Passive investing is usually better for busy doctors. It reduces trading and lowers costs. It also improves tax efficiency. Passive investing avoids the time burden and performance challenges of trying to beat the market. Active investing can still play a small role if you have interest, skill, and protected time. The right mix depends on your schedule, risk tolerance, and investment goals, but for most physicians your medical career should stay your main source of active income while your money compounds in the background.

Physicians sit in a unique spot. High earning potential. Heavy clinical responsibility. Limited free time. Your financial decisions happen alongside patient care, call schedules, and the stress of running a medical practice. That is why the active versus passive debate is not theoretical for you. It directly affects your path to financial independence and long-term financial stability.

The list below breaks down how each approach works in the real world for doctors, where each fits, and how to combine them without turning investing into a second job.

Understanding Active Investing: Hands-On Wealth Building

What Active Investing Entails: Control, Research, and Management

Active management means you or a professional frequently make decisions about what to buy, sell, and hold. You may pick individual stocks, trade sectors, run concentrated real estate deals, or invest in private businesses. You are not simply tracking market indexes. You are trying to do better than them.

This approach gives control. You decide when to buy, when to sell, and which opportunities look promising. For physicians who enjoy analysis, this can feel intellectually engaging after long days in clinical work.

But control comes with responsibility. Active investing requires research, monitoring, and emotional discipline during market swings. That time cost is real. When your day already includes documentation, procedures, and patient communication, adding constant portfolio oversight can stretch your mental bandwidth.

Read: [How Doctors Can Gain Financial Clarity Without Obsessing Over Every Decision]

The Potential Upside: Beating the Market and Maximizing Capital Gains

The main attraction of active investing is the chance to outperform market indexes and generate higher capital gains. In theory, better decisions lead to better results.

In practice, consistent outperformance is hard. Decades of performance data show that most actively managed funds fail to beat their benchmarks over long periods, even with professional teams and research resources. Evidence on how difficult it is for active managers to consistently beat the market shows that stock picking is not just about intelligence. It is about time, process, and discipline.

That does not mean active investing never works. Some physicians do well in areas tied to their expertise, such as healthcare startups or medical real estate. The key is that their edge comes from knowledge, not guessing.

The Demands of Active Management: Time Commitment and Stress

Active investing is work. Monitoring positions. Reading reports. Tracking market conditions. Making buy and sell decisions. That creates cognitive load.

Busy doctors often start active investing with enthusiasm, then realize the stress of watching markets during volatile periods. A tough week in the hospital plus a falling portfolio is not a fun combination.

If you choose active management, you need a structured system, not reactions to headlines. Without that, emotions drive investment decisions, which usually hurts results.

Active Investment Strategies for Doctors (with Realistic Time Estimates)

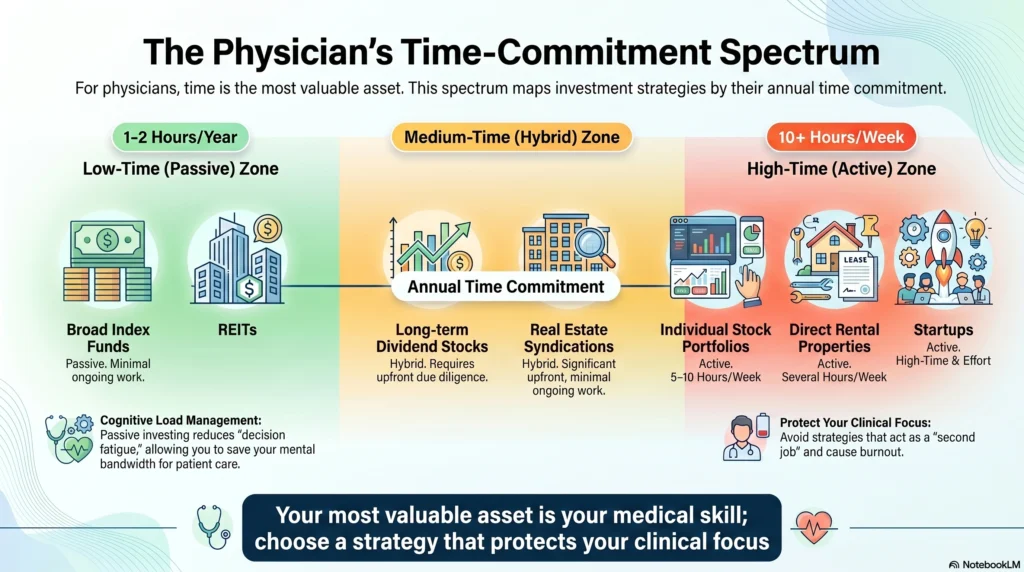

- Individual stock portfolios

Time: 5 to 10 hours per week

Best for doctors who enjoy markets deeply - Direct real estate investing with rental properties

Time: Several hours weekly unless fully outsourced

Tasks include property management, tenant issues, and financing

Many physicians pursue real estate for diversification and long-term appreciation, but it still requires oversight - Short-term rentals and vacation properties

Time: High upfront setup, ongoing coordination

Can generate strong cash flow but involve operational complexity - Private business or startup investments

Time: Heavy research and monitoring

High risk, potentially high reward

These strategies can build passive income later, but they often start as very active.

When Active Investing Aligns with a Doctor’s Goals

Active investing makes sense if you:

- Enjoy the process of analyzing investments

- Have time carved out consistently

- Accept higher risk and variability

- Want involvement beyond index funds

Even then, many physicians limit active investing to a smaller slice of their investment portfolio.

Understanding Passive Investing: Time-Efficient Wealth Growth

What Passive Investing Means: Delegating Management for Broad Market Exposure

Passive investing means you buy diversified funds that track market indexes and hold them long term. You are not trying to time markets. You accept market returns.

Passive strategies reduce trading, lower fees, and improve tax efficiency compared with frequent buying and selling. That cost advantage compounds over decades.

For busy physicians, this structure protects time and attention. Your investments grow while you focus on medicine.

The Advantages of Passivity: Minimizing Time, Diversification, and Lower Fees

Passive investing shines in three ways.

First, time efficiency. Passive approaches are well suited to busy professionals because they require minimal annual oversight. Automated contributions into index funds can run almost on autopilot.

Second, diversify your investments. A few broad funds can give exposure to thousands of companies, reducing the impact of any single failure.

Third, lower costs and tax benefits. Fewer trades mean fewer taxable events, which supports long-term financial stability.

Read: [Investment Types and Risk: How Doctors Should Think About Risk When Investing]

Also Read: [Investment and risk management]

Passive Investment Strategies for Doctors (with Minimal Time Estimates)

- Broad index funds tracking market indexes

Time: 1 to 2 hours per year - Dividend stocks held long term

Provide passive income through regular payouts - REITs and investment trusts for real estate exposure

Allow participation in real estate investing without direct property management - Passive real estate through syndications

Professional management teams handle operations

You focus on due diligence upfront

Physicians often use real estate and REITs as passive income sources for diversification. These still require initial research but become more passive after setup.

Why Passive Investing Is Often the Go-To for Busy Doctors

Your most valuable asset is your medical skill, not your ability to trade. Passive investing lets your money work while you stay focused on patient care and running your medical practice.

Passive investing also reduces the emotional roller coaster of constant decision making. You follow a plan, rebalance occasionally, and let long-term growth do the work.

Read: [Lifestyle Inflation: The Silent Wealth Killer for Doctors]

How to Choose the Right Path Based on Six Factors

Your choice depends on six factors.

- Available time beyond clinical hours

- Comfort with market swings

- Interest in financial research

- Investment goals such as retirement and financial independence

- Liquidity needs and cash flow demands

- Desire for control versus simplicity

The sweet spot for many physicians is a passive foundation with limited active exposure in areas like real estate or business ventures.

Hybrid Approaches for Optimal Wealth

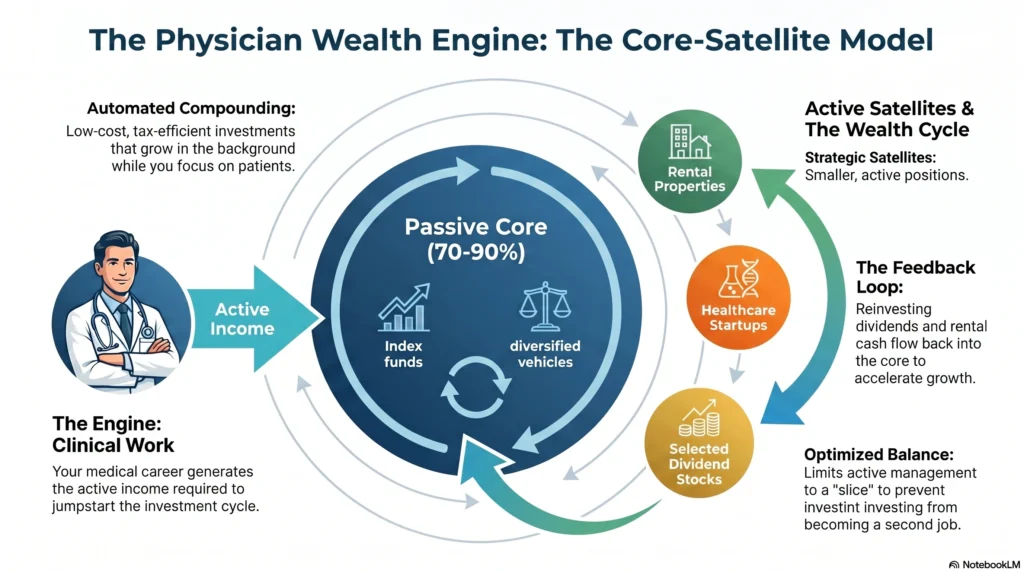

The Core-Satellite Portfolio

Most of your money sits in index funds and diversified vehicles. A smaller portion goes into active ideas such as rental properties or selected dividend stocks. This balances stability and opportunity.

Phased Investment Approach

Residency focuses on passive investing in retirement accounts. Early career adds some real estate investing. Later years may include more complex investment vehicles as knowledge and capital grow.

Delegated Active Management

You can participate in real estate investors groups or private deals where management teams handle operations. You remain involved at a higher level without daily property management tasks.

Actively Generating Income to Fuel Passive Investments

Extra clinical shifts or consulting can fund more passive real estate or dividend stocks. You convert active income into long-term passive income streams.

Critical Considerations for Doctors in Either Strategy

Instead of vague advice, here’s how key factors actually differ when you apply active vs passive investing as a physician.

Factor | Why It Matters for Doctors | Active Investing Impact | Passive Investing Impact |

|---|---|---|---|

Time Availability | Your primary job is patient care, not markets. Time away from charts, procedures, or family has a real cost. | Requires regular monitoring, research, and decision-making. Can feel like a second job. | Minimal time after setup. Periodic rebalancing only. Protects your focus for clinical work and life. |

Mental Bandwidth | Medicine already involves high-stakes decisions and cognitive load. | Adds stress during market volatility. Emotional decisions can creep in after long workdays. | Rules-based approach reduces decision fatigue and emotional trading. |

Tax Efficiency | High-income doctors lose a lot to taxes if portfolios are not structured well. | Frequent trades can trigger more taxable events and short-term capital gains. | Lower turnover improves tax efficiency and long-term compounding. |

Diversification | Your human capital is already concentrated in the medical field. | Risk of overconcentration if you bet heavily on a few stocks, deals, or properties. | Broad exposure across asset classes and market indexes reduces single-point failure risk. |

Cash Flow Needs | Early and mid-career doctors often juggle loans, lifestyle costs, and family needs. | Direct real estate or business investments may produce cash flow but with variability and management demands. | Dividend stocks, REITs, and index funds provide simpler, steadier long-term growth with some passive income. |

Skill and Interest | Not every doctor enjoys reading financial statements after clinic. | Works best if you genuinely enjoy investing and can commit time consistently. | Works even if you have low interest in markets. System does the heavy lifting. |

Career Flexibility | Goal is often financial independence, not just portfolio growth. | Potential for higher upside but also bigger mistakes that delay freedom. | Reliable wealth building that supports long-term financial stability and optionality. |

Bottom line. Active investing can increase returns in areas like real estate or private deals. Passive investing usually forms the stable backbone of your financial life. It supports your finances without taking much time.

Read: [The Biggest Financial Mistakes Doctors Make in Their 30s and 40s (And How to Avoid Them)]

Real-World Scenarios: Active vs. Passive Through a Doctor’s Career

Now let’s make this real. There are three hypothetical physicians. Three stages. Three different wealth approaches.

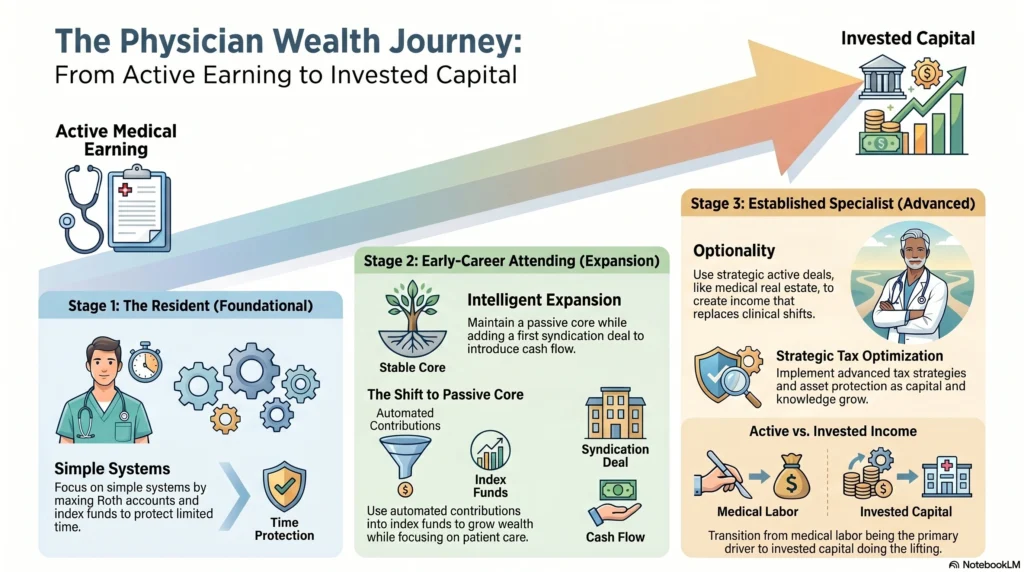

The Busy Resident: Maxing Passive Tax-Advantaged Accounts

Dr. Asha, PGY-2 Internal Medicine Resident

- Age: 29

- Income: Modest residency salary

- Debt: Heavy medical school loans

- Time: Almost none outside hospital

- Stress level: High

- Investment knowledge: Basic

Life Reality

Dr. Asha works long shifts, studies for boards, and barely sleeps. She does not have time for tenant calls, stock research, or analyzing private deals. Her biggest asset right now is future earning power, not current capital.

Best Wealth Strategy at This Stage

- Focus on passive investing only

- Contribute to Roth accounts and low-cost index funds

- Build basic emergency reserves

- Avoid active real estate or stock picking

Why This Works

- Protects limited time and mental energy

- Builds habits of automated investing

- Starts compounding early without complexity

This is where simple systems win. Her goal is to create a foundation, not to chase investment opportunities.

The Early-Career Attending: Passive Core, Exploring a First Turnkey Rental or Syndication Deal

Dr. Miguel, 3 Years Into Practice

- Age: 36

- Income: Strong jump after training

- Debt: Student loans partly paid down

- Family: Young children

- Time: Limited but more predictable

- Savings: Growing quickly

Life Reality

Dr. Miguel now earns well but faces lifestyle inflation pressure. Bigger house. Better car. Family expenses. This is the danger zone for wealth leakage.

Best Wealth Strategy at This Stage

- Majority in passive investing through index funds

- Max tax-advantaged retirement accounts

- Add one carefully chosen passive real estate or syndication deal

- Keep active investing limited and structured

Why This Works

- Passive core grows steadily

- A single real estate deal introduces cash flow and diversification

- Avoids turning into a full-time landlord

He gets exposure to real estate investing without letting property management take over his life. This stage is about expanding intelligently, not going all-in on active deals.

The Established Specialist: Diversified Blend, Strategic Active Deals, and Advanced Wealth Management

Dr. Sarah, 18 Years Into Career

- Age: 48

- Income: High, stable

- Net worth: Significant

- Debt: Mostly gone

- Time: More control over schedule

- Goals: Financial independence in 10 years

Life Reality

Dr. Sarah has capital, experience, and clearer goals. She is thinking about reducing clinical hours, not maximizing every dollar of income.

Best Wealth Strategy at This Stage

- Large passive base in diversified funds

- Multiple passive real estate positions for cash flow

- Select active deals where she has expertise or strong partners

- Strong focus on tax strategy and asset protection

Why This Works

- Passive investments support financial stability

- Real estate provides income that could replace clinical earnings

- Active investments are strategic, not random

At this stage, active investing becomes optional enhancement, not the foundation. Her portfolio works so she can choose how much to work.

Across all stages, one pattern holds.

Your medical career is your primary engine of wealth early on. Passive investing protects time and builds the base. Active investing, especially in real estate or businesses, can be layered in carefully once systems, capital, and clarity are in place.

That is how you invest without turning your life into another shift.

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Doctors should consider alternative investments for diversification beyond stocks and bonds and for potential additional income streams. Assets like real estate, private equity, or investment trusts can reduce reliance on traditional markets. They may provide cash flow, inflation protection, or long-term appreciation. These assets work well as part of a broader portfolio.

Doctors can evaluate alternative investments by checking the sponsor's track record. They should understand the business model and analyze fees. They need to check if incentives are aligned. They should also see how the investment fits their overall asset allocation and cash flow needs. Due diligence, independent verification, and sometimes input from a financial advisor are key.

No, alternative investments are not suitable for every doctor. They are generally better for physicians with stable finances, sufficient liquidity, and a long time horizon, because these investments can be complex and hard to exit quickly.

Time constraints limit how hands-on a doctor can be with alternative investments, especially real estate or private deals. Physicians with little free time often prefer passive structures. These include professionally managed funds or syndications. They avoid direct property management or active business involvement.

Yes, alternative investments can fit into a doctor’s overall financial plan when used as a complement, not a replacement, for core holdings. They typically serve as a smaller portion of a diversified strategy designed to balance growth, income, and risk across different asset classes.

Yes, many doctors invest in real estate as a way to diversify, build long-term wealth, and potentially generate passive income. Approaches range from direct rental properties to more passive options like REITs or real estate syndications, depending on time availability and interest.