If you are a doctor with extra cash, you should keep some money in a savings account for safety and easy access. You should invest the rest for long-term growth. Do this only after you understand timing, debt, and risk.

The confusion comes from not knowing how much belongs where, especially when student loan debt, irregular income, and burnout already create stress.

This guide walks you through that decision step by step, using plain language, real numbers, and physician-specific realities. By the end, you will know how to treat every extra dollar you earn without guessing or copying generic advice.

Understanding Financial Health: The First Step

Before choosing between a savings account and investing, you need clarity on your financial base. Doctors often skip this step because income feels high, but high income does not equal financial security.

Assessing Current Financial Situation

Start with cash flow. Not net worth. Not projections.

Ask four questions:

- How much comes in monthly after tax?

- How much goes out consistently?

- How much is unpredictable?

- What is left over every month?

Many physicians discover they are technically high earners but emotionally paycheck to paycheck. If this feels familiar, pause and read:

Read: [How High-Income Doctors Can Stop Living Paycheck to Paycheck]

You cannot decide between saving and investing until you know whether extra cash is truly surplus or just temporarily unassigned.

Identifying Personal Financial Goals

Money without a job creates anxiety.

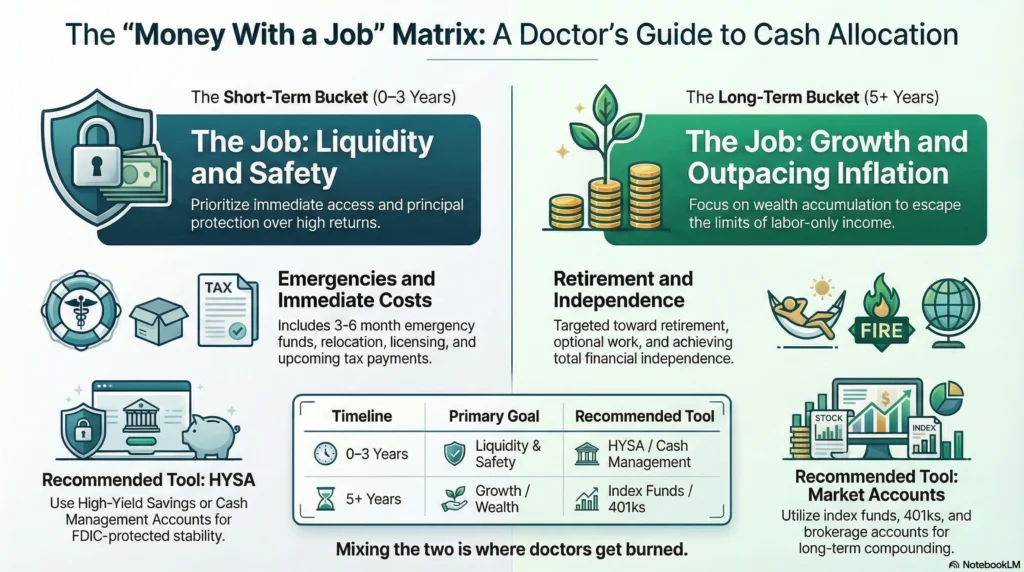

You need to separate short-term goals from long-term goals:

- Short-term goals include emergencies, relocations, licensing costs, and large purchases.

- Long-term goals include retirement, optional work, and financial independence.

Short-term money belongs in a savings account. Long-term money belongs in an investment account. Mixing the two is where doctors get burned.

The Case for High-Yield Savings Accounts

A savings account is not a bad decision. It is a protective tool. But it has a ceiling.

Importance of Liquidity and Safety

Liquidity matters more than returns in the short term. Cash gives you options. It reduces anxiety. It protects against forced selling during market downturns.

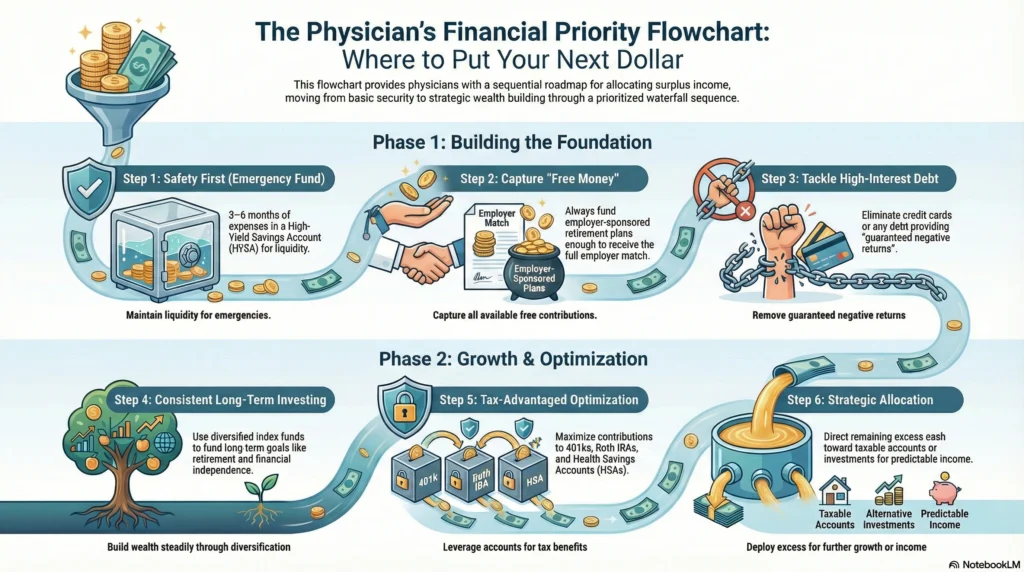

Every physician should maintain an emergency fund covering three to six months of expenses. That fund belongs in a savings account or high-yield savings account.

These accounts provide:

- Daily liquidity

- FDIC protection

- Stable balance regardless of market conditions

This is non-negotiable. Investing without an emergency fund increases stress and poor decision-making.

Role in Emergency Funds

Your emergency fund exists to handle:

- Job transitions

- Health issues

- Unexpected student loan changes

- Family emergencies

Without it, market volatility feels personal.

High-yield savings account rates can fluctuate. During high-rate environments, they may reach 4 to 5 percent. But that interest rate is not guaranteed long term.

Limitations in Interest Earnings

Even strong savings rates have limits.

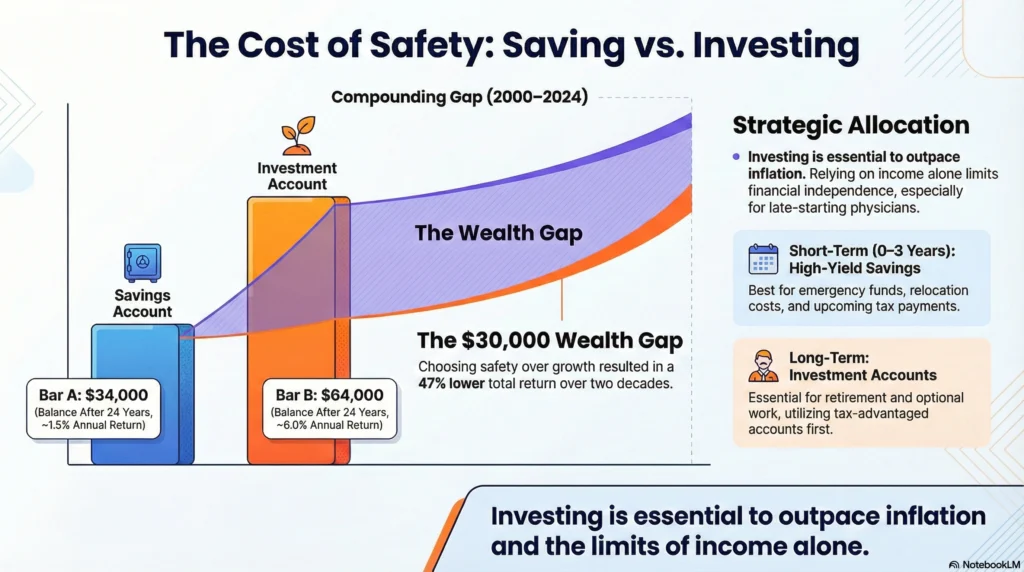

Savings accounts generally offer much lower returns than investments, often under 2 percent long term, which limits wealth building potential.

An example by Blackrock makes it super clear:

If you saved $100 per month from 2000 to 2024 in a savings account earning about 1.5 percent, you would have roughly $34,000. If you invested the same amount earning around 6 percent, it could grow to about $64,000.

This difference compounds quietly over decades.

The Benefits of Investing

Once safety is covered, investing is how doctors escape the limits of income alone.

Potential for Higher Returns

Long-term investing has historically outpaced cash.

The S&P 500 has delivered average annual returns in the 7 to 8 percent range over long periods, far exceeding typical savings account interest rates.

This is why investing is essential for retirement savings, especially for physicians who start late due to medical schools and training.

Importance of Risk Assessment

Risk is not binary. It is contextual.

Risk depends on:

- Time horizon

- Stability of income

- Existing emergency fund

- Emotional tolerance for volatility

Short-term money should not be exposed to market swings. Long-term money should not be trapped in cash.

This is where asset allocation matters. Not aggressive. Not conservative. Appropriate.

Index funds are a common starting point because they provide diversification, low cost, and simplicity. You do not need to pick stocks to participate in market growth.

Availability of Employer Match Programs

If you have access to employer matching in retirement accounts, this is immediate value.

Not capturing an employer match is equivalent to declining free compensation.

If you are unclear how this fits with saving versus investing, read:

Read: [Physician Net Worth by Age: What Doctors Should Expect at Every Stage]

Debt Considerations

Debt changes the math.

Doctors carry more student loan debt than almost any other profession, and ignoring this distorts saving and investing decisions.

Evaluating High-Interest vs Low-Interest Debt

High-interest debt, like credit cards, demands immediate attention. This is guaranteed negative investment returns.

Student loans are different.

Student loan debt often carries lower interest rates and may qualify for income-driven repayment or loan forgiveness programs. That changes the strategy.

Blindly paying down student loans before investing is not always optimal.

Prioritizing Loan Repayment Strategies

You must understand:

- Interest rate

- Repayment plan

- Loan forgiveness eligibility

- Emotional stress level

Doctors with stable income and long-term goals often benefit from simultaneously investing and managing student loan payments, rather than delaying one entirely.

For deeper clarity, read:

Read: [Student Loan Repayment Strategies for Doctors: A Clear Plan for High-Income Physicians]

Balancing Act: Saving, Investing, and Debt Reduction

This is the core skill. Not picking funds. Not chasing returns.

Crafting a Balanced Financial Plan

A simple framework for doctors:

- Build emergency fund in a savings account

- Capture employer match

- Pay off high-interest debt

- Invest consistently for long-term goals

- Optimize tax-advantaged options

- Allocate excess cash strategically

Doctors who skip structure tend to over-save out of fear or over-invest out of confidence.

If you already have surplus and want predictable income, explore:

Read: [Best Cash Flow Investments for Doctors Who Want Predictable Income]

Tax-Advantaged Accounts

Taxes quietly erode investment returns.

Maximizing Retirement Accounts

Retirement accounts offer tax advantages that amplify compound interest over decades.

For most physicians, these accounts should be funded before taxable investment accounts.

This includes 401k plans, Roth IRA strategies, and sometimes SEP IRA options for independent contractors.

Utilizing Health Savings Accounts (HSAs)

A health savings account combines saving and investing if used properly.

It can fund medical expenses now or become a stealth retirement vehicle later.

Formulating a Personalized Strategy

There is no universal formula. Only sequencing.

Aligning with Long-Term Financial Goals

Your investment strategy should align with long-term goals, not headlines.

Ask:

- What lifestyle do I want later?

- When do I want work to be optional?

- How much volatility can I tolerate today?

These answers shape decisions more than market predictions.

Each goal requires different investment returns, risk tolerance, and time horizons.

If you want to model outcomes, explore:

Check Out: [Future Net Worth Calculator for Doctors]

Managing Short-Term Needs vs Long-Term Gains

Short-term money stays liquid.

Long-term money gets invested.

Medium-term money uses blended strategies.

If you want a practical tool to test scenarios, check out: [Investment and Savings Calculator for Doctors]

How Guidance Fits Without Pressure

Many doctors ask when to involve a financial advisor.

The right answer is when complexity creates hesitation.

At Medicine and Money Show, we focus on education first. No products. No pressure. Just clarity.

Some physicians continue by:

- 📕 Reading our book Freedom for Doctors for structured guidance

- 📥 Downloading the free Physician Financial Flight Plan to test the LIFTOFFNOW framework

- 🎧 Listening to the audio version of this guide between shifts

- 📞 Booking a short clarity call to talk through personal numbers

FAQ

You should keep money needed in the next 0–3 years in savings and invest money meant for long-term goals like retirement or financial independence. The key condition is timing: short-term needs require safety, while long-term goals require growth to outpace inflation.

They have become popular because rising interest rates temporarily boosted yields to 4–5%, making them attractive for parking cash safely. However, these rates fluctuate and still do not replace investing for long-term growth.

High-yield savings accounts are FDIC-insured savings accounts that pay higher interest than traditional bank savings accounts. They are best used for emergency funds and short-term cash, not wealth building.

High-yield cash or cash management accounts are brokerage-linked accounts that hold cash and often invest it in money market funds while offering checking features. They may provide higher yields than savings accounts but are not always fully FDIC-insured in one place.

The main advantages are liquidity, safety, and higher interest than traditional savings accounts. These accounts reduce risk and provide flexibility for near-term expenses or uncertain cash needs.

The biggest disadvantage is limited long-term growth, as returns usually lag inflation and investing. Over time, relying too heavily on these accounts can slow wealth accumulation.

You should use them for emergency funds, upcoming tax payments, relocation costs, or any money you will need within a few years. They are not ideal for retirement or long-term financial goals.

Choose one with FDIC insurance (or clear sweep protection), competitive interest rates, no fees, and easy access to funds. Stability and transparency matter more than chasing the highest advertised rate.

Alternatives include money market funds, short-term Treasury bills, and short-duration bond funds. These can offer slightly higher yields than savings accounts but still carry more risk than insured bank deposits.