Doctors make bad financial decisions in their 30s and 40s because their income rises faster than their financial education. This causes delayed investing, lifestyle inflation, poor debt choices, weak protection, and underused retirement tools. The exact mix varies by career stage, debt load from medical school, family needs, and practice type, but the pattern is consistent. Smart physicians can reverse this with structured financial planning, automation, and disciplined systems.

This guide is built for practicing doctors who already earn well but feel behind on wealth building. We studied common money mistakes doctors make. We learned about these mistakes from physician finance educators and behavior research. Then we turned these mistakes into practical fixes. You will see exactly what the mistake looks like, why it quietly damages your financial health, and how to fix it using repeatable processes. This is not theory. This is applied personal finance for the medical profession.

Mistake 1: Delaying Financial Planning and Investing

Many physicians delay financial planning because clinical training conditions you to focus on patients first and yourself last. But money has a timeline. When investing is postponed, you lose years of compound interest that you can never recover. Many physicians put off financial planning while juggling clinical demands, family, and long training schedules. That delay shrinks your future nest egg even if you later earn more.

Compound interest works best with time, not just income. A doctor who invests modestly from their early attending years often outperforms someone who waits and then invests large sums later. The earlier dollars grow the longest. Waiting compresses the growth window and forces you to save aggressively just to catch up.

Another issue is operating without a written plan. If you do not have clear goals, an investment plan, and retirement targets, you will make emotional and reactive investment decisions. Market dips feel scary. Market highs feel like pressure to chase trends. Structure reduces emotional mistakes and keeps your wealth management aligned with purpose.

Doctors trained in medical school are not trained in personal finance. Financial literacy must be learned separately. Without it, even smart professionals hesitate, overthink, or delay.

Read: [Investment Types and Risk: How Doctors Should Think About Risk When Investing]

Solution: Automate Your Savings and Invest Early

Automation removes willpower from the equation. Set automatic transfers to retirement plans, brokerage accounts, and Roth IRA contributions. Even small automatic deposits grow meaningfully.

Automation builds discipline without stress and protects your future self.

Mistake 2: Unchecked Lifestyle Inflation

After residency, income can jump dramatically. Without structure, spending rises just as fast. This is lifestyle inflation. Bigger homes, luxury upgrades, expensive cars, and higher recurring costs expand your baseline. Surge in income after residency often leads doctors to substantially increase spending without a structured savings plan. That expansion limits long term wealth building.

The “doctor house” often comes too early. Large mortgages tied to real estate purchases reduce flexibility and increase financial stress. Add car loans, private school tuition, and lifestyle subscriptions, and suddenly a high income produces little surplus.

High salary is not net worth. Wealth equals assets minus liabilities. A physician earning well but carrying big mortgages, car loans, and consumer debt may have low net worth growth. That disconnect creates the illusion of success without true financial independence progress.

Social pressure magnifies the issue. Colleagues upgrade. Neighbors upgrade. Social media amplifies visible wealth but hides debt. Without clear personal finance priorities, spending drifts upward.

Read: [Physician Net Worth by Age: What Doctors Should Expect at Every Stage]

Solution: Live Below Your Means

Set a savings rate target first. Build lifestyle around what remains. Tie spending decisions to future retirement planning goals, not income spikes. Living below your means is not deprivation. It is buying freedom later.

Mistake 3: Mismanaging Debt Beyond Student Loans

Doctors understand student loans, but other debt sneaks in. Physicians commonly struggle with managing debt beyond student loans, including credit card obligations, mortgages, and practice related borrowing. Consumer debt strains cash flow and blocks investing.

Large real estate commitments early in career amplify risk. Income may be high, but job changes, burnout, or family needs can reduce earnings unexpectedly. Big fixed payments remove flexibility.

Debt also affects psychology. Carrying high interest balances increases stress and reduces clarity around financial planning. Money feels scarce even when income is strong.

Doctors with medical school debt must coordinate repayment with investing. Aggressive payoff can make sense, but ignoring retirement planning entirely delays compound growth.

Read: [Student Loan Repayment Strategies for Doctors: A Clear Plan for High-Income Physicians]

Solution: Prioritize Debt Re-payment After Securing Emergency Savings

Build a cash cushion first. Then attack high interest debt. Keep housing costs reasonable relative to income. Borrow money based on a plan, not based on feelings.

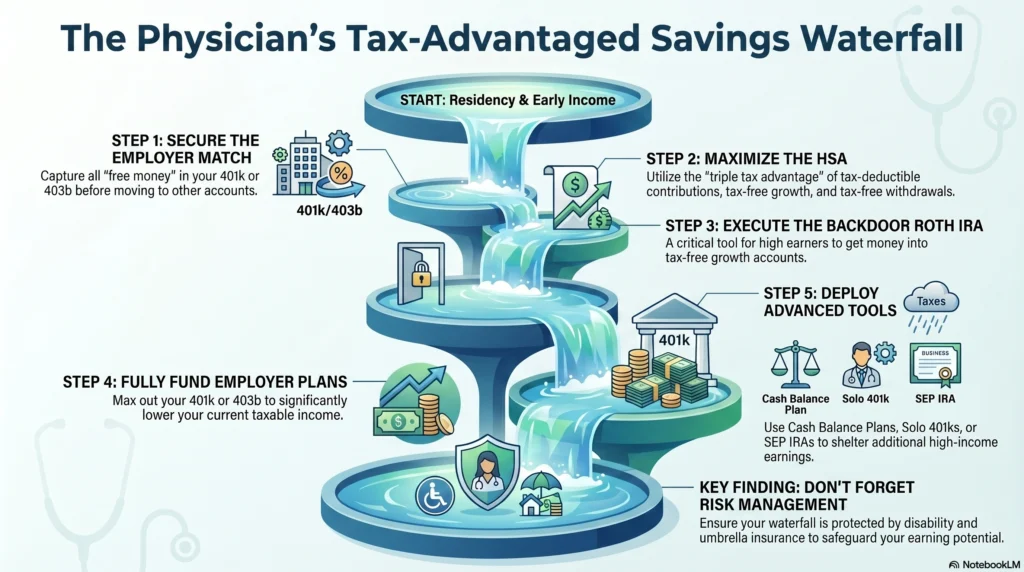

Mistake 4: Under-Optimizing Retirement and Tax-Advantaged Accounts

Physicians have access to powerful retirement plans but often do not maximize them. Physician finance experts note many doctors fail to fully understand or optimize retirement plans and tax advantaged accounts. Missing these tools slows retirement planning progress.

Key tools include employer 401(k) and 403(b), cash balance plans, Roth IRA strategies including backdoor Roth IRAs, HSAs, SEP IRA options, and Solo 401(k)s for independent earners. These accounts shelter growth from taxes, accelerating wealth.

Cash balance plans allow high income physicians to save large pre tax amounts. Solo 401(k)s provide flexibility for side income or practice owners. SEP IRA options support self employed income streams. Each tool has specific rules. Understanding them is critical.

Doctors focused only on salary may overlook these vehicles. Yet tax efficiency compounds over decades just like investment returns.

Read: [Where Doctors Should Invest After Maxing Out Their 401k and Roth IRA]

Solution: Maximize All Available Tax-Deferred and Tax-Free Growth Vehicles Systematically

Create a checklist. Max employer plans. Fund Roth IRA through backdoor Roth IRAs if income is high. Use HSAs as long term investment vehicles. Explore cash balance plans or Solo 401(k)s if eligible.

Mistake 5: Poor Investment Strategies and Decisions

Doctors often make investment decisions based on headlines, tips, or fear. Chasing hot stocks or crypto speculation adds risk without structure. Trying to time markets usually backfires.

A resilient portfolio needs asset allocation across stocks, bonds, and real estate. Broad diversification through index funds reduces single company risk. Low costs improve long term returns.

Behavioral mistakes are important. Emotional selling during downturns locks in losses. Overconfidence in bull markets leads to overexposure. Financial advisors who are commission based may push products rather than strategy, so understanding fee structures is essential.

Read: [Active vs Passive Investing: What Works Best for Busy Doctors?]

Solution: Embrace a Simple, Diversified, Low-Cost Index Fund Investing Strategy

Use broad market index funds. Rebalance your investments every year. Focus on long term investment strategies tied to goals, not news cycles.

Mistake 6: Inadequate Risk Management and Protection

Your ability to earn is your greatest asset. Yet many physicians skip disability insurance or carry minimal life coverage. That exposes families to catastrophic risk.

Disability insurance protects income if illness or injury prevents practice. Life insurance protects dependents. Umbrella policies protect against lawsuits. Estate planning ensures assets pass smoothly.

Doctors in demanding specialties face burnout and health risks. Without protection, years of savings can vanish quickly.

Solution: Safeguard Your Income, Your Family, and Your Legacy with Proper Protections

Work with qualified financial advisors who understand physician risk profiles. Align coverage with income, dependents, and practice exposure.

Mistake 7: Neglecting Proactive Tax Planning and Efficiency

Taxes are one of the largest expenses physicians face. Yet many treat tax planning as an annual event instead of a strategy. Missed deductions, poor timing of asset sales, and lack of coordination with investments reduce after tax wealth.

Tax loss harvesting, business expense tracking, and smart timing of income can significantly improve outcomes. Physicians in private practice have even more opportunities for structured financial planning.

Solution: Work with a Competent Tax Accountant for Ongoing Tax Planning and Optimization

A proactive accountant becomes part of your wealth management team, not just a form preparer.

Your Path to Financial Success in Your 30s and 40s: Strategic Actions

Financial literacy must become ongoing. Read, listen, learn. Personal finance is a clinical skill for your own life.

Clearly define what financial independence means to you. Know your number. Build retirement planning targets around it.

Seek fee only financial advisors who provide behavioral coaching, not product sales. Monitor net worth annually. Prioritize asset growth over income growth.

Read: [Physician Retirement Planning: How Doctors Can Retire Confidently (Even If They Start Late)]

Read: [Financial planning for doctors]

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Yes, many doctors struggle financially even though they earn a lot. This happens because of lifestyle inflation, delayed investing, large student loans, poor financial planning, and underused retirement accounts. Income does not equal net worth, and without structure, high earnings get absorbed by spending, debt, and taxes.

Retirement blunders usually refer to common financial mistakes that reduce long-term wealth, and many of them overlap with the errors doctors make in their 30s and 40s. These mistakes include delaying investing. They also include not using tax-advantaged retirement plans, carrying high-interest debt, poor asset allocation, chasing hot investments, inadequate insurance, ignoring tax planning, withdrawing too early from retirement accounts, and failing to define a clear retirement goal. The exact list varies by source, but the theme is the same: lack of planning and emotional decisions cost more than low income ever does.