Student loan debt causes measurable financial stress and mental health strain among doctors, especially during medical school, residency, and early career years but its impact varies based on debt levels, income timing, repayment structure, and perceived control.

For some physicians, student debt creates persistent anxiety and burnout. For others, it delays major life decisions like homeownership, family planning, or career flexibility. And for many, the stress isn’t just about money, it’s about uncertainty.

What follows is a clear, evidence-based explanation of how student loan stress develops in doctors, why it’s so intense in medicine, and what actually helps reduce it without pretending the debt isn’t real.

The Burden of Student Loan Debt on Physicians

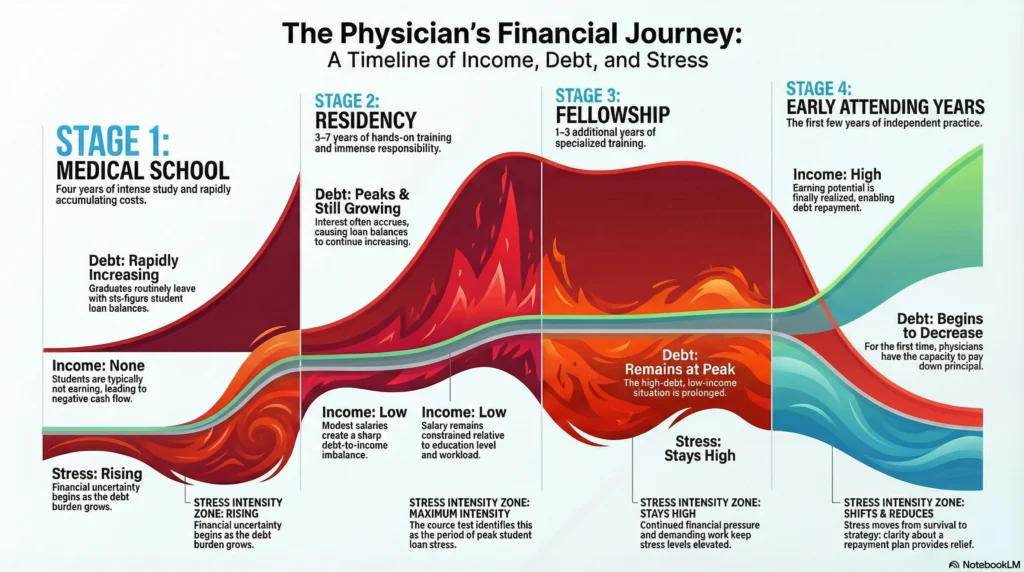

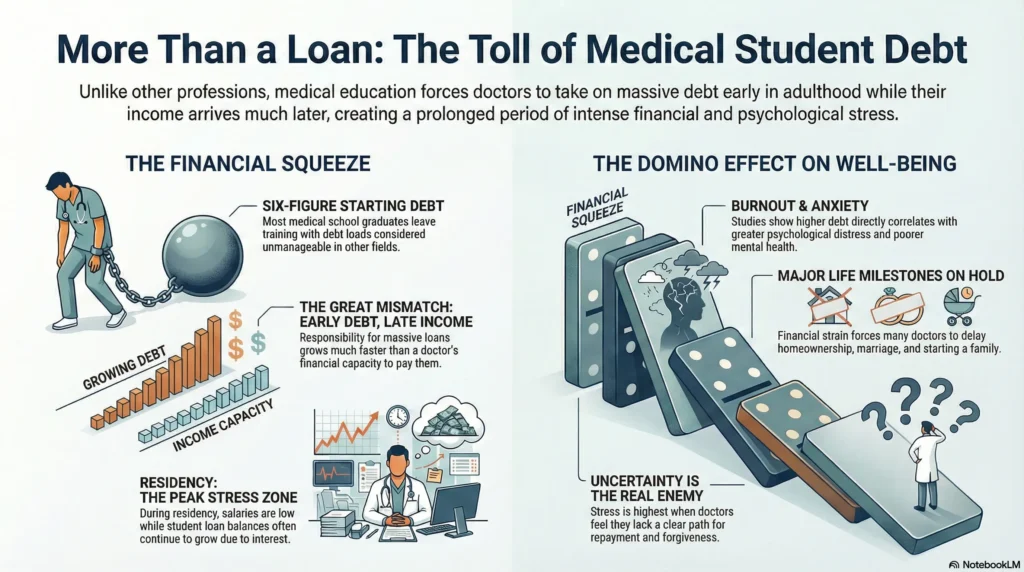

Student debt hits doctors differently than most professionals because medical education compresses extreme costs into the earliest years of adulthood, while income arrives much later.

That mismatch creates a long stretch where responsibility grows faster than financial capacity.

Typical Debt Amounts for Medical School Graduates

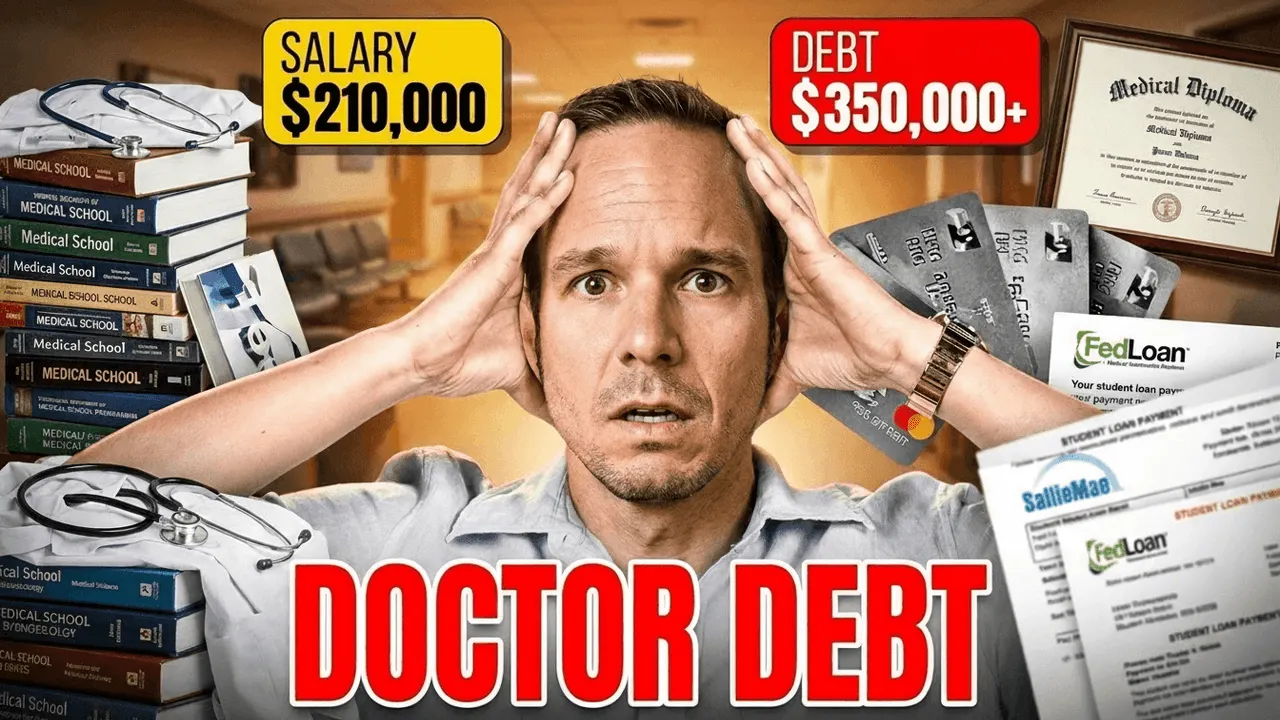

Most medical school graduates leave training with debt that would be considered unmanageable in almost any other field.

Research tracking U.S. medical school graduates shows that medical student debt routinely exceeds six figures, with balances often continuing to grow during residency due to interest accrual and limited repayment capacity.

Peer-reviewed evidence demonstrates that higher student loan debt is directly associated with higher reported stress levels and psychological burden, including anxiety and depressive symptoms

What matters most isn’t just the number. It’s the length of time doctors carry that debt, often well into their 30s and 40s.

Read: [Medical School Debt Explained: Why Doctors Graduate With Six-Figure Loans]

Financial Challenges Faced by Resident Physicians

Student loan stress peaks during medical residency because financial responsibility increases while income remains constrained.

Modest Resident Physician Salaries

During residency, doctors earn a salary that rarely reflects their workload or education level. This creates a sharp debt-to-income imbalance.

At the same time:

- Student loan balances continue to grow

- Interest capitalizes

- Repayment decisions feel permanent

This combination elevates stress levels even among otherwise resilient medical professionals.

Balancing Medical Training with Financial Obligations

Residents are expected to manage:

- Monthly student loan repayment decisions

- Income-driven repayment certifications

- Credit implications

- Long-term loan forgiveness eligibility

All while navigating clinical training, exams, night shifts, and emotional patient care.

That cognitive overload is a major but under-discussed contributor to financial stress.

Mental Health Implications of Financial Stress

Student loan stress is not a personality flaw. It is a predictable psychological response to prolonged financial uncertainty.

Prevalence of Anxiety and Burnout Among Physicians

Multiple longitudinal studies show that higher student debt correlates with higher stress levels and poorer mental health outcomes, including burnout.

A large academic review found that individuals with higher debt reported:

- Greater psychological distress

- Higher perceived stress

- Lower overall well-being

For physicians, this compounds existing burnout risks already present in the healthcare industry.

Link Between Financial Stress and Mental Health

Financial stress doesn’t just sit in the background. It actively shapes how doctors think about the future.

Mental health literature notes that uncertainty around repayment timelines and forgiveness eligibility increases anxiety, especially when borrowers feel they lack clear options

Stress is highest when doctors don’t know:

- Whether their repayment plan is “right”

- If forgiveness will still exist

- How long the debt will follow them

Clarity—not speed—is often the first stress reliever.

External Factors Compounding Financial Stress

Student loan stress rarely exists alone. It stacks on top of broader economic and professional pressures.

Broader Financial Obligations Beyond Student Loans

Doctors often delay:

- Homeownership

- Marriage or children

- Geographic flexibility

Research on young adult debt shows that perceived financial strain matters as much as actual debt amounts, especially when emergency savings are limited

For physicians, this can create social isolation—watching peers in other industries reach milestones sooner.

Strategies for Mitigating Financial Stress

This is not about optimization. It’s about reducing pressure.

Consumer financial research consistently shows that stress drops when borrowers move from avoidance to structure, even if the debt amount stays the same

Effective stress-reducing actions include:

- Creating a clear student loan repayment framework

- Choosing a repayment plan aligned with income reality

- Understanding eligibility for loan forgiveness

- Reducing daily decision fatigue

This doesn’t require paying more. It requires choosing once.

Read: [Federal Student Loan Repayment Options Explained for Doctors and Physicians]

Role of Debt Forgiveness and Broader Reforms

Loan forgiveness matters psychologically even for doctors who may never use it.

Public Service Loan Forgiveness and other federal student loan forgiveness programs:

- Reduce perceived debt burden

- Shorten mental timelines

- Increase career flexibility

Financial observers consistently note that long repayment horizons worsen stress and affect quality of life decisions, even when payments are manageable

Policy uncertainty increases anxiety. Stability—even imperfect—reduces it.

What This Means for Doctors Right Now

Student loan stress does not mean:

- You chose the wrong career

- You made a bad financial decision

- You’re behind

It means you’re experiencing a structural financial challenge unique to medicine.

Doctors who regain control don’t eliminate debt first. They eliminate uncertainty first.

If you’re ready to go deeper:

- Read: [Should Doctors Pay Off Student Loans Early or Invest Instead]

- Read: [Federal Student Loan Repayment Options Explained for Doctors and Physicians]

Stress eases when the path becomes visible.

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

Student loan debt reduces early-career cash flow and delays wealth-building milestones for many doctors.

Even high earners can feel financially constrained when large monthly payments coexist with housing, insurance, and family costs.

Student loan debt is strongly linked to higher stress, anxiety, and burnout among doctors.

The mental strain often comes from uncertainty—how long repayment will last and whether current choices are “right.”

Doctors must manage debt while juggling demanding clinical workloads, complex repayment rules, and delayed income growth.

The challenge is not just paying loans, but making long-term decisions under pressure with limited time and clarity.

Student loan debt can push some doctors toward higher-paying specialties or away from lower-paid primary care roles.

The pressure is not universal, but debt concerns can influence where and how doctors choose to practice.

Doctors benefit most from choosing a clear repayment structure that reduces uncertainty and decision fatigue.

Mental well-being improves when repayment feels intentional rather than reactive—even if balances remain high.

Loan forgiveness programs can significantly reduce stress by shortening the perceived repayment timeline.

Even doctors who may not ultimately qualify often feel relief simply knowing forgiveness is an option.