If you feel confused, you’re not behind.

No one taught you how money actually works.

Medical training teaches diagnosis, treatment, and risk mitigation.

It does not teach how income turns into net worth, how debt affects decisions, or how investments compound over decades.

So doctors do what rational people do.

They follow defaults.

- contribute to retirement accounts

- pay bills on time

- upgrade lifestyle gradually

- assume higher income will fix everything

Then years pass.

Income is high.

Stress is still there.

Clarity is missing.

This playbook gives you a clear mental model for financial planning, from zero knowledge to confident execution.

By the end, you will understand:

- how to set financial goals that actually guide decisions

- how to manage cash flow without budgeting misery

- what foundations must come before investing

- how to invest without gambling

- how to avoid common mistakes doctors make

Financial planning for doctors is not about making more money.

It is about not wasting the money you already worked so hard to earn.

Step 0: Understand the Real Problem Doctors Face

Doctors face unique financial challenges that set the stage for poor habits:

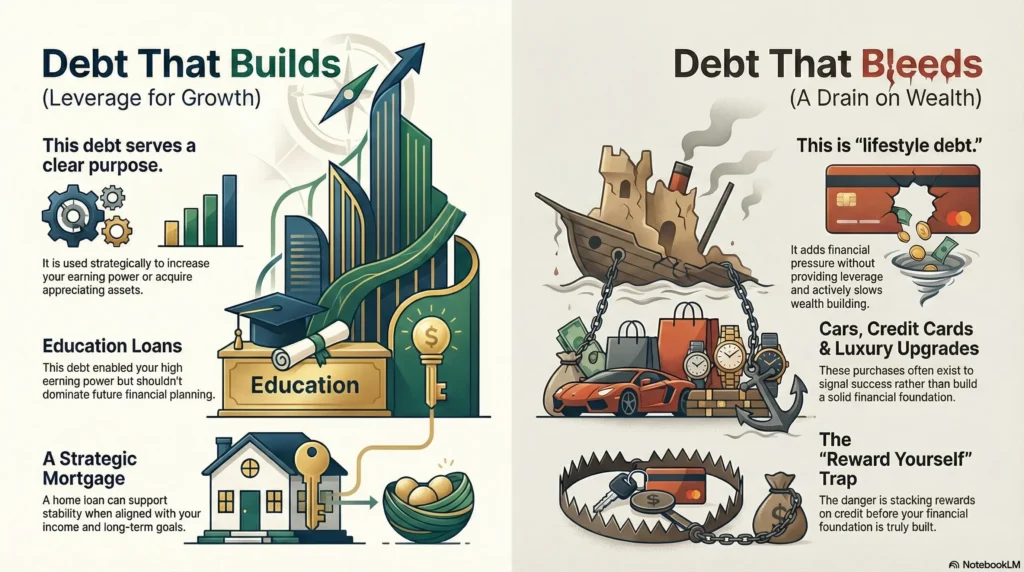

- Delayed earnings due to medical school and training. Physicians often complete residency around age 30–32, 10 years later than age-matched peers. This “late start” means colleagues in other fields may already own homes and save for retirement while doctors are still in school or low-paid training.

- High student loan debt. About 76% of medical students graduate with around $200,000 of debt. This heavy debt load contributes to high rates of financial stress and even physician burnout

- Perceived income stability but hidden volatility. Doctor salaries can feel secure, but events like burnout, injury, or healthcare policy shifts can abruptly cut income. In fact, medical burnout is prevalent and dangerous – studies note burnout is linked to poor mental health and higher physician suicide rates. Doctors must plan for income disruptions.

- Lifestyle pressure and high earning potential. With high incomes come expensive habits. It’s tempting to increase spending whenever pay rises, which can outpace saving and leave no buffer

- Responsibility to loved ones. Many doctors have families relying on them. Protecting loved ones adds pressure (e.g., making sure there’s life or disability insurance in place).

This creates a dangerous pattern.

High income creates false security.

Planning gets delayed because “there’s time.”

Spending increases because “I earned this.”

Investing decisions feel scary because mistakes can cost a lot.

The goal of financial planning is to remove dependence on uninterrupted income.

That is financial freedom.

Step 1: Define Financial Goals Doctors Actually Care About

Why “retirement” is not a useful starting goal

“Retirement” alone is too vague to motivate action. A far-off goal feels abstract and emotionally empty, so it doesn’t influence daily choices. Instead, doctors need goals that answer, “What problem am I solving with money?”. Think in terms of life outcomes, not just account balances. Examples of meaningful goals for physicians include:

Better beginner-friendly goals for doctors

Think in life outcomes, not account balances.

Examples that actually work:

Time freedom

Being able to reduce hours without financial stress.

Practice flexibility

The ability to change roles, negotiate employment contracts, or exit private practice without panic.

Burnout protection

Money that allows rest, retraining, or career adjustment.

Family security

Knowing loved ones are protected through insurance planning and savings.

Legacy and continuity

Planning for estate needs, succession planning, or business transition if you own a practice.

These goals create motivation and clarity.

Short-term (1–3 years) | Medium-term (5–10 years) | Long-term (15+ years) |

|---|---|---|

emergency fund | investment accounts outside retirement | retirement savings |

student loan management | practice ownership or exit planning | wealth preservation |

home down payment fund | reducing dependence on salary | estate planning and legacy |

Step 2: Income, Expenses, and Cash Flow (The Foundation Most Doctors Skip)

Why Traditional Budgeting Often Fails Doctors

Budgeting by restriction often fails busy doctors. Traditional budgets assume you have time and emotional bandwidth to track everything. But physicians’ workdays are long and free time is limited. In a 2020 survey, only 18% of physicians had a formal written budget, and 33% had none at all. With hectic schedules, missing one month of tracking can collapse the whole system, creating guilt rather than clarity.

Think in cash flow, not restriction

Instead of micro-budgeting, focus on cash flow: three questions – how much comes in, where it goes, and what remains. You don’t need to record every coffee; you need to ensure the money is flowing the right way. Key rules:

- Automate savings and investing first. Transfer money to savings/investments as soon as you’re paid (a “pay yourself first” strategy). Automation makes saving invisible.

- Keep fixed expenses reasonable. House, cars, loan payments, and insurance (fixed costs) are often your largest obligations, defining your lifestyle. Reducing these can dramatically improve cash flow.

- Resist gradual lifestyle creep. Small variable expenses (dining, travel, subscriptions) add up quietly. Whereas cutting a car payment or refinancing a mortgage (fixed costs) can have bigger impact on your budget.

- Avoid mental accounting guilt. If you automate and stay below your means, you can enjoy discretionary spending without constant tracking

Think of your paychecks as buckets: let essential costs and savings be buckets first, and use only what’s left for wants. By focusing on direction (increasing your “saved” bucket) rather than minutiae, you build a resilient financial base without exhausting time.

Understand fixed vs variable expenses

- Fixed expenses: These recur monthly at roughly the same level (housing, insurance, student loan minimums, etc.). They typically include your largest financial obligations. Because fixed costs dominate budgets, small percentage reductions (e.g. refinancing a loan) can free up significant cash.

- Variable expenses: These change each month (food, travel, entertainment, upgrades). They can balloon slowly if unchecked.

High-impact improvements usually come from reducing large fixed costs, not sweating over every latte. Set your fixed expenses to a level that lets you save and invest comfortably, then let yourself enjoy reasonable variable spending.

Tools beginners can safely use

You don’t need advanced software to start. Useful tools include:

- Expense-tracking apps. Apps or simple spreadsheets to identify spending patterns.

- Net worth trackers. Regularly checking your assets vs. liabilities keeps you motivated as savings grow.

- Bank/card alerts. Set up notifications or caps on spending to catch surprises (like subscriptions you forgot).

- Automated payments. Automate bills and contributions so you pay on time without thinking.

These measures provide clarity with minimal effort. Automation removes willpower strain, helping build stability quietly in the background.

Step 3: Mandatory Foundations Before You Invest

Emergency fund: why doctors need more than average

Doctors face unique risks: burnout, unexpected income loss, or major liabilities. An emergency fund is a financial safety net for large unforeseen expenses (home repair, illness, tax bill) or sudden income stops. For most people, the rule of thumb is 3–6 months of living expenses. Given doctors’ high expenses and risks, many advisors suggest aiming toward the higher end (6–12 months) for peace of mind. This money is for peace of mind, not growth – liquidity beats returns here. Keep it safe and accessible (high-yield savings or money market accounts), and commit to rebuilding it if you ever use it.

Insurance planning explained simply

Insurance protects your income and assets from disasters – it’s not an investment. Key coverages for physicians include:

- Health insurance: Protects you from catastrophic medical bills (critical even for healthy doctors).

- Disability insurance: Since you are your biggest asset, your earning power must be protected . Disability insurance replaces most of your income if illness or injury prevents you from practicing. (Roughly 1 in 7 physicians end up using disability insurance during their careers.)

- Malpractice (professional liability) insurance: Protects you from the financial catastrophe of medical lawsuits. It “pays all or part of the cost of your defense and any judgments against you” . This is often very expensive but indispensable in high-risk specialties.

- Term life insurance: Protects your family if you die unexpectedly. Life insurance “provides your loved ones financial protection if you die unexpectedly” . As an attending physician, even though your income is high, a relatively cheap term policy ensures your family isn’t burdened by mortgages or loans if you’re gone.

If insurance feels complex, that’s normal. Start with the basics: ensure each of these risks (health, income, liability, life) is covered well enough to prevent financial ruin. The goal is risk management, not optimization – you want adequate protection in place.

Retirement accounts: useful but incomplete

Employer-sponsored retirement plans (401(k), 403(b), 457, etc.) are excellent tools: they reduce your taxable income today and automate long-term savings. For example, in 2025 you can contribute up to $23,500 to a 401(k) (plus catch-up if eligible) . However, these accounts have limits and restrictions:

- Contribution limits cap growth. You can’t shelter unlimited income. The IRS sets firm caps each year , so high earners often outgrow these accounts.

- Liquidity is restricted. Withdrawals before retirement age typically incur taxes and penalties, so retirement accounts aren’t a source of emergency cash or medium-term goals.

- Not the whole plan. Think of retirement accounts as one tax-advantaged bucket in your toolbox, not as your entire financial plan.

Once you’ve maxed out what’s feasible in retirement plans, you’ll need other accounts (like taxable or Roth) for flexibility. But start by contributing at least enough to get any employer match – that’s free money.

Step 4: Investing Beyond Retirement Accounts (Without Fear)

First, understand risk in plain language

Risk in investing has two aspects:

- Risk tolerance: How much market volatility you feel you can handle emotionally.

- Risk capacity: How much you can afford to lose without derailing your life or goals.

Doctors often overestimate their tolerance (they can intellectually handle stock losses) and underestimate capacity issues (losing money could disrupt debt plans or contract obligations). This mismatch breeds anxiety. Clarify both: how much would actually hurt your plans, and can you handle the swings?

Core growth assets beginners should understand

You don’t need complicated products to build wealth over time. In fact, most long-term market growth has come from basic stock market investments. The S&P 500 index, for example, has historically returned about 10% per year on average (≈7% after inflation) . That growth is powered by U.S. companies’ profits. Beginners should focus on:

- Stocks or equity index funds: Broad, low-cost funds (e.g. total market or S&P 500 index funds) that own many companies.

- Diversified mutual/index funds: Vehicles that spread your investment across sectors and geographies.

These simply represent fractional ownership of businesses. They will grow over decades, but unevenly (markets have busts and booms). The key is consistency: invest regularly and stay invested. Long-term consistency beats short-term timing. Most advisors note that “the best way for less experienced investors to time the market is not to do so at all” . In practice, this means avoid obsessing over short-term swings – keep adding to your investments on schedule.

Alternative investment options

Some doctors explore investments like real estate, self-storage, commodities, or crypto. These can diversify beyond stocks but add complexity, fees, and risk you may not fully understand. Beginners should focus on education first, not on quickly allocating money. Before putting significant funds into an unfamiliar asset, learn its downsides, tax implications, and how it fits with your other goals. Often, a small exposure (if any) is fine once core allocations are set.

Remember: diversify broadly, but don’t diversify yourself into confusion.

Step 5: Diversification Is About Behavior, Not Assets

The purpose of diversification is to protect you from yourself. It guards against bad timing and panic selling. However, piling into many accounts or exotic investments can hurt beginners by causing:

- Tracking fatigue (too many accounts to watch)

- Decision paralysis (what to invest in next?)

- Emotional reactions to each portfolio’s swings

In fact, data show simple index portfolios often match or outperform more complex strategies. For example, a Vanguard “3-fund” index portfolio recently beat the average large college endowment’s return over 3, 5, and 10 years (https://awealthofcommonsense.com/2021/08/simple-vs-complex-2020-edition), simply by keeping costs low and rebalancing. In practice, a clear, simple portfolio with a few broad funds will likely serve you better than trying to chase performance with dozens of funds.

Simple allocation beats perfect allocation

Beginners do best with:

- Fewer buckets. E.g. one fund each for U.S. stocks, international stocks, and bonds (or a target-date fund that covers them).

- Clear purpose for each. Don’t pick funds just because they’re “hot”; pick ones that align with your risk and goals (e.g. growth vs stability).

- Rules instead of opinions. Have an investment plan (like “I’ll always keep 20% in bonds”) and stick to it.

Remember: you’re not trying to beat professionals. You’re building your financial well-being. As one physician-author warns, “investing prowess doesn’t come automatically — unless you choose a simple strategy like low-cost index funds” . In fact, simple index strategies outperform most active DIY approaches almost all the time.

Learn to ignore short-term noise

Markets move daily; wealth grows slowly over years. Constantly checking your balances usually just raises anxiety without improving decisions. As noted above, do not try to time the market . Set up a schedule (e.g. monthly or quarterly) for reviewing long-term performance, not hourly. Over time, you’ll see progress if you consistently invest and hold quality assets.

Preventing Impulsive Financial Decisions

Why smart doctors still make money mistakes

High intelligence doesn’t equal financial smarts. Medical training rewards decisive answers in life-or-death scenarios; financial markets reward patience and probability. This mismatch often leads doctors to overconfidence: feeling they should do their own sophisticated investing, or believing they can out-guess the market. They underestimate emotional biases (fear and greed) that derail even highly educated people.

Simple rules that protect beginners

Implement guardrails for common pitfalls:

- Waiting periods for large purchases. When tempted by a big buy (car, gadget), put it off for a week or more. You’ll often realize you don’t need it as much after cooling off.

- Written checklists for investing. Before moving money, use a checklist: “Does this fit my asset allocation? Have I done my research? What is my worst-case outcome?” This reduces impulse buys.

- Automated savings and debt payments. Automate transfers so decisions happen by plan, not by momentary feeling.

These rules take willpower out of the equation. They ensure you act according to your strategy, not your impulses.

What to Do Next (Without Pressure)

f this guide felt helpful but overwhelming, that’s okay.

You do not need to master everything at once.

Here are simple next steps.

- 🎧 Listen to the audio version of this guide while commuting or between shifts

- 📘 Read our book on Amazon for a structured walkthrough of financial freedom for doctors

- 📥 Download the free LIFTOFFNOW ebook to understand the full framework

- 📞 Book a free 10–15 minute clarity call if you want to talk through your situation

Medicine and Money Show exists to educate, not sell.

No courses.

No coaching.

No financial products.

Just clear guidance for doctors who want to turn hard work into lasting wealth.