Doctors with federal student loans have access to multiple repayment plans, forgiveness programs, and loan repayment benefits that can dramatically reduce monthly payments and long-term debt but only if they choose correctly and avoid irreversible early mistakes. The right option depends on whether you work for a qualifying employer, your income trajectory, your loan type, and how much flexibility you need early in your medical career.

If that already sounds overwhelming, that’s normal.

Most physicians were never taught how student loan repayment works. Medical school trains you to care for patients, not to navigate federal government loan systems, repayment plans, or forgiveness rules.

This guide exists to do one thing:

replace confusion with clarity, fear with structure, and paralysis with a safe next step.

You don’t need to master everything today.

You just need to understand the system well enough to protect yourself.

Understanding Your Student Loan Options

Before you pick a repayment plan, chase loan forgiveness, or think about refinancing, you need to understand the rules of the game.

Most mistakes happen because doctors act before understanding what kind of loans they actually have.

Identify Your Loan Type in 10 minutes

- Log into studentaid.gov

- Download your loan summary

- Highlight:

- Loan type (Direct, PLUS, consolidated)

- Balance

- Interest rate

- Ignore strategy for now — just get clarity

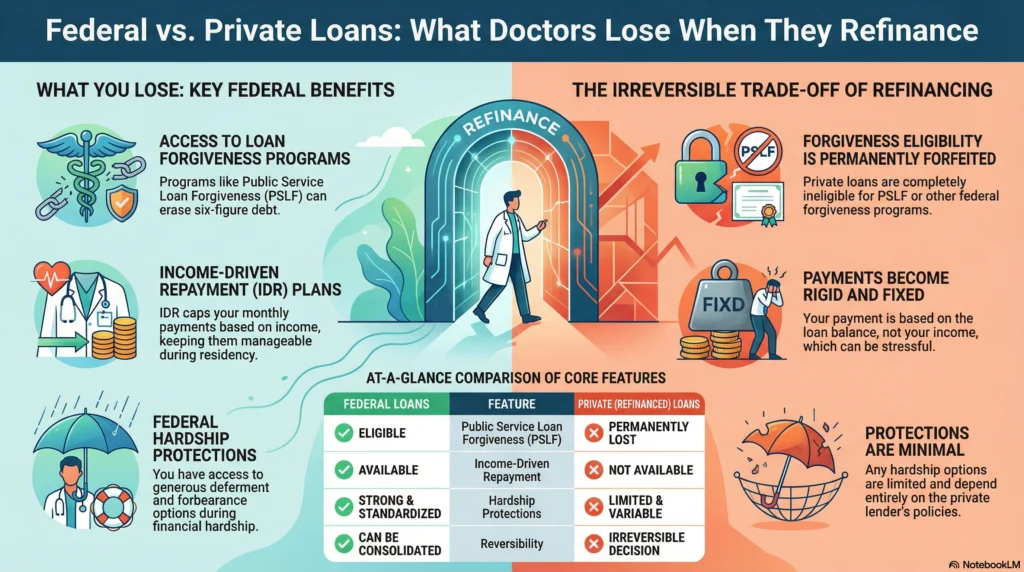

Federal vs. Private Loans

This is the most important distinction you’ll make.

Federal student loans are issued by the federal government.

Private student loans are issued by banks or private lenders.

Why this matters:

- Federal loans qualify for loan repayment programs, forgiveness, and income-based protections

- Private loans do not qualify for federal loan forgiveness

- Federal loans offer flexibility when income is low (like residency)

- Private loans prioritize credit score and fixed monthly payments

As explained by Moneta Group, federal student loans have more repayment flexibility and forgiveness programs (like PSLF and IDR) that private lenders don’t offer.

If you refinance federal loans into private loans too early, you permanently lose:

- Public Service Loan Forgiveness

- Income-driven repayment

- Federal hardship protections

Federal Student Loans | Private Student Loans | |

|---|---|---|

Issued by | Federal government | Banks / private lenders |

Income-driven repayment | ✅ Yes | ❌ No |

Loan forgiveness | ✅ PSLF, NHSC, IDR | ❌ None |

Payment flexibility | High | Low |

Protections during hardship | Yes | Limited |

Eligible for repayment programs | Yes | No |

Best for doctors because | Long training + forgiveness | Lower rates only after forgiveness decisions |

That’s why “lower interest rate” is not always a win.

Importance of Interest Rates and Terms

Your interest rate determines how fast your loan debt grows.

Your repayment term determines how long it follows you.

Federal student loans usually have fixed interest rates.

Private loans may have variable interest rates that rise.

Here’s the key idea for beginners:

- High interest rate + high balance = pressure to repay faster

- Lower interest rate + forgiveness eligibility = flexibility

Two doctors with the same student loan balance can end up paying wildly different totals depending on:

- Their repayment plans

- Whether they qualify for loan forgiveness

- How long they stay on income-based repayment

This is why student loan repayment is strategic, not emotional.

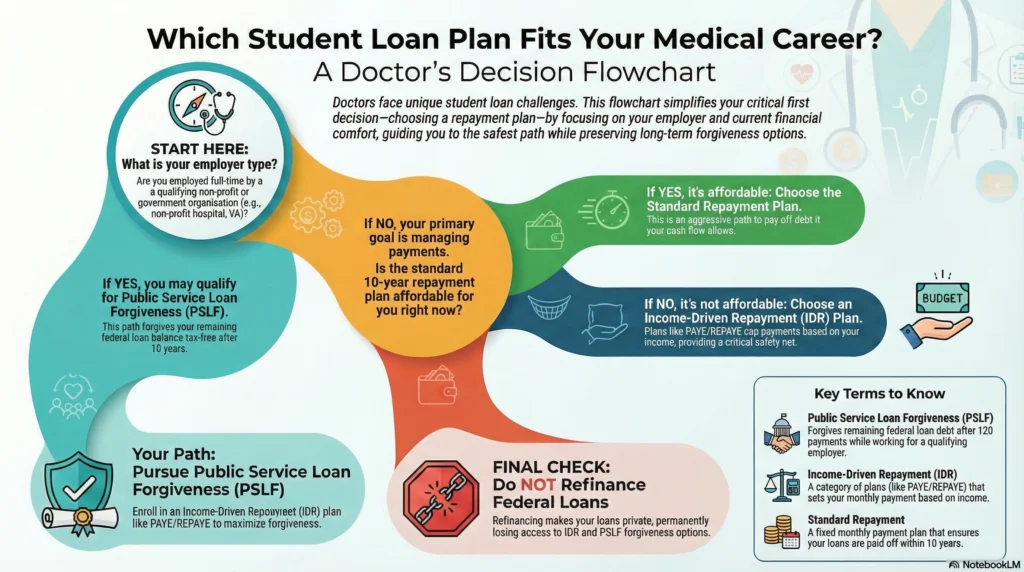

Income-Driven Repayment Plans

If you’re early in your career or your loan debt is large relative to income, income-driven repayment (IDR) is usually the safest place to start.

IDR plans cap your monthly payments based on income, not balance.

Lock in Payment Safety

- Estimate current Adjusted Gross Income

- Use a student loan calculator

- Compare:

- Standard repayment monthly payments

- IDR monthly payments

- If standard payment feels stressful → IDR is your safety net

PAYE and REPAYE Explained

PAYE and REPAYE are the most common repayment plans used by physicians.

In simple terms:

- Payments are based on discretionary income

- Payments adjust annually as income changes

- Payments stay manageable during residency

- Remaining balance may be forgiven later

These plans exist because the federal government recognizes that medical students and residents carry large student loan debt before peak earning years.

PAYE/REPAYE are often paired with public service loan forgiveness when eligible.

PAYE | REPAYE | |

|---|---|---|

Payment cap | 10% discretionary income | 10% discretionary income |

Payment cap limit | Yes (never exceeds standard plan) | No cap |

Interest subsidy | Limited | Stronger (especially during residency) |

Best for | Lower income growth | Residents / early attendings |

PSLF eligible | ✅ Yes | ✅ Yes |

Risk | Income spikes later | Higher payments later |

Important note:

IDR plans are not “avoiding responsibility.”

They are loan repayment benefits designed for long training paths.

If you’re in residency → REPAYE often makes sense.

If income will rise fast → PAYE may protect you later.

Evaluating Income-Contingent Repayment (ICR)

ICR is mainly used in edge cases, such as:

- Parent PLUS loans

- Certain consolidated loans

It usually results in higher monthly payments than other IDR options and is rarely the first choice for physicians unless required by loan structure.

Exploring Forgiveness and Assistance Programs

This is where student loan repayment can feel hopeful—and risky.

Forgiveness programs can erase six figures of loan debt.

But they require strict rules and long-term planning.

Test PSLF Eligibility (No Commitment)

- Look up employer EIN

- Use the PSLF Help Tool

- Confirm employer status

- Save documentation — even if unsure

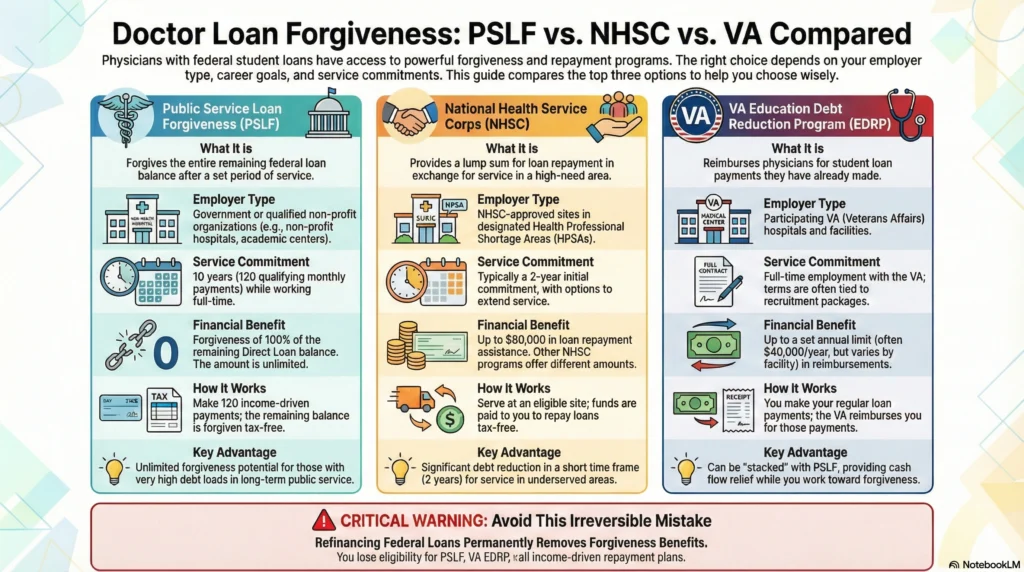

Public Service Loan Forgiveness (PSLF)

PSLF forgives the remaining balance on Direct Federal Loans after 120 qualifying monthly payments while working full-time for a qualifying employer.

Key points beginners must understand:

- Payments must be on a qualifying IDR plan

- Employer must be nonprofit or government

- Payments typically take 10 years

- Forgiveness is tax-free

Many nonprofit hospitals and academic institutions qualify.

PSLF rewards career alignment, not speed.

National Health Service Corps (NHSC) Programs

The NHSC Loan Repayment Program offers up to $80,000 in tax-free loan repayment assistance for clinicians serving in Health Professional Shortage Areas.

Additional programs include:

- NHSC Students to Service – up to $120,000

- Substance Use Disorder Workforce Program – up to $75,000

- Indian Health Service – up to $40,000

As summarized by Physicians Thrive, state and federal service-based loan repayment benefits can dramatically reduce student loan debt for doctors willing to work in underserved areas (https://physiciansthrive.com/financial-planning/a-physicians-guide-to-student-loan-forgiveness).

These programs trade location flexibility for debt relief.

VA Education Debt Reduction Program

The VA Education Debt Reduction Program is one of the most underused loan repayment benefits available to physicians — mostly because it’s poorly explained.

At a high level, EDRP reimburses qualifying physicians for payments they already make on their federal student loans, instead of forgiving balances later like PSLF.

Here’s what makes it different:

- It reimburses actual loan payments, up to an annual cap

- It runs in parallel with PSLF (you can do both)

- It is not automatic — approval is facility-specific

- It applies only to VA-employed physicians

How EDRP Actually Works

If you work full-time at a qualifying VA facility:

- You keep making your normal student loan payments

- The VA reimburses you up to a set annual limit (often ~$40,000/year, varies by facility)

- Reimbursements are paid after you make the payments

- Funds go to you, not the loan servicer

This makes EDRP especially powerful during:

- Early attending years

- High-balance loan periods

- PSLF repayment years

Who EDRP Is Best For

EDRP works best if you:

- Are (or plan to be) VA-employed

- Have large federal student loan debt

- Are already planning PSLF

- Want short-term cash flow relief, not just long-term forgiveness

Step-by-Step: How to Use EDRP Safely:

Step 1: Confirm VA facility participation

Not all VA hospitals offer EDRP. Ask HR or physician recruitment directly.

Step 2: Verify eligible loans

Only qualifying federal student loans count.

Step 3: Enroll in an eligible repayment plan

Most physicians pair EDRP with an income-driven repayment (IDR) plan.

Step 4: Apply during hiring or open enrollment

EDRP is often tied to recruitment packages.

Step 5: Track payments carefully

You must prove payments to receive reimbursement.

Beginner mistake to avoid: assuming EDRP replaces PSLF. It doesn’t. It stacks with PSLF when structured correctly.

Refinancing and Consolidation Considerations

This is where many doctors make irreversible mistakes.

Differences Between Refinancing and Consolidation

- Federal consolidation keeps loans federal and may unlock new repayment plans

- Refinancing replaces federal loans with private loans

Federal Consolidation | Refinancing | |

|---|---|---|

Keeps loans federal | ✅ Yes | ❌ No |

PSLF eligibility | Possibly (if done right) | ❌ Lost |

IDR eligibility | ✅ Yes | ❌ Lost |

Interest rate | Weighted average | New private rate |

Reversible | Sometimes | ❌ Permanent |

Best used when | Fixing eligibility | After forgiveness decision |

Federal consolidation can help with eligibility.

Refinancing permanently removes loan forgiveness benefits.

Refinancing before confirming forgiveness eligibility is one of the most expensive mistakes physicians make.

Beginner Rule of Thumb

- If forgiveness is possible → don’t refinance

- If forgiveness is impossible → refinancing may help later

- If unsure → wait

Time is your ally here.

Impact on Federal Loan Benefits

Once you refinance:

- PSLF is gone

- IDR is gone

- Federal protections are gone

Locum tenens physicians should be especially careful. Locum roles do not automatically qualify for PSLF unless structured through a qualifying employer.

Weighing Aggressive Repayment vs. Financial Flexibility

Doctors are wired to eliminate problems fast.

Debt feels like a problem.

But early career flexibility often beats speed.

Aggressively paying off student loans may:

- Delay emergency savings

- Increase burnout risk

- Reduce financial resilience

This is why many physicians benefit from a balanced approach.

For deeper guidance, Read: [Should Doctors Pay Off Student Loans Early or Invest Instead]

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

You qualify for PSLF only if you work full-time for a government or nonprofit employer that meets federal PSLF criteria.

This includes many nonprofit hospitals, academic medical centers, VA facilities, and public health institutions.

You must have Direct Federal Student Loans to qualify for PSLF and most federal income-driven repayment plans.

If you have older FFEL or Perkins loans, they must be consolidated into a Direct Consolidation Loan to become eligible.

Yes, residency counts toward PSLF as long as you work full-time for a qualifying employer and make payments under an eligible repayment plan.

Many residents qualify through nonprofit teaching hospitals while enrolled in income-driven repayment.

Doctors can choose from standard repayment, income-driven repayment plans, forgiveness programs, and federal consolidation options.

The best choice depends on income level, employer type, and whether forgiveness is realistic.

Physicians qualify for income-driven repayment by having eligible federal loans and submitting income documentation annually.

Payments are based on discretionary income rather than total loan balance.

Yes, programs like PSLF, NHSC Loan Repayment, VA EDRP, and military repayment programs are commonly used by physicians.

Most require service commitments or employment in qualifying settings.

Income-driven repayment caps monthly payments at a percentage of discretionary income and adjusts annually based on earnings.

Any remaining balance may be forgiven after 20–25 years, or sooner under PSLF.

PSLF forgives remaining Direct Federal Loan balances after 120 qualifying monthly payments while working for a qualifying employer.

Many physicians qualify through nonprofit hospitals, academic centers, and government healthcare roles.

Lower income during residency and fellowship reduces monthly payments under income-driven repayment plans.

This period is often the most efficient time to accumulate qualifying payments toward forgiveness.

REPAYE or PAYE are usually the most beneficial for physicians with high debt, depending on income growth and family status.

REPAYE often helps during residency, while PAYE can cap payments later in high-income years.

PSLF forgiveness is tax-free under current federal law, while some non-PSLF forgiveness may be taxable.

Tax treatment can change, so long-term planning matters.