Yes, most doctors need a deliberate student loan repayment strategy—because medical school debt is large, repayment timelines are long, and income alone does not protect you from costly mistakes.

This is especially true for physicians with six-figure debt, delayed earning years, and rapidly rising income after residency, where the wrong choice can cost hundreds of thousands of dollars over time.

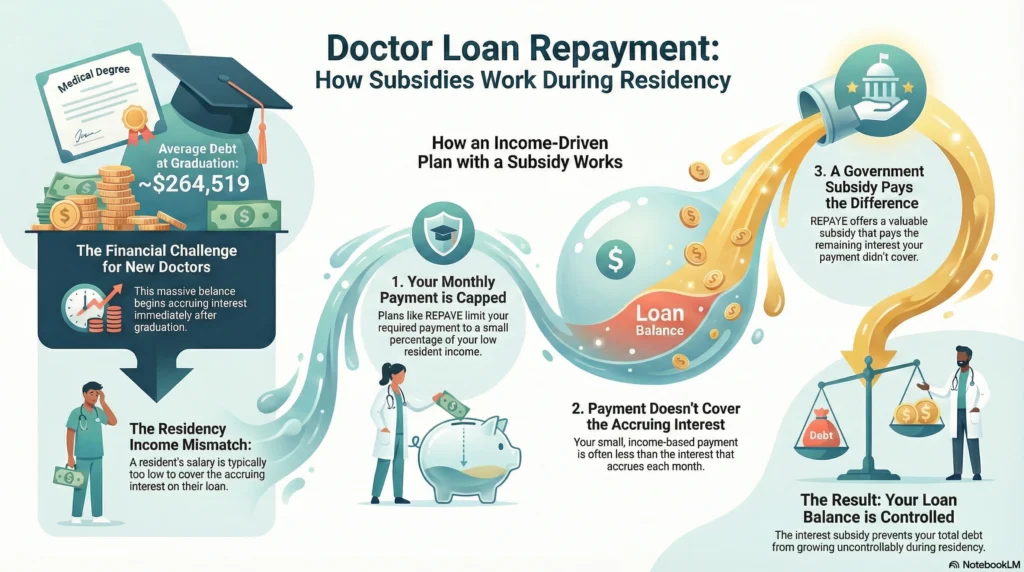

Most doctors graduate with significant debt. About 73% of medical students graduate with student loan debt, and the average balance is roughly $264,519, a figure that applies across medical, dental, and other high-cost health degrees but is especially punishing for physicians due to long training periods

Doctors’ student debt often rivals or exceeds early-career income. Gen Z physicians face debt-to-income ratios around 64%, and 74% of doctors had to rebalance their budgets once federal payment pauses ended

This guide exists so you don’t guess.

You’ll learn:

- How the major federal repayment plans actually work

- When forgiveness makes sense (and when it doesn’t)

- How high income changes the math

- How to balance repayment with investing

- And how to build a clear, defensible plan instead of reacting year by year

Revised Pay As You Earn (REPAYE)

REPAYE is often the default starting point for residents—and for good reason.

What it is

REPAYE is an income-driven repayment plan that sets monthly payments at 10% of discretionary income and offers a valuable interest subsidy when payments don’t cover accruing interest.

Why it matters

During residency, your income is low while interest continues to accrue. REPAYE limits payment shock and prevents loan balances from ballooning.

The American Medical Association notes that residents who plan early can reduce repayment stress and avoid unnecessary interest capitalization by choosing the right plan before the grace period ends

Who it’s best for

- Residents and fellows

- Physicians pursuing Public Service Loan Forgiveness

- Doctors with very high federal loan balances relative to income

The tradeoff

Once income spikes as an attending, REPAYE payments can rise quickly—sometimes higher than alternatives. That’s not a flaw. It’s a signal to reassess.

Income-Based Repayment (IBR)

IBR looks similar to REPAYE, but the details matter.

What it is

IBR limits payments to 10–15% of discretionary income and critically caps payments so they never exceed what you’d owe on the Standard Repayment Plan.

Why it matters

For physicians whose income rises rapidly, that cap can protect cash flow during early attending years.

Who it’s best for

- Doctors with rising income who want predictability

- Physicians unsure whether forgiveness will pan out

- Those who want a payment ceiling

The downside

IBR generally lacks the interest subsidy that makes REPAYE attractive during residency.

Repayment Assistance Plan (RAP)

RAP is not one plan, it’s a category.

What it is

Loan repayment assistance offered by hospitals, states, nonprofits, or institutions in exchange for service.

Why it matters

Physician shortages are real. Employers are using loan repayment incentives as recruiting tools.

Who it’s best for

- Primary care physicians

- Psychiatrists

- Doctors willing to work in Health Professional Shortage Areas

Programs vary widely. Some offer $25,000. Others exceed $100,000 over time.

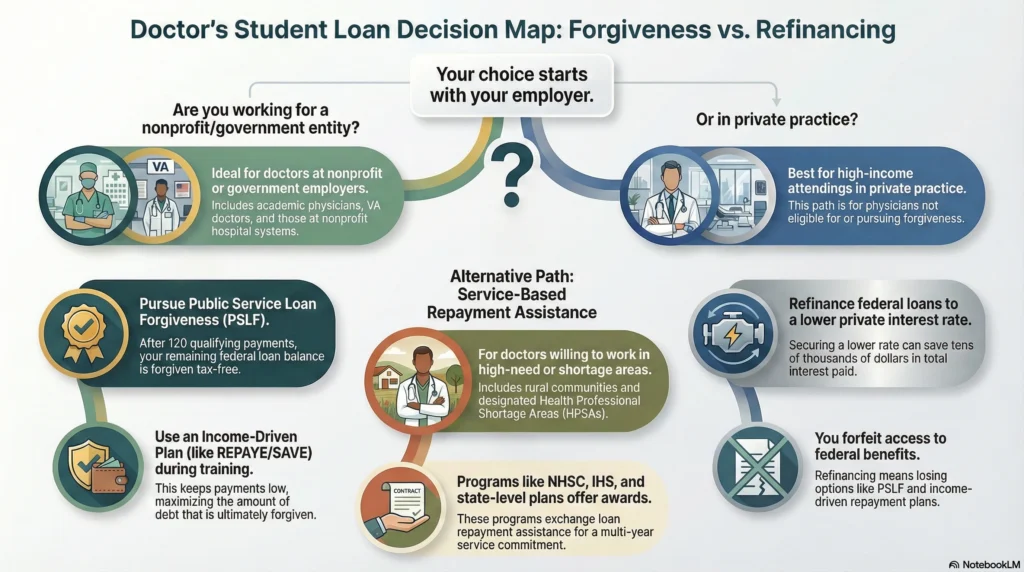

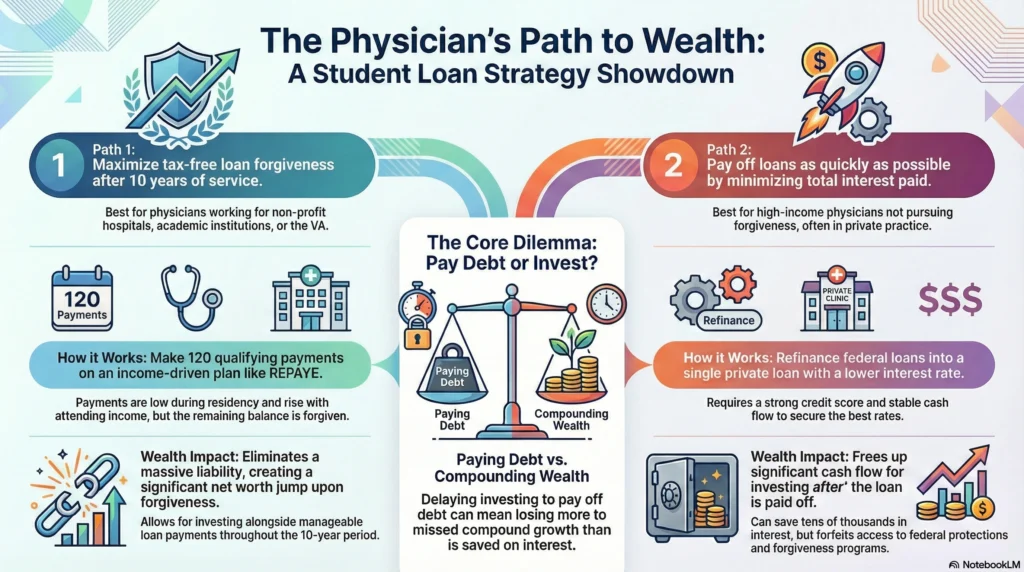

Public Service Loan Forgiveness (PSLF)

PSLF is the most powerful repayment option for doctors who qualify—and the most misunderstood.

What it is

Make 120 qualifying payments while working full-time for a qualifying employer. The remaining balance is forgiven tax-free.

Why Physicians Benefit From PSLF Program

Physicians often have the perfect profile for PSLF: high debt, nonprofit employment, long training years.

Federal reforms have increased approval rates substantially in recent years, making PSLF more reliable when rules are followed

(https://studentaid.gov/manage-loans/forgiveness-cancellation/public-service).

Who it’s best for

- Academic physicians

- VA doctors

- Employed hospital physicians under nonprofit systems

The real risk

Not PSLF itself—but poor documentation and inconsistent certification.

PSLF Eligibility Criteria And Requirements

PSLF only works if you meet every requirement.

You must:

- Hold Direct federal student loans

- Work full-time for a qualifying employer

- Enroll in a qualifying repayment plan

- Certify employment regularly

Miss one step, and payments may not count.

Advantages for Medical Professionals

For doctors with large balances:

- Payments stay manageable during training

- Forgiveness occurs when balances are highest

- Forgiven amounts are not taxable

That combination is rare—and valuable.

Steps to Apply

Step 1: Confirm loan types

Ensure loans are Direct Loans. Consolidate if needed.

Step 2: Choose a qualifying repayment plan

Typically REPAYE or IBR.

Step 3: Certify employment annually

Submit the PSLF Employment Certification Form every year.

Step 4: Track qualifying payments

Use the Department of Education portal and keep records.

Step 5: Reassess annually

Income changes. Strategy should too.

Government and State-Based Repayment Assistance Programs

When we talk about repayment assistance beyond federal plans like REPAYE, IBR, and PSLF, there’s a second class of programs that directly reduce balances for doctors who serve in areas with healthcare workforce shortages. These programs are funded through federal dollars, state budgets, or both, and they often require service commitments such as working in underserved or rural areas.

National Health Service Corps (NHSC) Loan Repayment Program

The NHSC is a federal initiative for clinicians who commit to practice in Health Professional Shortage Areas (HPSAs).

- The core NHSC Loan Repayment Program can repay part or all of your student loans if you agree to work in an NHSC-approved site.

- There are multiple tracks, including the Substance Use Disorder Workforce LRP and Rural Community LRP, allowing flexibility based on practice location and specialty.

- Awards can potentially total tens of thousands of dollars while you serve in high-need areas.

Under the NHSC State Loan Repayment Program, federal funds are granted to states and territories, enabling them to operate their own state-specific repayment initiatives. These programs often mirror NHSC eligibility (service in shortage areas) but are administered by state agencies.

Federal support from NHSC and the State Loan Repayment Program works with PSLF and other federal plans. Some doctors can combine help from these programs. But they must work in qualifying shortage areas.

Indian Health Service (IHS) Loan Repayment Program

This is another federal program aimed at expanding care in underserved Native communities.

The IHS Loan Repayment Program lets eligible doctors and health workers get up to $50,000 in loan repayment. They must commit to serve for two years at facilities that care for American Indian and Alaska Native people.

NIH Loan Repayment Programs (LRPs)

Although not physician-practice-location based like NHSC or IHS, the NIH LRPs exist to keep clinicians in biomedical and clinical research roles by repaying loans in exchange for research service commitments. These are often relevant for doctors who pursue research careers and still face significant medical school debt.

Individual State Programs

Many U.S. states have their own loan repayment or forgiveness programs. These are for doctors who serve in certain places, like rural or underserved communities. These areas are often called HPSAs or medically underserved areas. These programs typically pair service obligations with loan repayment benefits.

Some states have programs that operate independently; others piggyback on federal HRSA funding such as the NHSC State Loan Repayment Program.

Here are specific examples state-by-state:

Montana Rural Physician Incentive Program (MRPIP)

- Physicians who agree to practice in rural or medically underserved areas may qualify for repayment assistance.

- Physicians practicing full-time can receive up to $150,000 over five years toward educational debt.

Maryland State Loan Repayment Programs

- Maryland’s State Loan Repayment Program (SLRP) and Maryland Loan Assistance Repayment Program offer debt repayment funds for physicians and other clinicians who serve in medically underserved or shortage areas.

Louisiana Physician Loan Repayment Program

- Physicians serving in HPSAs may receive up to $30,000 annually for five years.

- Completing a five-year obligation with compliance can allow renewal with additional awards for extended service.

Georgia Physician Education Loan Repayment Program

- The Georgia Board of Health Care Workforce administers programs for physicians who agree to practice in underserved or rural counties. These programs help pay down debt in exchange for service.

Texas Loan Repayment and Incentive Programs

Though administered under multiple labels within the state (e.g., Primary Care Office programs), Texas offers a suite of physician repayment and incentive programs, including:

- Rural Community Loan Repayment Program

- Physician Education Loan Repayment Program

- St. David’s Foundation Public Health Corps Loan Repayment Program

- Substance Use Disorder Workforce Loan Repayment Program

These can provide targeted repayment assistance for primary care doctors and other clinicians who choose underserved practice sites.

Private and Employer-Based Loan Forgiveness Options

Some hospital systems offer repayment as part of compensation packages.

Always clarify:

- Vesting schedules

- Tax treatment

- Contract obligations

Loan Refinancing Strategies

Refinancing replaces federal loans with private ones.

Why it matters

Lower interest rates can save tens of thousands over time.

Best for

- High-income attendings

- Physicians not pursuing forgiveness

- Doctors with strong credit scores

The risk

You permanently lose federal protections.

Calculating Potential Savings

Refinancing works best when:

- Interest rates are high

- Forgiveness is off the table

- Cash flow is stable

Tools like loan calculators help—but context matters more than spreadsheets.

Balancing Aggressive Debt Repayment and Investment

This is where doctors struggle most.

Paying debt early feels safe.

Investing early builds compounding.

The right balance depends on:

- Interest rates

- Forgiveness eligibility

- Risk tolerance

- Time horizon

Doctors who delay investing entirely often lose more to missed compound growth than they save on interest.

Read: [Should Doctors Pay Off Student Loans Early or Invest Instead? A Numbers-Based Comparison]

Also Read These for Deeper Clarity

What to Do Next (Without Pressure)

If this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

Listen to the audio version of this guide while commuting or between shifts

Listen to the audio version of this guide while commuting or between shifts Read our book on Amazon for a structured walkthrough of financial freedom for doctors

Read our book on Amazon for a structured walkthrough of financial freedom for doctors Download the free LIFTOFFNOW ebook to understand the full framework

Download the free LIFTOFFNOW ebook to understand the full framework Book a free 10–15 minute clarity call if you want to talk through your situation

Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.

FAQ

The average physician graduates with roughly $240,000–$265,000 in student loan debt, depending on school type and specialty path. This figure includes federal Direct Loans and Grad PLUS loans.

Most physicians pay $2,000–$4,000 per month once they reach attending income, depending on repayment strategy. Residents often pay far less under income-driven repayment plans.

Yes, most doctors eventually pay off their student loans, but the timeline varies widely based on whether they pursue forgiveness, refinance aggressively, or balance repayment with investing.

It usually takes 10 to 25 years to fully pay off medical school debt. The time depends on whether the doctor uses standard repayment, income-driven plans, forgiveness programs, or refinancing.

Yes, doctors can qualify for forgiveness through programs like PSLF, NHSC, VA, and state-based repayment programs, provided they meet employment and service requirements.

Medical students themselves do not receive forgiveness, but the loans they take can later qualify for forgiveness once they become employed physicians in eligible roles.

The most effective strategies include income-driven repayment with forgiveness, targeted loan repayment programs, or refinancing paired with aggressive payoff, depending on career path and employer type.

Doctors can use REPAYE/SAVE, IBR, PSLF, NHSC programs, VA repayment, state programs, and refinancing, each with different tradeoffs tied to income and job setting.