Doctors get clear about money by building a simple system. This system automates key money choices. It tracks only important numbers. Doctors get expert help when needed. They avoid trying to control every expense, market change, or money decision. This approach varies slightly based on career stage, income stability, and debt load, but the core idea stays the same: clarity comes from systems and priorities, not constant attention. You do not need to think about money all the time to be in control of it.

You live in a world of high responsibility. Patients depend on you. Your schedule is unpredictable. Your mental energy is already stretched. Yet your finances often feel like another full-time subject you are somehow supposed to master.

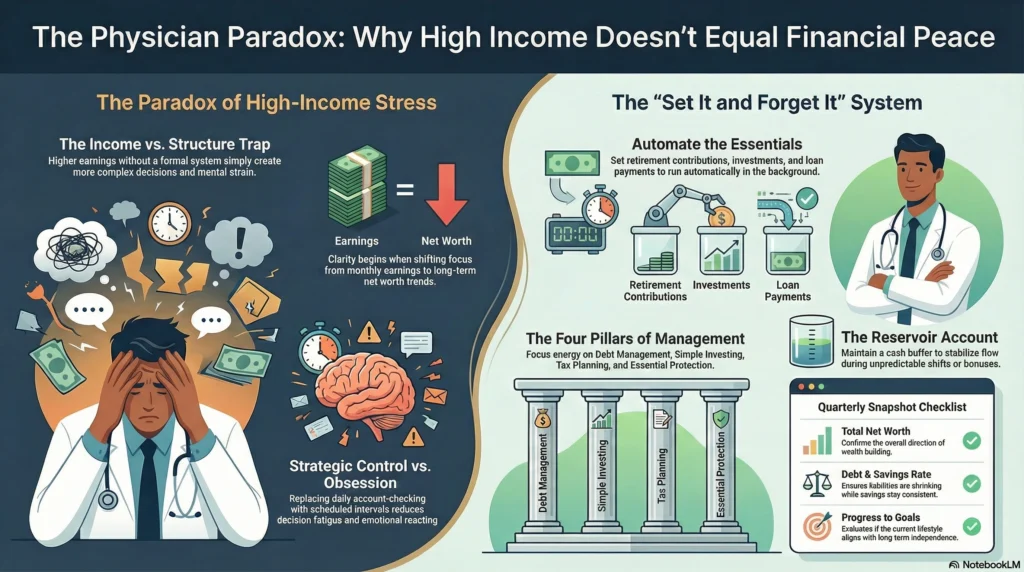

This creates the physician paradox. High income. High stakes. High stress. But low confidence about money.

And here is the hard truth. High income does not automatically produce financial clarity or financial independence; many affluent professionals focus too much on earnings instead of net worth, habits, and long-term perspective. You can earn more than most people and still feel behind.

The good news is that clarity is not about complexity. In fact, the more complex your life becomes, the more your financial life must simplify.

This guide shows you how to:

• Stop obsessing over small money choices

• Focus only on numbers that actually matter

• Build systems that run in the background

• Make confident financial decisions without constant mental strain

You do not need to become a finance expert. You need a framework that works for licensed healthcare professionals with demanding careers.

Redefining “Financial Clarity” for the Time-Strapped Physician

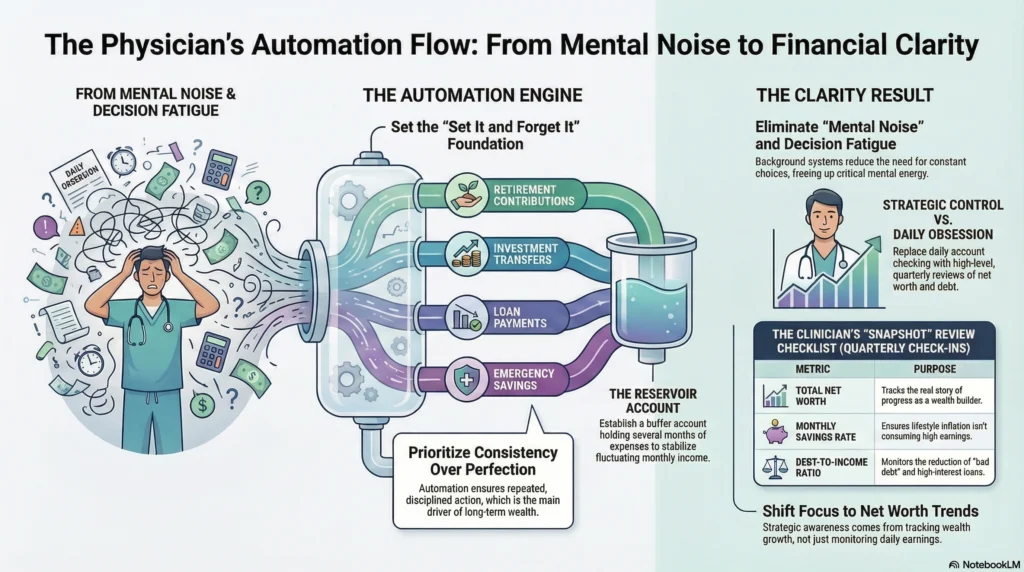

Most doctors misunderstand financial clarity. They think it means tracking everything. That belief creates stress, not control.

Beyond Spreadsheets: What True Clarity Really Means

Financial clarity is not about knowing your daily balance. It is about knowing your direction.

You have clarity when you can answer, without panic:

• Is my net worth growing year after year?

• Is my debt under control?

• Am I saving consistently?

• Are big risks covered?

• Is my lifestyle aligned with long-term financial independence?

Notice what is missing. No daily stock checking. No tracking every coffee. No comparing portfolios with colleagues.

Clarity is strategic awareness.

Many physicians focus on income and ignore net worth. That is a trap. Your net worth tells the real story of your progress as a wealth builder. Income can rise while net worth stays flat if lifestyle and bad debt grow at the same pace.

Doctors often reach attending physician status and suddenly earn well, but without structure, income turns into bigger houses, car upgrades, and rising fixed costs. Read: [Lifestyle Inflation: The Silent Wealth Killer for Doctors]

Clarity begins when you shift attention from earnings to net worth trends.

Ditching the “Obsession Mindset” for a “Strategic Control” Mindset

Obsession feels responsible. But it is usually fear.

You check accounts constantly. You worry about every expense. You delay investing because you want the perfect choice. That is not control. That is decision fatigue.

Strategic control works differently.

You design a plan. Then you review the plan at set intervals. Not daily. Do not make decisions based on emotions. Do things in an organized way.

Doctors often struggle here because training rewards perfection. But personal finance rewards consistency, not perfection. Even small disciplined steps early like budgeting, saving, and investing consistently make a big difference in long-term financial outcomes.

You do not need perfect timing. You need repeated action.

Establish Your Financial Overview with Minimal Effort

You cannot gain clarity without visibility. But visibility does not require complex tools.

The Snapshot Approach: Regular, High-Level Financial Check-ins

Think like a clinician. You do not monitor every vital sign every minute. You check at meaningful intervals.

Do the same with money.

Every three months, review only:

• Total net worth

• Total debt and bad debt specifically

• Monthly savings rate

• Cash flow after fixed expenses

• Progress toward key goals

This takes under an hour.

Doctors who skip this review drift. Doctors who check daily become anxious. Quarterly creates balance.

For many attending physician households, this review reveals where pressure actually sits. Often it is not income. It is cash flow management and rising fixed costs.

If your income is strong but you feel tight each month, lifestyle creep is likely the issue.

Automate the Essentials: Set It and Forget It Strategies

Automation is the most powerful clarity tool.

Set up automatic processes.

• Retirement contributions

• Investment transfers

• Loan payments

• Emergency savings

Once automated, decisions reduce. Fewer decisions mean less mental noise.

Many doctors delay automation because they want to “optimize first.” But delay costs time. And time is the main driver of wealth for wealth builders.

Doctors also benefit from creating a “reservoir account.” This is a buffer account that holds several months of expenses. It protects cash flow and reduces stress when income fluctuates, especially for practice owners or those with variable bonuses. A reservoir account stabilizes cash flow management and prevents small disruptions from becoming crises.

Strategic Simplification: Core Areas for Physician Financial Management

You do not need to master everything. Focus on four pillars.

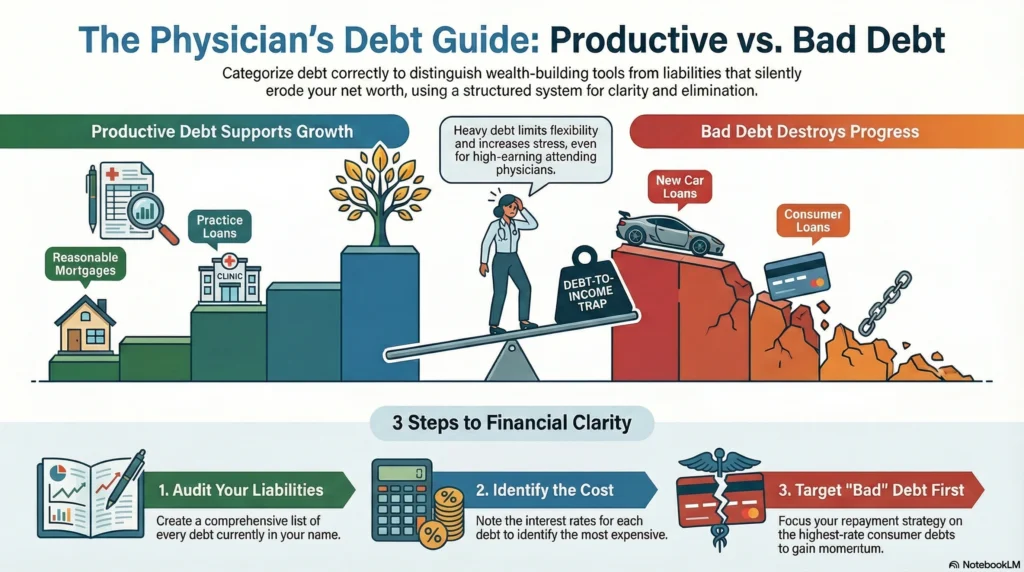

Debt Management: Smart Strategies to Reduce Overwhelm

Debt is one of the biggest clarity killers.

Start by labeling debt honestly:

• Productive debt: reasonable mortgage, practice loans

• Bad debt: high interest consumer loans, unnecessary upgrades

Bad debt erodes net worth silently.

Doctors often carry large student loans from medical school. Combine that with new car loans and aggressive housing choices, and the debt-to-income ratio becomes heavy.

High debt-to-income ratio limits flexibility and increases stress, even for high earners.

Clarity comes from a visible plan:

- List all debts

- Note interest rates

- Target highest-rate bad debt first

Consider student loan refinancing when appropriate, but only after reviewing protections you may lose.

For younger physicians and medical student graduates, this stage sets the tone for decades.

Investment Strategy: Building Wealth Without Becoming a Day Trader

You do not need to monitor markets daily.

A simple structure works:

• Core diversified investments

• Regular automated contributions

• Annual rebalancing

Your job is patient care, not trading.

Doctors who try to “outsmart” markets often create stress and poor outcomes. Instead, use simple investment tools and systems.

If you want a deeper understanding of how risk fits into your life, Read: [Investment Types and Risk: How Doctors Should Think About Risk When Investing] and also Read: [Investment and risk management]

The goal is progress, not excitement.

Tax Planning: Proactive Steps for Peace of Mind

Taxes create anxiety when ignored.

Annual tax planning reduces that anxiety.

Doctors, especially practice owners and healthcare providers with complex income streams, benefit from structured tax planning. Planning includes:

• Maximizing retirement accounts

• Reviewing deductions

• Timing major expenses

When taxes are planned, surprises shrink. And clarity grows.

Protecting Your Future: Essential Insurance & Estate Planning

You cannot have clarity if one event can collapse your plan.

At minimum:

• Disability insurance

• Basic life coverage

• Simple estate documents

For an attending physician, income protection is critical. Your earning ability is your largest asset early on.

Protection changes uncertainty into financial security.

Read: [Active vs Passive Investing: What Works Best for Busy Doctors?]

The Power of Delegation: Leveraging Expertise to Minimize Your Burden

You do not do surgery on yourself. Do not do everything financially alone either.

When and How to Engage a Financial Advisor

Doctors should consider professional help when:

• Income becomes complex

• Time becomes limited

• Decisions feel overwhelming

A good advisor reduces mental load. They help filter choices and keep you aligned with long-term wealth-building strategies.

Specialized Financial Services for Healthcare Providers

Doctors have unique patterns:

• Delayed earning start

• High education debt

• Irregular hours

A specialist understands physician mortgages, contract structures, and career paths.

Building Your Financial Dream Team: Accountants, Lawyers, and More

Clarity improves when experts coordinate.

Your team may include:

• Financial advisor

• Tax professional

• Legal advisor

For practice owners, including those with a dental practice or larger medical practice, this coordination becomes even more important.

Cultivating a “Clear-Headed” Financial Mindset and Habits

Systems matter. Mindset sustains them.

Embrace Imperfection: Progress, Not Perfection, is the Goal

You will make imperfect financial decisions. That is normal.

Doctors are trained for precision. Money rewards consistency.

Wealth builders win through repeated, disciplined action.

Connecting Financial Security to Holistic Well-being

Financial stress affects sleep, relationships, and work satisfaction.

Clarity reduces background stress. You stop carrying money anxiety into every shift.

Regular, Intentional Review Habits

Keep habits simple:

1. Quarterly snapshot

2. Annual planning session

3. Major life event review

No daily obsession. Just structured awareness.

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Doctors can make finances easier by automating savings and investments. They track only a few key numbers like net worth and cash flow. They use a quarterly review system instead of checking daily. They also let experts handle complex areas like tax planning and investing. Simplicity comes from systems, not constant attention.

Doctors feel more confident with money when they make a simple plan. They pay off high-interest debt and automate investing. They build an emergency fund. They check their progress regularly instead of reacting emotionally to every decision. Confidence comes from consistent action, not perfect knowledge.

You stop obsessing by replacing daily monitoring with scheduled reviews, automating major financial moves, defining clear long-term goals, and accepting that small mistakes will not derail a solid system. Obsession usually fades when you know a plan is running in the background.

To reduce emotional decisions, use written rules for investing and spending, wait 24 to 48 hours before big money moves, avoid frequent market checking, and rely on a structured plan or advisor for major choices. Systems and pre-made rules protect you when emotions run high.

Doctors who manage money well focus on growing net worth. They automate investing and control lifestyle spending. They use tax-advantaged accounts. They protect income with insurance. They work with financial experts who understand healthcare careers. Those without a system often rely on income alone and feel constant financial pressure.

High earners fall into poor habits because income creates a false sense of safety, social pressure increases spending, and financial decisions are made under stress or fatigue instead of strategy. Without a clear system, money follows emotion and lifestyle rather than long-term goals.