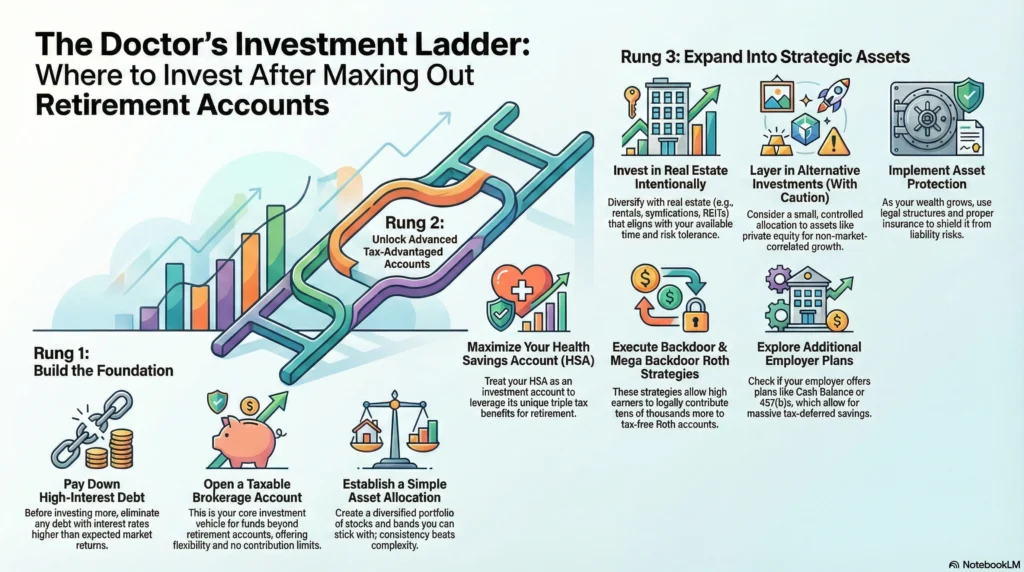

Once you’ve maxed out your 401k and Roth IRA, the smartest place for doctors to invest next is a taxable brokerage account—unless high-interest debt, cash-flow gaps, or missed advanced tax strategies should come first.

The exact order depends on your debt profile, income stability, and access to additional retirement plans, but the framework does not change.

If you’re here, you’re likely feeling stuck.

You’ve done what every checklist told you to do.

You’ve filled your Roth IRA, maxed your retirement accounts, and hit the contribution limits.

And now the advice online suddenly gets vague.

This guide solves that.

What follows is a decision-driven playbook used in real financial planning for doctors. Not theory, not generic advice. You’ll learn where to invest, why each option exists, and how to sequence decisions so your money actually compounds instead of drifting.

Step 1: Prioritize Paying Down High-Interest Debt

What to do

Before adding new investments, review all liabilities—especially student loan balances, private debt, and any interest rate above long-term market expectations.

Why it matters

Investing while carrying high-interest debt works against compound interest.

Every dollar earning 6% while another dollar costs 8% is a net loss—no matter how “diversified” your portfolio looks.

This step protects future cash flow and stabilizes your foundation before scaling investments.

👉 Read: [Student Loan Repayment Strategies for Doctors: A Clear Plan for High-Income Physicians]

What usually goes wrong

Doctors often:

- Assume investing always beats debt

- Ignore variable interest rates

- Treat debt and investing as separate decisions

They aren’t. This step determines whether future returns actually stick.

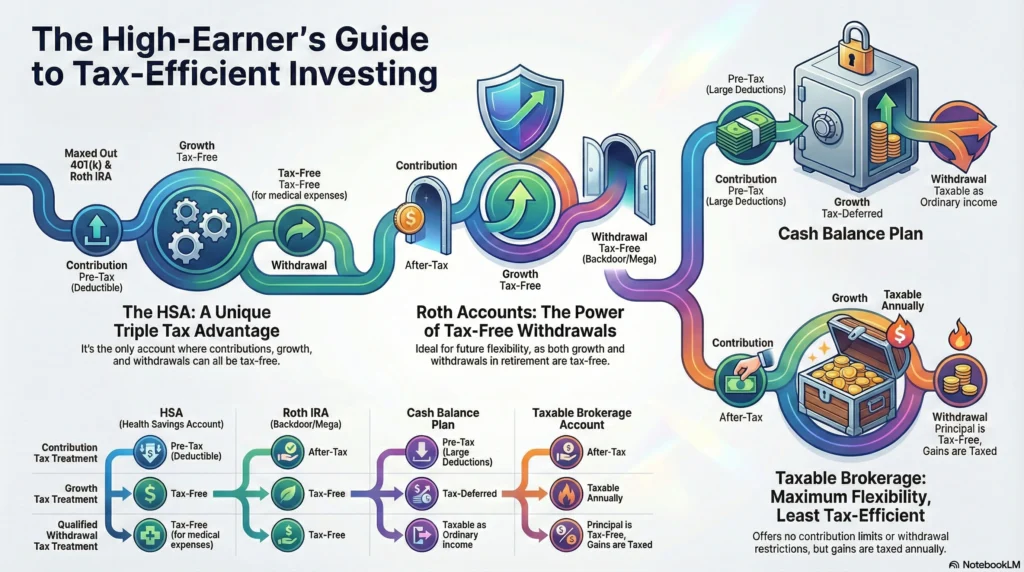

Step 2: Use a Taxable Investment Account

What to do

Open and fund a Brokerage account once tax-advantaged accounts are full.

Why it matters

Taxable brokerage accounts:

- Have no contribution limits

- Offer total flexibility

- Allow access before retirement age

- Scale with income as you become a high earner

According to Ramsey Solutions, once tax-advantaged space is maxed out, a taxable brokerage account becomes the most flexible investing vehicle with no income or contribution caps

This is where most physician wealth is actually built.

What usually goes wrong

- Treating it like a “play account”

- Overtrading

- Ignoring tax strategies like Tax-loss harvesting

- Poor asset allocation

👉 Read: [Retirement Account vs Investment Account]

Step 3: Build a Smart Asset Allocation (Not a Fancy One)

What to do

Build an asset allocation that:

- You understand

- You can stick with during volatility

- Aligns with your income stability, timeline, and goals

For most doctors, that means a globally diversified portfolio spread across:

- Stocks, Mutual Funds, ETFs (growth engine)

- Bonds (stability and liquidity)

- Cash equivalents (short-term flexibility)

Not complexity.

Not cleverness.

Not what sounds impressive at a dinner party.

A smart asset allocation fits into your overall retirement plan, not just your brokerage account.

Why it matters

Doctors earn well, but income often comes later and can be volatile due to:

- Burnout

- Practice changes

- Malpractice risk

- Shifts in reimbursement

That makes consistency more valuable than optimization.

A clean, well-structured allocation supports:

- Long-term retirement funds

- Predictable compounding

- Emotional discipline during market stress

Most long-term investing success comes from staying invested—not picking winners.

This is where strong financial plans quietly outperform aggressive ones.

How to actually build it

A physician-friendly framework looks like this:

- Growth assets (equities) for long-term goals

- Defensive assets (bonds) for stability

- Cash for near-term needs

Then apply this across all accounts, not inside each account.

For example:

- Stocks inside tax-advantaged retirement accounts

- Bonds inside tax-deferred accounts

- Tax-efficient funds in taxable accounts

This approach improves after-tax returns without increasing risk—one of the most overlooked tax benefits in investing.

What usually goes wrong

- Chasing performance

- Overreacting to headlines

- Overcomplicating portfolios

- Ignoring how accounts interact

Another common mistake is confusing investment selection with allocation.

Buying great funds doesn’t fix a poor structure.

A portfolio filled with overlapping mutual funds, trendy ETFs, or speculative bets isn’t diversification—it’s noise.

Simple portfolios compound.

Fancy ones distract.

Step 4: Backdoor and Mega Backdoor Roth Strategies (Without Tripping the IRS)

Roth assets give you:

- Tax-free growth

- Tax-free withdrawals

- Future flexibility

This flexibility is very valuable in retirement.

Unlike traditional accounts, Roth money:

- Doesn’t force withdrawals

- Doesn’t increase taxable income later

- Helps manage Medicare premiums and taxes

That’s why Roth strategies sit at the core of advanced retirement planning for physicians.

Backdoor Roth IRA

- Contribute to a Traditional IRA (non-deductible)

- Convert that amount to Roth shortly after

- Avoid holding pre-tax IRA balances elsewhere

The key risk here is the pro-rata rule.

If you already have pre-tax money in a Traditional IRA, the IRS treats all IRAs as one bucket.

That’s where people get burned.

Used properly, the Backdoor Roth IRA is one of the simplest ways to build tax-free assets annually—especially when layered into long-term financial plans.

According to Fidelity, backdoor Roth IRAs are a common next step for aggressive savers after maxing retirement accounts

Mega Backdoor Roth

It works inside certain employer plans that allow:

- After-tax 401k contributions

- In-service Roth conversions

This can allow tens of thousands of dollars per year to move into Roth space—far beyond standard limits.

Key requirements:

- Your employer plan must allow it

- The execution must be precise

- Timing matters

Many physicians never check their plan document—and miss this entirely.

When available, the mega backdoor roth is one of the most powerful levers in modern physician investing.

And yes, it can coexist with:

- A Roth 401k

- A Traditional 401k

- A Backdoor Roth IRA

But coordination matters.

👉 Read: [401k investment alternatives]

Step 5: Maximize Health Savings Accounts (HSAs)

What to do

Treat your Health Savings Account (HSA) as a long-term investment vehicle, not just a place to park money for next year’s copays.

If you’re enrolled in a qualifying high-deductible health plan (HDHP), your HSA can become one of the most powerful tools in your retirement plan.

Here’s the correct sequence physicians should follow:

- Contribute the maximum allowed under current contribution limits

- Pay current medical expenses out-of-pocket when cash flow allows

- Invest HSA funds instead of leaving them in cash

- Save receipts for future reimbursement

- Use the account strategically later in retirement

This turns the HSA into a stealth retirement asset.

Why it matters

HSAs are unique because they offer triple tax benefits:

- Contributions reduce taxable income

- Growth is tax-deferred

- Withdrawals for qualified medical expenses are tax-free

No other account combines all three.

For physicians, future healthcare costs are almost guaranteed. That makes HSAs one of the most reliable components of long-term retirement planning, especially when layered on top of a 401k, Roth IRA, or Backdoor Roth IRA strategy.

When invested properly, HSAs can function like a supplemental retirement account—without required minimum distributions.

According to Consilio Wealth Advisors, HSAs as one of the most powerful next steps after retirement limits are reached

What usually goes wrong

Most doctors misuse HSAs in three common ways:

- Leaving money in cash instead of investing it in diversified mutual funds

- Spending the HSA immediately instead of letting it compound

- Treating it like a checking account instead of an investment account

Another mistake is ignoring coordination with broader financials plans. HSAs work best when integrated with your tax strategy, insurance planning, and long-term investment horizon.

For self-employed physicians, HSAs can also be paired with higher-deductible plans to improve cash flow efficiency while still protecting against catastrophic risk.

HSAs aren’t about optimization tricks.

They’re about patience and discipline.

Step 6: Add Spousal and Household-Level Accounts

What to do

Once your own retirement accounts are optimized, expand your strategy to the household level.

Even if your spouse doesn’t earn income—or earns much less—you may still unlock powerful planning opportunities through:

- Spousal IRAs

- Coordinated retirement contributions

- Strategic roth conversions across tax brackets

- Income smoothing over decades

Household-level planning often creates more upside than any single investment.

Why it matters

Taxes don’t care who earned the money.

They care how it’s structured.

By planning jointly, physicians can:

- Shift income across accounts strategically

- Optimize withdrawal sequencing in retirement

- Reduce lifetime tax drag

- Build flexibility for early or partial retirement

This is especially important when one partner plans to reduce work hours, exit clinical practice earlier, or focus on non-clinical roles.

Using spousal accounts correctly strengthens long-term retirement planning and reduces reliance on a single income stream.

What usually goes wrong

The biggest mistake is treating finances as “mine” and “yours” instead of “ours.”

Other common issues:

- Ignoring spousal eligibility for IRAs

- Failing to coordinate asset location

- Overfunding taxable accounts while leaving spousal tax-advantaged space unused

Another overlooked factor is catch-up contributions. When you get close to your 50s, making catch-up contributions across household accounts can speed up retirement savings. This can happen without adding more risk.

Some physicians also overuse life insurance products here without fully understanding whether they’re solving a tax problem—or just adding complexity.

Spousal planning isn’t about control.

It’s about alignment.

Step 7: Use Children’s Accounts Strategically (Not Emotionally)

What to do

When investing for children, lead with strategy, not guilt or pressure.

Physicians often rush into children’s accounts out of fear:

- “I don’t want them buried in student debt”

- “I didn’t have help, so I should overcompensate”

- “This is the only way to give them a head start”

Those emotions are understandable—but unchecked, they can derail your own financial independence.

Why it matters

Children’s accounts should support, not sabotage your long-term investment strategies.

Used correctly, they can:

- Fund education efficiently

- Teach financial literacy

- Create flexibility without obligation

- Protect your own retirement trajectory

529 plans, custodial accounts, and (in limited cases) Roth IRAs for working children can all play a role—but only when coordinated with your broader financials plans.

The priority order matters:

- Your retirement security

- Your financial flexibility

- Then education funding

Children can borrow for school.

You cannot borrow for retirement.

What usually goes wrong

- Overfunding 529s before securing their own retirement

- Treating education savings as guaranteed commitments

- Investing too conservatively for long-term horizons

Another mistake is failing to match the investment approach to the timeline. Long-term education funds can still be invested in growth-oriented mutual funds early on, rather than sitting idle in cash-like options.

Children’s accounts should create options—not obligations.

A well-structured plan gives your kids flexibility without compromising your future.

Step 8: Access Additional Employer Retirement Plans

Cash Balance Plans

What to do

For practice owners and self-employed physicians, explore Cash Balance Plans.

Why it matters

They allow six-figure annual deferrals.

According to Finance for Physicians, cash balance plans and 457(b)s let doctors shelter far more income beyond standard 401k limits

What goes wrong

- Poor plan design

- Ignoring staff costs

Defined Benefit Plans

What to do

Evaluate defined benefit plans later in your career.

Why it matters

They accelerate retirement funding when income peaks.

Step 9: Real Estate Investing (Beyond “Buy a Rental” Advice)

What to do

If you’re going to add real estate, do it intentionally—based on time, risk tolerance, and role, not hype.

For physicians, real estate investing usually falls into four buckets:

- Direct rental properties

- Self-storage real estate investments

- Syndications and private funds

- REITs inside brokerage or retirement accounts

Each has a very different impact on cash flow, asset protection, and long-term financial independence.

Why it matters

Real estate can:

- Diversify beyond stocks and mutual funds

- Produce income not tied to your clinical hours

- Offer inflation hedging and tax advantages

- Reduce portfolio volatility when structured correctly

According to Ramsey Solutions, rental real estate is a viable post-401k investment, but warns it requires work and risk tolerance

That’s why real estate appears so often in advanced retirement planning conversations for doctors.

But it’s also one of the fastest ways physicians destroy capital when rushed.

What goes wrong

- Overleverage

- Mistaking active work for “passive income”

Self-Storage Real Estate

Self-storage real estate has quietly become one of the most physician-aligned real estate models.

Why it works for doctors:

- Lower maintenance than residential rentals

- Sticky tenants (low churn)

- Recession-resistant demand

- Scales well into semi-passive ownership

For high-income physicians who want real estate exposure without tenant drama, self-storage often fits better than single-family rentals.

What usually goes wrong:

- Investing without understanding local supply risk

- Joining syndications without reviewing fee structures

Self-storage is still real estate. Due diligence matters.

Real Estate Syndications & Funds

Best for:

Doctors who want to invest in real estate but do not want to manage it.

You invest capital.

The sponsor handles acquisition, management, and exit.

Why it matters:

- Frees your time

- Offers access to larger assets

- Can complement a Brokerage account strategy

What usually goes wrong:

- Blind trust in sponsors

- Chasing projected returns instead of risk-adjusted returns

REITs (Real Estate Without Illiquidity)

REITs allow you to own real estate exposure through public markets.

Where they fit best:

- Inside tax-advantaged accounts

- As a diversification layer, not a core strategy

Real estate grows net worth. Structure determines whether it grows freedom.

👉 Read: [Doctor Net Worth vs Financial Freedom: Why They’re Not the Same Thing]

Step 10: Diversify Beyond Conventional Investments

What to do

Once your core strategy is built, you may layer in alternative investments—but only intentionally.

Common alternatives that interest physicians include:

- Private equity funds

- Private real estate funds

- Venture-style investments

- Crypto exposure (small, controlled)

- Specialty life insurance strategies (advanced cases only)

Why it matters

As income rises, concentration risk increases.

Diversifying beyond public markets can:

- Reduce portfolio correlation

- Add return drivers unlinked to equities

- Improve long-term asset allocation

But alternatives are amplifiers—not foundations.

Private Equity & Private Funds

Best for:

Doctors with:

- Strong cash flow

- Long time horizons

- High risk tolerance

What goes wrong:

- Over-allocating early

- Ignoring illiquidity

- Confusing access with advantage

Private equity is not “better.”

It’s different.

Crypto

Crypto should never replace:

- Retirement accounts

- Brokerage investing

- Real estate exposure

If used, it belongs in a small satellite allocation, fully acknowledging volatility and regulatory risk.

Life Insurance

Permanent life insurance is often oversold to physicians.

When it might fit:

- Estate planning

- Asset protection

- Very high income + maxed tax strategies

When it doesn’t:

Most early- and mid-career physicians.

What usually goes wrong:

Doctors are sold complexity before clarity.

Diversification works only when integrated into a full plan.

👉 Read: [Financial planning for doctors]

Step 11: Protecting Assets

What to do

As your assets grow, protecting them becomes as important as growing them.

This includes:

- Proper account titling

- Legal structures for real estate

- Insurance coverage review

- Thoughtful separation of personal and investment risk

Why it matters

Physicians face elevated liability risk.

Without structure:

- One lawsuit can undo decades of progress

- Growth outpaces protection

- Stress rises as wealth grows

Asset protection isn’t fear-based.

It’s responsible financial planning.

What usually goes wrong

- Waiting too long

- Overcomplicating structures early

- Copying strategies without personalization

Step 12: Work With Advisors

At this stage, the goal isn’t more products.

It’s better decisions.

This is where guidance matters—not because you can’t learn, but because:

- The cost of mistakes rises

- Opportunity cost compounds

- Strategy beats tactics

Most physicians don’t fail due to lack of intelligence.

They fail due to fragmented decisions made in isolation.

That’s exactly why we built this platform.

Our Approach

We’re building a community of medical professionals who want:

- Financial independence without burnout

- Clear frameworks instead of noise

- Education first, execution second

- Long-term clarity over quick wins

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

No, maxing out your 401(k) alone is usually not enough for doctors to reach financial independence because contribution limits cap how much high earners can shelter each year. Once your income rises, you need additional investment vehicles to grow wealth beyond basic retirement savings.

After maxing out your 401(k) and Roth IRA, doctors should typically invest through taxable brokerage accounts, advanced Roth strategies, HSAs, real estate, or additional employer plans. The right mix depends on cash flow, risk tolerance, tax planning goals, and long-term lifestyle priorities.

Most doctors invest across a mix of retirement accounts, brokerage accounts, real estate, and sometimes private investments. Physicians who earn a lot often focus on saving taxes, spreading out investments, and long-term safety. They do not chase risky high returns.

The 10/5/3 rule is a general guideline that assumes average annual returns of about 10% for stocks, 5% for bonds, and 3% for cash or fixed income. It’s a planning framework—not a guarantee—and actual results vary based on markets and asset allocation.

Only a small percentage of Americans—roughly 2–3%—have a 401(k) balance of $1 million or more. Doctors are more likely than average to reach this level, but it still requires decades of consistent investing and disciplined strategy.

Yes, HSAs are one of the best investment options for doctors because they offer triple tax benefits when used correctly. Contributions to HSAs reduce taxes. The money grows tax-free. Qualified medical withdrawals are also tax-free. This makes HSAs very useful for long-term planning.

Yes, doctors commonly use Backdoor Roth IRAs, Mega Backdoor Roth strategies, and employer-based plans to invest beyond standard limits. These strategies must be executed carefully to avoid tax issues, but when done correctly, they significantly improve long-term after-tax wealth.