Concentrated income from one profession

• Higher lifestyle expectations

• Exposure to healthcare regulatory shifts

Read: [Investment Types and Risk: How Doctors Should Think About Risk When Investing]

Key Investment Risks Every Doctor Must Understand

Market Risk (Systematic Risk): The Inevitable Ups and Downs of Stocks, ETFs, and Mutual Funds

Market risk means broad declines affect most investments regardless of quality. Stocks, mutual funds, index funds, and exchange-traded funds move with overall markets.

Why it matters now: Volatility is normal. Fear-driven selling locks in losses.

Who it is best for to understand deeply: Physicians with large equity exposure inside retirement accounts like 401k plans and Roth IRA.

Proof: Long-term investors who stay invested through downturns historically recover, while those who exit often miss rebounds. Diversified portfolios across asset classes reduce exposure to a single sector.

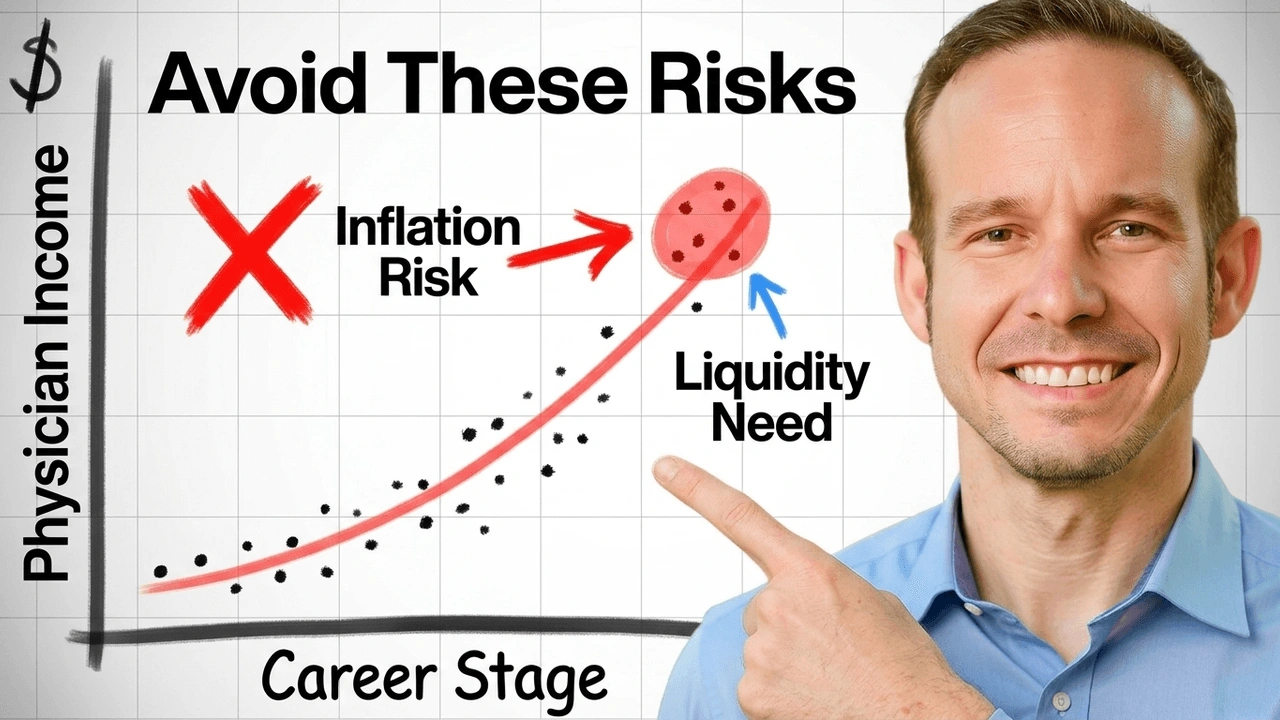

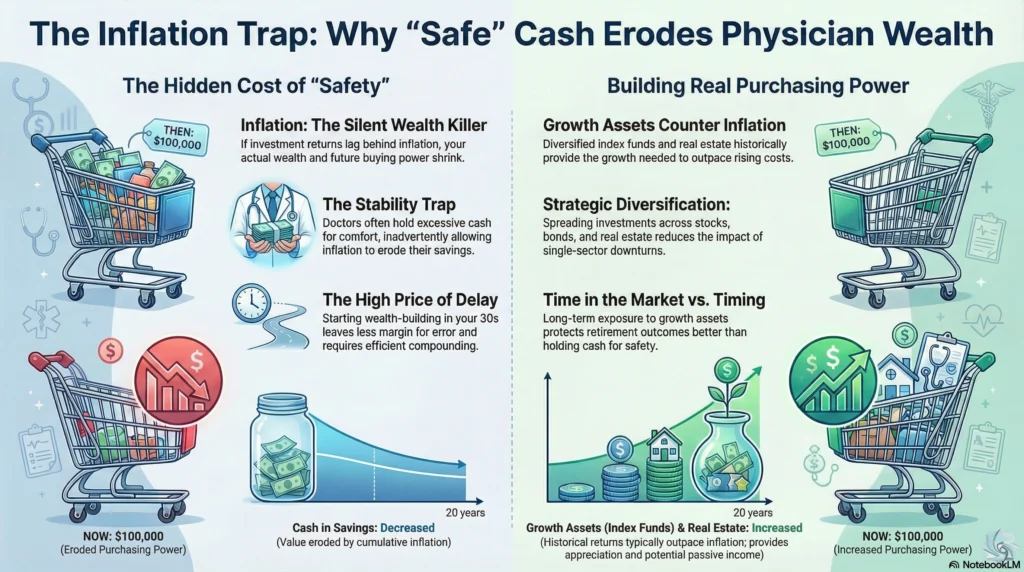

Inflation Risk: Protecting Your Future Purchasing Power and Retirement Savings

Inflation risk means your money buys less over time. If returns lag inflation, wealth shrinks in real terms.

Doctors often hold too much in a savings account for safety. While liquidity is useful, excess cash loses purchasing power.

Inflation risk is critical for retirement plans because expenses decades from now will be higher than today. Growth investments like index funds and real estate help offset this.

Interest Rate Risk: How Changing Rates Affect Bonds and Real Estate Investments

Interest rates influence bond prices and real estate financing. When interest rates rise, bond values typically fall. Higher rates also affect mortgages for real estate investing and rental properties.

Doctors often diversify into real estate for passive income. Understanding how interest rates affect cash flow and valuations helps avoid overleveraging.

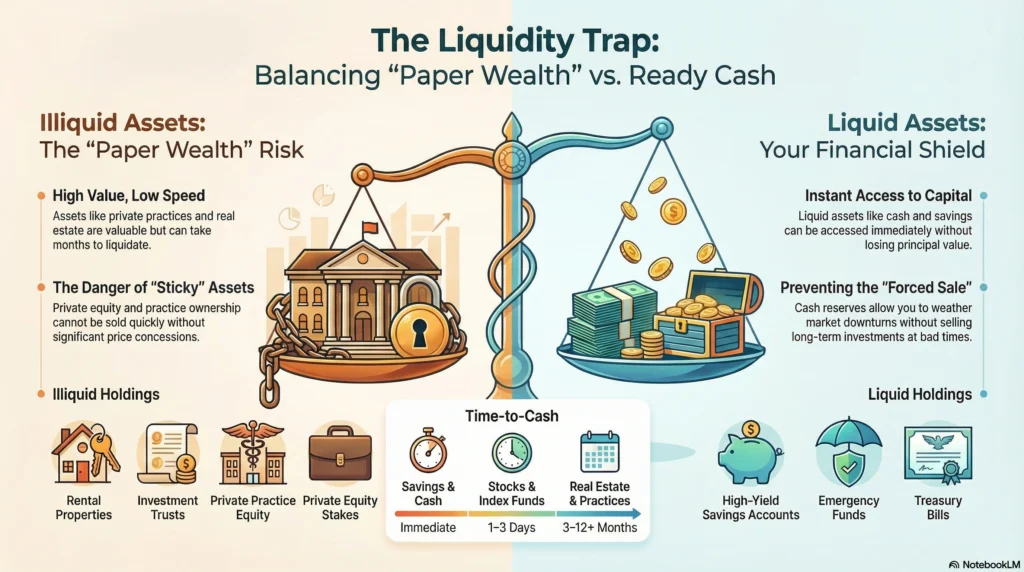

Liquidity Risk: Navigating Illiquid Assets like Real Estate, Private Equity, and Business Ownership

Liquidity risk appears when assets cannot be sold quickly without losses. Real estate, rental properties, private practice ownership, and investment trusts can be hard to liquidate.

Emergency funds in a savings account protect against selling illiquid assets at bad times. Liquidity risk planning is core risk management.

Sequence of Returns Risk: A Critical Concern for Doctors Nearing or In Retirement

Sequence risk occurs when market declines early in retirement damage portfolio sustainability.

Doctors near retirement need to change their asset mix. They should use different retirement accounts to lower withdrawal pressure during market downturns.

Credit Risk: Assessing the Default Potential of Bonds and Other Debt Instruments

Credit risk affects bonds, corporate debt, and some mutual funds. Higher yield often means higher default risk.

Balanced exposure to treasury bills and high-quality debt reduces credit risk inside retirement plans.

Political and Regulatory Risk: The Impact of Healthcare Policy and Tax Law Changes

Healthcare markets face regulatory shifts. Policy changes can affect reimbursement, taxes, and even investment environments.

Research discussing private equity ownership of hospitals highlights how pressure for short-term financial returns can introduce systemic risk in healthcare markets. This reminds physicians that business structures and investment environments carry broader risk beyond charts and returns.

Building a Robust Investment Strategy

Defining Your Risk Tolerance Level and Financial Goals: A Crucial First Step

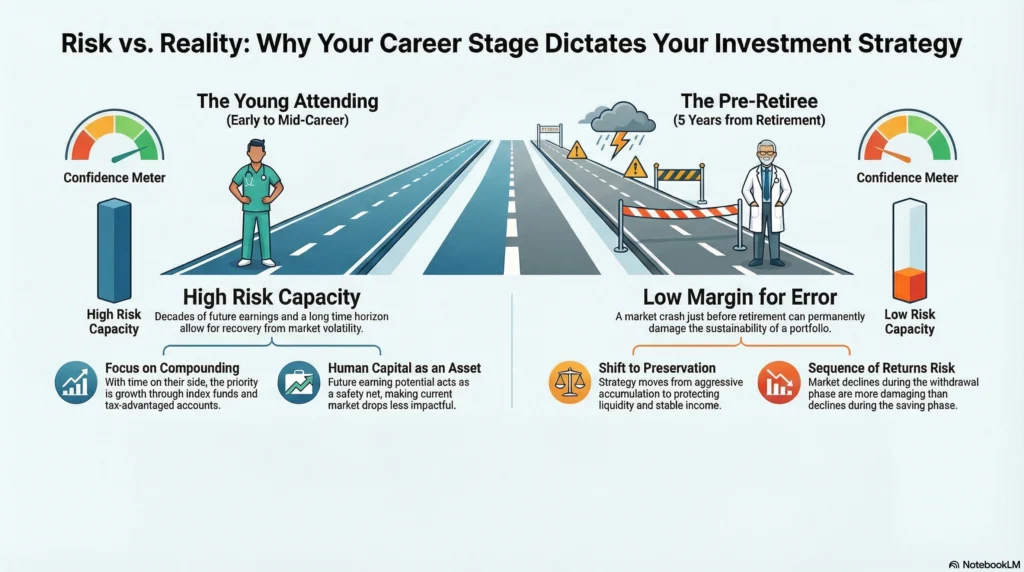

Your risk tolerance level combines emotional comfort and financial capacity. A surgeon with stable income and long horizon can accept more volatility than a doctor five years from retirement.

Your financial plan should link asset allocation to goals, not headlines.

The Power of Diversification and Asset Allocation: Your Primary Shields Against Volatility

Diversification spreads money across asset classes like stocks, bonds, and real estate.

Spreading investments across different asset classes reduces the impact of any one market downturn.

Doctors can use index funds, mutual funds, exchange-traded funds, and real estate investing to build diversified exposure. Asset allocation decisions drive long-term outcomes more than stock picking.

Leveraging Tax-Advantaged Accounts for Optimized Risk Management

Tax sheltering increases net returns and reduces pressure to take excessive risk.

Key vehicles include:

• 401k plans

• 403b plans

• solo 401k

• Roth IRA

• Traditional IRA

• defined benefit plans

These retirement accounts protect growth from annual taxes and support disciplined investing strategy.

Strategic Investment Choices for Controlled Risk

Choose low-cost index funds, diversified mutual funds, treasury bills for stability, and measured real estate exposure.

Doctors with private practice income may use solo 401k or defined benefit structures to increase tax-advantaged savings.

Read: [Active vs Passive Investing: What Works Best for Busy Doctors?]

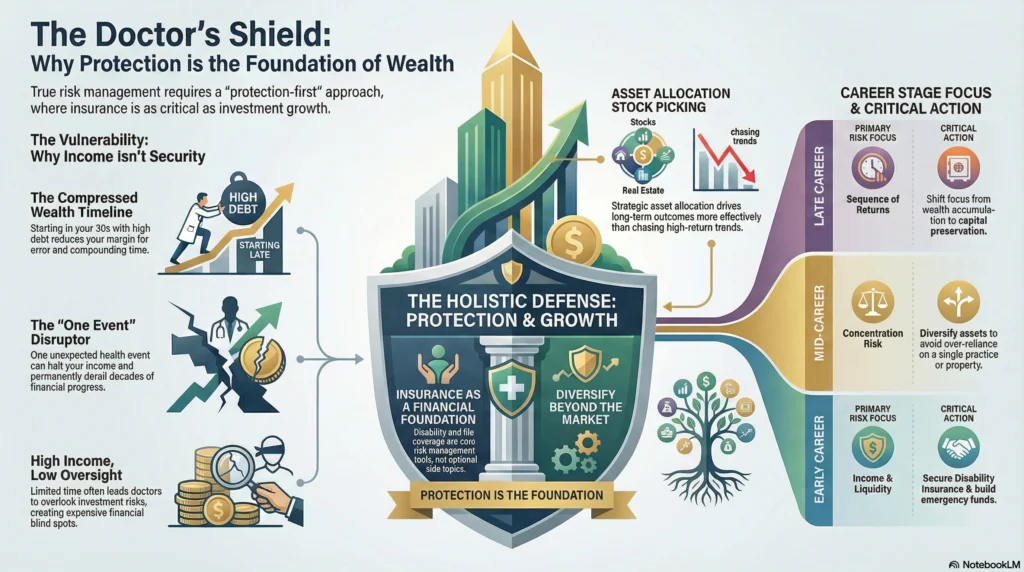

The Role of Comprehensive Insurance in Holistic Risk Management

Disability and life coverage protect earning power. Without it, one event can undo decades of financial planning.

Adapting Risk Management According to Your Career Stage

Investment risk is not static. Your income stability, time horizon, debt load, and life responsibilities change across your career. Your investment strategy and risk management approach must evolve with you.

What is appropriate risk as a resident can be dangerous near retirement. And what feels “safe” early on can quietly slow wealth building.

Here is how to think about risk at each stage.

Early Career (Residency/Fellowship): Build a Foundation While Controlling Downside Risk

At this stage, your biggest risks are not market risk. They are income risk, career risk, and liquidity risk.

You have:

• Lower income

• Student loans

• Limited savings

• High future earning potential

• Long investing time horizon

Your goal is not to chase returns. Your goal is to build financial stability and reduce fragile points in your life.

Risk management focus here:

1. Protect your income first

Your future earnings are your biggest asset. Disability insurance matters more than picking the right mutual funds.

2. Avoid lifestyle traps early

Keeping expenses low now reduces pressure later. It protects your ability to take career risks and build long-term financial security.

3. Start investing, even small amounts

Time in the market matters more than timing the market and early investing allows compound interest to work longer . Even small Roth IRA contributions build long-term resilience.

4. Keep your investment strategy simple

Use broad index funds or diversified mutual funds. You do not need complex real estate or private deals yet.

5. Build liquidity

A savings account and emergency fund reduce liquidity risk and prevent high-interest debt if life happens.

At this stage, the biggest mistake is overcomplicating investing before building a base.

Mid-Career (Attending Physician): Balance Growth With Risk Control

Now your situation changes.

You have:

• High income

• Growing assets

• Family responsibilities

• Mortgage or real estate exposure

• Larger retirement accounts

This is the phase where investment mistakes get expensive.

Physicians with high income and limited time often ask fewer questions before investing, which increases the chance of costly errors .

Risk management focus here:

1. Diversify across asset classes

Spreading investments across stocks, bonds, real estate, and other vehicles reduces the damage from any single downturn .

2. Manage concentration risk

Do not let:

• One property

• One private investment

• Your own private practice

• Your employer stock

dominate your net worth.

3. Watch real estate risk carefully

Real estate investing can build wealth, but rental properties bring leverage risk, liquidity risk, and property management complexity. Rising interest rates can stress cash flow.

4. Align asset allocation with goals, not hype

Your investing strategy should match:

• Retirement timeline

• Risk tolerance level

• Family needs

Not what colleagues or social media discuss.

5. Increase risk protection as wealth grows

Umbrella insurance, estate planning, and liability protection become part of risk management.

6. Keep retirement accounts optimized

Use 401k plans, 403b plans, Roth IRA, Traditional IRA, and defined benefit options where available. Tax structure reduces long-term portfolio risk.

Mid-career doctors often take hidden risks through overconfidence and complexity. Your job here is not to maximize risk. It is to take intentional risk.

Late Career / Pre-Retirement: Protect Against Timing Risk

Now risk shifts again.

Your biggest threat is no longer missing gains. It is losing money at the wrong time.

Sequence of returns risk becomes critical. A major downturn just before or early in retirement can permanently damage your retirement plans.

Risk management focus here:

1. Reduce market risk gradually

That does not mean going all cash. It means adjusting asset allocation to reduce volatility as you approach withdrawals.

2. Protect liquidity

You should not be forced to sell stocks or real estate at bad prices to fund living expenses.

3. Focus on withdrawal strategy

How you draw from retirement accounts matters as much as how you invested.

4. Reassess real estate exposure

Illiquid real estate may look good on paper but can create liquidity risk when you need predictable income.

5. Review healthcare and longevity risks

Healthcare costs, long life spans, and inflation risk must be built into your plan.

6. Shift mindset from accumulation to preservation

Your goal now is durability. Stable income. Lower downside. Financial security means having enough money to feel safe.

Many physicians stay too aggressive too long. Others become too conservative too early. The right answer depends on your timeline and cash flow needs.

Role of a Qualified Financial Advisor

Investment risk becomes more complex as your income, assets, and responsibilities grow. Most doctors were never trained to manage asset allocation, retirement accounts, tax structure, and real estate risk at this level.

A financial advisor’s role is not stock picking. It is helping you:

• Match investment strategy to career stage

• Control risk you do not see

• Avoid emotional decisions in volatile market conditions

• Structure retirement plans efficiently

• Bring clarity to complex choices

If this guide felt helpful but overwhelming, that’s okay. You do not need to master everything at once. Here are simple next steps.

🎧 Listen to the audio version of this guide while commuting or between shifts

📘 Read our book on Amazon for a structured walkthrough of financial independence for doctors

📥 Download the free LIFTOFFNOW ebook to understand the full framework

📞 Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn high income into lasting wealth with smarter risk management.

FAQ

Investment risk is the possibility that your investment returns will be lower than expected or that you could lose some or all of your money. It includes market risk, inflation risk, interest rate risk, liquidity risk, and credit risk, all of which affect how stable or volatile your portfolio may be.

The five major investment risks are market risk, inflation risk, interest rate risk, liquidity risk, and credit risk. Market risk comes from price changes in stocks and funds. Inflation risk lowers your buying power. Interest rate risk affects bonds and real estate. Liquidity risk limits how fast you can get your money. Credit risk happens when borrowers fail to pay back debt.

You reduce investment risk by spreading money across different types of assets. You should choose asset allocation that fits your risk level and timeline. Use retirement accounts that save on taxes. Keep enough cash available. Avoid putting too much money in one investment or property. Regular rebalancing and working with a financial advisor also help manage risk as your career and financial goals change.

The best investments for doctors are low-cost and spread out. They fit your time limits and long-term goals. Examples include index funds, mutual funds, exchange-traded funds, retirement accounts like 401k and Roth IRAs, and carefully chosen real estate. The right mix depends on career stage, income stability, and risk tolerance, not on chasing high-return trends.

Whether to pay off debt early or invest depends on interest rate, risk tolerance, and overall financial plan. High-interest debt should usually be paid off first, while low-interest mortgages may allow room for investing, especially if long-term market returns and retirement needs justify it. Liquidity and job stability also matter in this decision.

Investing in the stock market is important for doctors because salary alone rarely builds long-term wealth or financial independence. Equities, index funds, and diversified mutual funds provide growth that outpaces inflation over time, helping physicians turn high income into lasting net worth instead of relying only on earned income.