Doctors who want predictable income should focus on cash flow investments that balance stability, liquidity, and sustainability. They should avoid chasing maximum returns. The right approach depends on your career stage, time horizon, risk tolerance, tax bracket, and existing obligations like student loans or family expenses. The core goal stays the same: reliable income without constant oversight or unnecessary stress.

This guide is written for physicians who already earn well but want their money to work harder and more predictably. Every section explains not just what an investment is, but why it matters, when it fits, and where it breaks down. Nothing is held back.

High-Yield Savings Accounts: Liquidity and Safety

High-yield savings accounts are the simplest place to generate low-risk cash flow while preserving principal and daily access to funds. These accounts pay interest rates far higher than traditional bank savings accounts, especially in higher-rate environments.

High-yield savings accounts are protected by FDIC insurance up to $250,000 per depositor per bank, which makes them one of the safest places to hold cash while still earning yield. This protection is critical for physicians who prioritize capital preservation for near-term needs or uncertainty.

Despite improved interest rates, savings accounts usually fail to keep pace with inflation over long periods. This limits their usefulness for long-term income or retirement savings.

Best use cases for doctors

- Emergency fund storage

- Temporary parking for bonuses or large cash inflows

- Bridge funding before deploying capital elsewhere

Where this breaks down

- Limited long-term purchasing power

- Not suitable for building passive income at scale

Read: [Savings Account vs Investing: What Doctors Should Do With Extra Cash]

Money Market Funds: A Secure Option

Money market funds are often misunderstood as savings accounts, but they are regulated investment products designed to preserve value while generating modest income.

Money market funds invest in short-term, high-quality debt such as treasury bills, repurchase agreements, and commercial paper. They are not FDIC insured, but they are regulated to maintain stability and low volatility.

Source: SEC overview of money market funds

This makes money market funds attractive for physicians who want higher yield than a savings account without locking money away. Money market accounts offered by banks are different products, often FDIC insured, but usually pay lower yields than money market funds.

Best use cases

- Holding large balances while waiting to invest

- Managing cash flow for irregular income

- Supplementing an emergency fund

Limitations

- Returns fluctuate with interest rates

- No long-term growth engine

Money market funds and money market accounts are cash management tools, not wealth builders.

Dividend-Paying Stocks: Income and Growth Potential

Dividend-paying stocks provide ongoing cash flow while allowing participation in long-term market growth. For physicians with longer time horizons, this combination is powerful.

The S&P 500 has historically delivered average annual returns of roughly 7 to 8 percent, combining dividends and price appreciation over extended periods.

Source: Historical stock market returns

Dividend income can supplement cash flow while index funds provide broad exposure across asset classes. Many doctors prefer dividend-focused index funds to avoid stock picking.

Best use cases

- Mid-career physicians

- Doctors building passive income streams

- Long-term retirement savings

Risks to understand

- Market volatility

- Dividend cuts during downturns

Index funds remain one of the most efficient vehicles for accessing dividend-paying companies while maintaining diversification.

Real Estate Investments: Steady Rental Income

Real estate remains one of the most reliable cash flow generators when executed correctly. Rental income provides monthly cash flow that often adjusts with inflation.

Real estate income historically shows low correlation with stock market returns, which improves diversification across asset classes.

Source: Real estate performance data

Physicians are drawn to real estate for both cash flow and tax advantages, including depreciation and expense deductions.

Best use cases

- Physicians with stable income

- Doctors seeking inflation protection

- Long-term passive income builders

Tradeoffs

- Illiquidity

- Management responsibilities

- Local market risk

Real estate works best when paired with conservative leverage and professional property management.

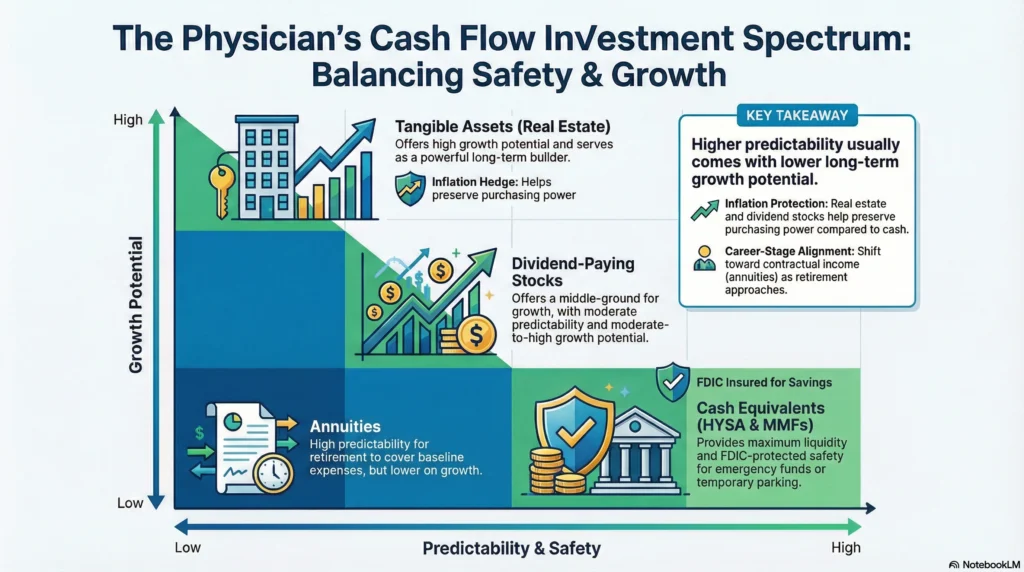

Annuities: Guaranteed Income Sources

Annuities convert capital into contractual income. They are not growth investments, but they provide predictable cash flow that removes market risk.

Single Premium Immediate Annuities (SPIA)

SPIAs provide immediate, guaranteed income for life or a fixed period. They are often used to cover baseline living expenses later in life.

Deferred Income Annuities (DIA)

DIAs delay payments until a future date, increasing income later and protecting against longevity risk.

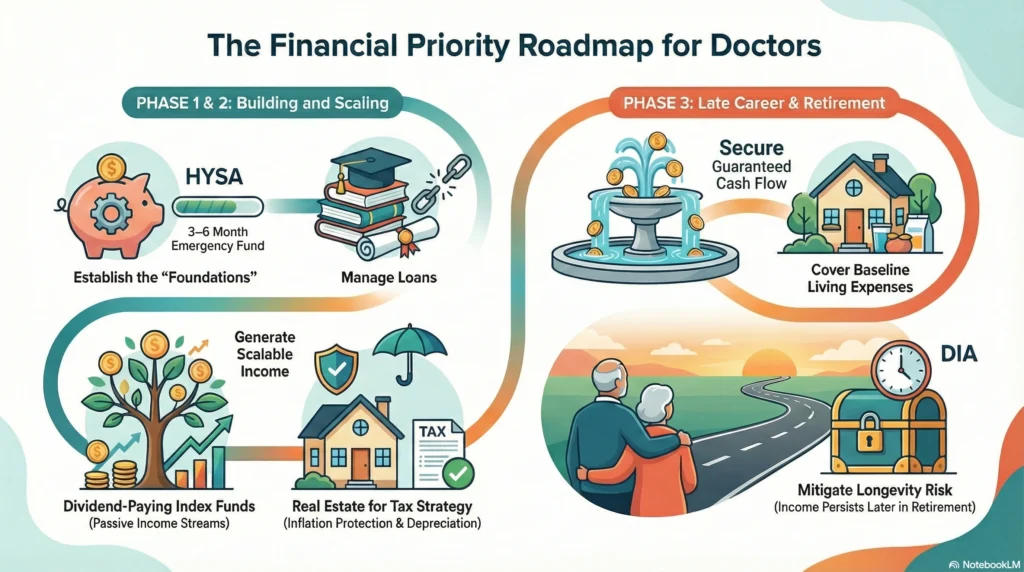

Reliable cash flow becomes more important than raw growth in later career stages and during retirement.

Understanding Risk Tolerance for Physicians

Risk tolerance is shaped by more than emotion. It is influenced by debt, career stability, and time horizon.

Physicians often carry student loans well into their attending years, which affects how much risk is appropriate early on. Cash flow stability matters more when obligations are high.

Risk tolerance should be reassessed as:

- Student loans decline

- Income stabilizes

- Retirement approaches

Balancing Debt Reduction With Investment Strategies

Debt reduction is a guaranteed return. High-interest debt almost always outweighs investment returns.

Student loans complicate this decision. Federal student loans with income-based repayment or loan forgiveness programs may justify investing alongside paying off loans. Aggressive payoff may not be necessary.

The right balance protects cash flow while maintaining progress toward long-term financial goals.

Read: [How High-Income Doctors Can Stop Living Paycheck to Paycheck]

Wealth and Asset Management Tailored for Physicians

Wealth management for doctors must integrate cash flow planning, insurance coverage, and tax efficiency.

This includes:

- Coordinating retirement accounts

- Managing asset allocation across asset classes

- Adjusting exposure as income grows

Portfolio management should reduce decision fatigue, not add complexity.

Tax Considerations in Cash Flow Investments

Taxes determine real returns. Interest income is taxed at ordinary rates, while qualified dividends and municipal bonds may receive preferential treatment depending on your tax bracket.

Municipal bonds are especially relevant for high-income physicians seeking tax-efficient cash flow.

Tax-advantaged accounts such as Roth IRAs and retirement accounts protect growth but often limit access.

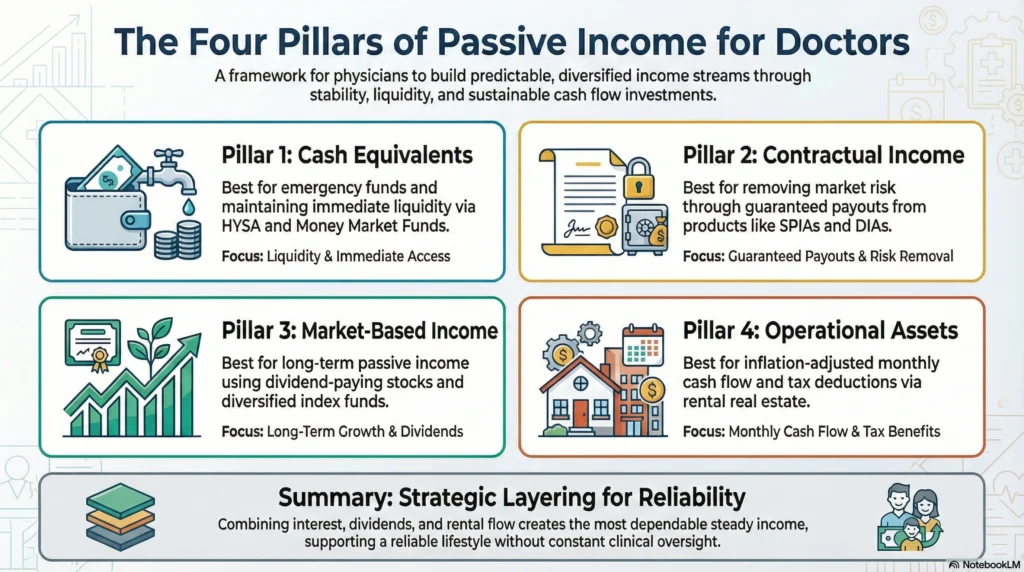

Grouping Passive Income Activities for Physicians

Passive income falls into clear categories:

- Cash equivalents

- Market-based income

- Contractual income

- Operational assets

Grouping investments this way simplifies portfolio management and clarifies risk exposure.

Passive investments should support lifestyle goals, not replace clinical income prematurely.

Investing With Longevity and Retirement Planning in Mind

Physicians often retire later but live longer, making predictable cash flow critical.

Retirement savings should prioritize sustainability and inflation protection. They should not focus only on account balances.

Read: [Physician Net Worth by Age: What Doctors Should Expect at Every Stage]

Check out: [Investment and Savings Calculator for Doctors]

Check out: [Future Net Worth Calculator for Doctors]

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Investments that generate contractual or recurring payouts provide the most predictable income. These include high-yield savings accounts, money market funds, dividend-paying stocks, rental real estate, and certain annuities. The tradeoff is that higher predictability usually comes with lower long-term growth potential.

There is no single best investment, but a combination of cash equivalents, dividend-focused investments, and real estate tends to create the most reliable steady income. The right mix depends on your time horizon, risk tolerance, and whether income is needed now or later.

The best cash flow strategy layers multiple income sources such as interest income, dividends, and rental cash flow instead of relying on one asset. Doctors benefit most by pairing liquid income sources with longer-term growth assets to avoid sacrificing future flexibility.

The best investments for doctors balance predictability, tax efficiency, and low time commitment. These include high-yield savings accounts for liquidity, index funds for scalable income and growth, real estate for inflation-adjusted cash flow, and annuities for guaranteed income later in life.

Most physicians should keep three to six months of essential expenses in an emergency fund, with higher amounts for those with variable income, practice ownership, or family dependents. This fund should remain liquid and low risk, not invested for growth.